Killer Bees Market Brief March 19, 2026

The Sting

Micron just posted the most absurd semiconductor quarter in recent memory revenue nearly tripled, EPS beat by 31%, Q3 guidance exceeded its entire annual revenue through fiscal 2024 and the stock dropped 4% after hours. Not because anything went wrong on the call. Because Iran hit Qatar's LNG infrastructure while Sanjay Mehrotra was still talking. Welcome to 2026, where even a generational AI earnings print can't outrun a cruise missile.

Deep Dive #1: The Gulf Energy War Just Changed the Math on Everything

Here's what happened in the last 48 hours: Israel struck Iran's South Pars gas field the largest natural gas field on the planet in what Qatar and the UAE called "a dangerous escalation." Iran responded by attacking Qatar's Ras Laffan complex (the world's biggest LNG export facility), hitting gas infrastructure in the UAE, launching drones at Saudi and Kuwaiti refineries, and continuing to choke the Strait of Hormuz. Brent crude blew past $110 a barrel Thursday morning, up more than 50% since the war started on February 28th. WTIWTI-- touched $97. The Brent-WTI spread widened to its largest since May 2019.

The policy response has been aggressive and, so far, insufficient. The IEA coordinated a 400-million-barrel release from strategic petroleum reserves including 172 million barrels from the U.S. SPR. The White House issued a 60-day Jones Act waiver covering oil, gas, fertilizer, and coal. Trump eased sanctions on Venezuelan oil to try to boost global supply. None of it has mattered. Brent is still north of $110 because the problem isn't inventory it's geography. When the world's most critical energy chokepoint is an active war zone and the Gulf's biggest LNG and refining complexes are taking direct hits, no amount of SPR drawdowns will fix the supply curve.

And then Wednesday afternoon, Powell made the quiet part loud. The Fed held rates at 3.50%–3.75% as expected, kept the dot plot at one cut for 2026, and raised their core PCE forecast to 2.7%. But the real signal was in the press conference: Powell explicitly said energy prices from the Middle East conflict could preclude any rate cut this year. February's PPI had already come in scorching — +0.7% month-over-month, the biggest jump in a year, double the 0.3% consensus. So the sequence is: missiles hit energy infrastructure → oil spikes → inflation reaccelerates → the Fed can't cut → risk assets reprice. The Dow dropped 768 points on Wednesday to a new 2026 closing low, falling below its 200-day moving average for the first time since May 2025. The S&P 500 closed at 6,625, just a few points above its own 200-day. Over 75% of U.S. issues declined. It didn't matter if you were large-cap or small-cap the Russell 2000 fell 1.64%, the Dow 1.63%, the Nasdaq 1.46%.

The question nobody's asking: What happens to corporate earnings estimates if Brent stays above $100 for a full quarter? We've been so focused on rate cut timing that we've barely started modeling the margin compression for airlines, chemicals, logistics, and consumer discretionary. The 1970s comparisons are lazy but the transmission mechanism from energy shock to earnings revision is very real, and the Street hasn't repriced it yet.

Deep Dive #2: Micron's Supercycle Print Got Photobombed by Geopolitics

Let's just sit with these numbers for a second. MicronMU-- reported fiscal Q2 earnings per share of $12.20 versus $9.31 expected a 31% beat. Revenue came in at $23.86 billion, nearly tripling from $8.05 billion a year ago and crushing the $20.07 billion consensus. Gross margins hit 81%. Free cash flow set a record. The board approved a 30% dividend hike. And the Q3 guide? $33.5 billion in revenue versus Street expectations of $24.3 billion. That single-quarter guidance exceeds Micron's entire annual revenue for every fiscal year through 2024.

The story is HBM high-bandwidth memory and the structural supply crunch driving it. Micron's full calendar-year 2026 HBM supply is completely sold out. CEO Mehrotra said some key customers are receiving only 50% to two-thirds of what they're requesting. Volume production of HBM4 for Nvidia's Vera Rubin platform has begun, and the company signed its first five-year Strategic Customer Agreement a signal that customers are locking in multi-year commitments because they can't afford not to. Among the ten most valuable U.S. tech companies, Micron is the only one in the green this year up 62% YTD while Oracle leads the losers at –22%.

And yet the stock slipped about 4% after hours. Some of that is capex anxiety fiscal 2026 spend is above $25 billion, with fiscal 2027 stepping up "meaningfully" with over $10 billion in additional construction costs. But most of it was timing. Iran struck Qatar's LNG infrastructure during the earnings call. Micron's conference call literally got photobombed by a geopolitical escalation. It's the perfect encapsulation of this market: the best AI story in semis can't outperform a war. The bull case is that demand is structurally insatiable and margins are durable. The bear case is that even a perfect quarter gets you a sell-the-news reaction when Brent is at $113 and the Fed just told you rate cuts are off the table.

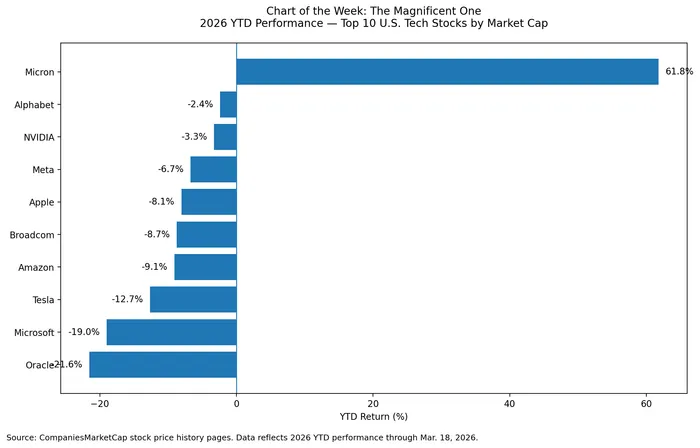

Chart of the Week: The Magnificent One

Micron vs. the rest of the top-10 U.S. tech stocks — 2026 YTD performance

Among the ten largest U.S. tech companies by market cap, Micron is up 62% year-to-date. Every other name is red. Oracle is down 22%. Microsoft and Tesla have posted double-digit declines. The "Magnificent Seven" have become the "Magnificent One" and it's a memory chip company riding AI demand that nobody would have put at the top of their 2026 prediction list.

The Hive Mind

FinTwit is in full stagflation debate mode the 1970s OPEC comparisons are everywhere, and the "oil above $100 kills the bull market" crowd is getting louder. Over on r/wallstreetbets, the Micron earnings thread was a mess of confusion — half the sub celebrating the blowout, the other half watching their calls evaporate on the after-hours dip. The most upvoted comment: "MU could cure cancer and still trade flat." Some things never change.

The Thread

Two stories, one collision. The best AI earnings quarter in semiconductor history happened on the same day the Fed admitted it can't cut rates because of an energy war, while Iran was literally attacking LNG infrastructure during the conference call. This market is being pulled in two directions at once structural AI demand that is genuinely unprecedented, and a geopolitical oil shock that is repricing the entire macro outlook in real time. The question isn't which force wins. It's what happens to the companies caught in between the ones that aren't Micron, don't have structural scarcity, and now have to navigate both rising input costs and a Fed that just took away the safety net. That's where the next shoe drops.

Senior strategist with 20+ years experience delivering data-driven research, ETF and stock analysis, and practical investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet