Killer Bees — Market Brief March 05, 2026

The Sting

Iran didn't need a navy to close the Strait of Hormuz. It needed a few drones and a phone call. Meanwhile, BlackstoneBX-- just let investors pull a record $3.8 billion from its flagship credit fund and called it "meeting 100% of redemption requests" which is technically true in the same way that a bank run is technically a withdrawal. Two very different markets, one uncomfortable theme: what happens when the thing that was never supposed to happen actually happens?

The Insurance Blockade

Here's what's wild about the Hormuz situation: the strait isn't formally closed. Iran didn't deploy mines, didn't line up warships, didn't physically block the 21-mile-wide passage between its coastline and Oman. What it did was launch a few selective drone strikes on tankers, transmit a VHF radio warning that any vessel passing through would be set ablaze, and wait.

That was enough. Tanker transits dropped from an average of 24 per day in January to four on March 1 three of which were flying Iranian flags. By March 2, zero tankers broadcast AIS signals in the strait. Not because Iran achieved naval superiority, but because the insurance industry did the work for them. Protection and indemnity coverage was pulled for March 5. War-risk premiums had already spiked from 0.125% to 0.4% of hull value per transit an extra quarter-million dollars for a single VLCC crossing. No insurer, no voyage. It's a blockade by spreadsheet.

The market reaction has been strangely measured. Brent is at $84. That's up 10-13% from pre-conflict levels, sure, but this is 20% of global oil supply we're talking about. J.P. Morgan estimates 329 tankers stuck in the Gulf. Iraq is shutting down production at its Rumaila oil field because it literally has nowhere to put the oil it's pumping. Qatar halted LNG production after Iranian strikes hit its facilities. European natural gas futures nearly doubled before pulling back. And yet Brent isn't at $100.

Why the restraint? A few reasons. Global stockpiles were healthy going in. China has buffer inventory. And traders are pricing in a short conflict, Trump suggested four to five weeks. His offer to provide U.S. Navy escorts and government-backed insurance for tankers trimmed the intraday spike on Tuesday (Brent pulled back from +9% to settle at $81.40). But here's the question nobody's asking: what if the insurance market doesn't come back even after the shooting stops? Shipping companies don't un-learn risk. The Houthis resumed Red Sea attacks the same weekend. The risk map for global energy transit just got permanently redrawn, and the premium for that doesn't go away when a ceasefire is announced. RBC's Helima Croft compared this to the 1970s oil embargo. That might be hyperbolic. But the mechanism choking supply through logistics rather than production is genuinely novel, and nobody has a playbook for it.

The Quiet Run

While everyone was watching oil prices, something arguably more consequential for the average investor was unfolding in private credit. Blackstone disclosed that investors sought to redeem a record 7.9% of its $82 billion flagship private credit fund, BCRED roughly $3.8 billion. That's well above the fund's standard 5% quarterly cap. Blackstone raised the limit to 7%, then had its own employees invest $400 million to cover the rest. They're framing it as conviction. The market heard something else: BXBX-- shares dropped 8.5% intraday Tuesday.

This isn't an isolated event. It's the third wave. Blue Owl scrapped quarterly redemptions in its OBDC II fund last month, switching to periodic payouts funded by asset sales. (They sold $1.4 billion in loans at 99.7 cents on the dollar good execution, but the fact that they had to is the story.) Blue Owl's tech-focused fund saw 15.4% redemptions in its most recent quarter. KKR is down 12% in the past two weeks. Ares fell 8%. The entire alt-manager complex is repricing.

What's driving it? Three things braided together. First, the Blue Owl situation spooked retail wealth advisors, and once advisors start calling in redemptions, the herd follows. Second, there's growing anxiety about private credit's exposure to software companies roughly 25% of BCRED's portfolio as AI threatens to erode traditional SaaS business models. Third, and most structurally: rates are still high, and public credit is suddenly competitive. Why lock up money in a semi-liquid BDC yielding 9.8% when you can buy investment-grade corporates yielding 5-6% with daily liquidity?

Carlyle CEO Harvey Schwartz said the quiet part loud back in December: the industry should probably stop calling these products "semi-liquid" and start calling them "sometimes not liquid at all." RA Stanger is forecasting a 40% year-over-year decline in BDC capital formation for 2026. The era of easy retail capital flowing into private credit might be over or at least entering a very uncomfortable adolescence.

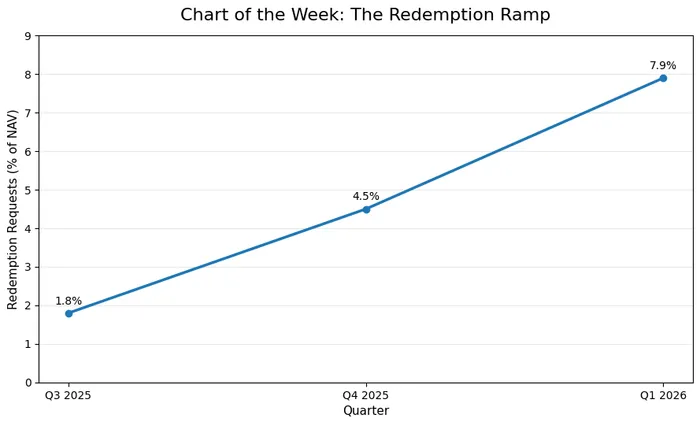

Chart of the Week: The Redemption Ramp

BCRED quarterly redemption requests as % of NAV

That's a near-perfect exponential ramp. Each quarter roughly doubles the prior one. If you drew this line on any other chart a stock, a commodity, a macro indicator you'd call it a trend, not noise. The 5% quarterly cap that was supposed to be a guardrail was breached for the third time. Blackstone's global head of private credit said investors "should never buy these products if they expect 100% liquidity." He's right. But the marketing sure didn't emphasize that part. The BDC industry grew from $127 billion to $451 billion in assets since 2020. That's a lot of money that came in through a door marked "semi-liquid" and is now discovering what that hyphen actually means.

The Hive Mind

FinTwit is split into two camps this week. The energy crowd is screaming $100 oil and posting Strait of Hormuz maps like it's fantasy football. The private credit corner is quieter but more anxious a lot of advisors are asking whether they should be pulling clients out of BDCs before the next quarter's gates hit. The interesting contrarian signal: Steve Eisman ("The Big Short") went on CNBC Monday and said he wouldn't change a single trade because of Iran. "Long term, this is very, very positive," he said. The man who shorted housing in 2007 thinks the biggest oil disruption in 50 years is a buying opportunity. Make of that what you will.

The Thread

Two stories, one word: liquidity. Iran proved you don't need to physically block a strait you just need to make it uninsurable. Private credit is learning the same lesson in reverse: you can promise periodic liquidity, but when everyone wants it at once, "periodic" starts to feel like "theoretical." In both cases, the architecture worked exactly as designed, right up until it didn't. The question for 2026: where else has liquidity been promised but not stress-tested?

Senior strategist with 20+ years experience delivering data-driven research, ETF and stock analysis, and practical investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet