Killer Bees Market Brief March 26, 2026

The Sting

The S&P 500 rallied 0.54% on Wednesday on hopes that a 15-point U.S. peace proposal would end the Iran war. By Thursday morning, futures were down 0.72% after Tehran rejected the deal and Axios reported the Pentagon is drawing up plans for a "final blow." Somewhere in between those two headlines, Arm HoldingsARM-- reinvented its entire business model and Circle posted its worst day ever and neither had anything to do with the Middle East. Funny how that works.

Deep Dive #1: ArmARM-- Just Blew Up the Switzerland Model

For 35 years, Arm Holdings (ARM) has been the Switzerland of semiconductors license the instruction sets, collect royalties on every chip, compete with nobody. On Tuesday, that era ended. Arm unveiled the AGI CPU, its first in-house silicon product ever, designed for AI inference in data centers. The stock ripped 16% on Wednesday. Meta is the launch customer.

Here's what most coverage missed: this isn't just a new chip. It's a new business model. Arm went from toll booth to car manufacturer while still running the toll booth. Haas projected $15 billion in AGI CPU revenue by 2031, total annual revenue of $25 billion, and $9 EPS. Arm did $4 billion in 2025. That's a six-bagger in six years, priced in before a single chip ships.

The interesting part is who this threatens. Arm's customers IntelINTC--, AMDAMD--, QualcommQCOM-- are now its competitors. The AGI CPU claims 2x performance over traditional x86 platforms, which is basically walking into Intel's living room and rearranging the furniture. Haas said CPU demand will see a 4x increase from agentic AI workloads and admitted he might be "under-calling that number."

Raymond James immediately upgraded to outperform with a $166 target. But the real tell was the 50-partner endorsement video at launch. AWS, Google, Microsoft, Nvidia, Broadcom, Samsung, all lined up to bless the move. When your competitors publicly cheer your entry into their market, either they're being diplomatic or they're genuinely relieved someone is building what they needed but didn't want to build themselves. I'm not sure which is more bullish.

Deep Dive #2: Circle's 20% Haircut and the War Over Stablecoin Yield

Circle dropped 20% on Tuesday its worst single day since going public after a draft of the Clarity Act revealed language that would ban stablecoin issuers from paying yield on passive balances. Volume hit 56.4 million shares, roughly 289% above its three-month average. This wasn't an orderly repricing. This was get-me-out selling.

The setup matters. Circle had been up 170% since early February. Higher-for-longer rates (thanks, Iran oil shock) had been a tailwind because Circle earns the vast majority of its revenue from interest on Treasury reserves backing USDCUSDC-- $733 million of its $770 million Q4 revenue came from T-bill interest. The stock was a leveraged bet on rates staying elevated. Then one legislative draft zeroed in on the mechanism that makes the flywheel spin: yield as customer acquisition.

The question nobody's asking: does this actually matter? The yield ban targets the incentive to hold USDC but the real growth is in tokenized assets, prediction market settlement, and AI-agent payments, none of which depend on passive yield. Polymarket processed $22 billion in volume last year using USDC as settlement. Clear Street's Owen Lau called it "an overreaction." ARKARK-- Invest scooped up over $20 million of the dip. Meanwhile, Tether chose the same day to announce a Big Four reserve audit competitive knife-twist or coincidence, you decide.

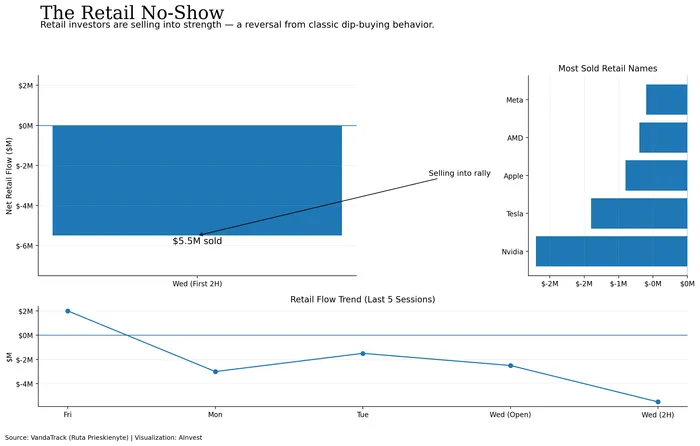

Chart of the Week: The Retail No-Show

Everyday investors net sold $5.5 million of U.S. single stocks in the first two hours of Wednesday trading — right into a ceasefire-hope rally.

VandaTrack's Ruta Prieskienyte flagged it: retail isn't chasing the bounce. Nvidia — broadly the most popular retail pick of the last two weeks — was the most sold name on Wednesday despite climbing 2%. "Retail is not chasing the ceasefire hope driven bounce and is instead trimming exposure in its most crowded AI winner," Prieskienyte wrote. This matches Monday's pattern. The dip-buyers have become the rip-sellers.

That's notable because retail has been the marginal bid for the better part of two years. When the most enthusiastic buyers start using rallies as exit liquidity instead of entry points, you're watching a sentiment regime change in real time. It doesn't mean the market goes down tomorrow — but it means the next leg has to come from somewhere else.

The Hive Mind

FinTwit is debating whether Arm can execute fabless without cannibalizing its licensing moat the bull case and bear case are the same chart read two ways. On r/stocks, the Circle selloff has retail split between "generational buying opportunity" and "the business model is one Senate markup away from collapse." Most retweeted take: a thread arguing Iran ceasefire whiplash is training the market to ignore geopolitics entirely — which, if true, is itself a geopolitical risk.

The Thread

Two stories: a 35-year-old chip licensor decides it needs to make things, and a one-year-old stablecoin issuer learns that regulators might unmake the thing that made it work. Both are about the same question what happens when the business model that got you here isn't the business model that gets you there? Arm is betting the answer is reinvention. Circle is finding out the answer might be imposed on it. In both cases, the market moved 15-20% in a single session. That's not analysis. That's a repricing of identity. And it happened on a day when everyone was supposed to be watching Iran.

Senior strategist with 20+ years experience delivering data-driven research, ETF and stock analysis, and practical investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet