Killer Bees — Market Brief February 19, 2026

The Sting

Blue Owl Capital permanently locked retail investors inside a private credit fund on the same week Warren Buffett's final 13-F revealed he's been sprinting toward the exits with $381.6 billion in cash. One group of investors can't get their money out. The other the greatest allocator in history won't put his in.

Deep Dive #1: Blue OwlOWL-- Locks the Exits

Blue Owl Capital told investors in its retail-focused OBDC II fund that quarterly redemptions are done. Not paused permanently halted. The firm reversed its own plan to resume withdrawals this quarter, replacing them with "periodic distributions" funded by asset sales. OWL dropped 2.3% on the news. The stock is down 33% year-to-date.

Here's what most coverage glossed over: this isn't a surprise it's the final chapter of a slow-motion unraveling. In November, Blue Owl froze redemptions after requests overwhelmed limits. In December, a class action lawsuit was proposed alleging undisclosed liquidity issues. In January, the firm had to allow 17% redemptions on a separate tech-focused BDC after a "deluge" of withdrawal requests blew past the normal 5% cap. Now? The door is welded shut.

The numbers paint a grim picture. Blue Owl sold $1.4 billion in loans across three funds $600 million from the retail fund alone, roughly 30% of its assets to pension funds and insurers at 99.7 cents on the dollar. That's an orderly liquidation dressed in a press release. Meanwhile, Blue Owl's founders reportedly pledged $1.9 billion in personal OWL shares as collateral for loans. Redemption pressure surged 20% year-over-year through the first nine months of 2025.

The question nobody's asking: if a $307 billion alternatives manager can't manage retail redemptions, what's happening at the dozens of smaller private credit shops that don't make Bloomberg? Wall Street spent five years selling "democratized alternatives" to retail investors. Blue Owl is what happens when the pitch meets the plumbing. The whole value proposition quarterly liquidity in illiquid assets works beautifully until it doesn't. And when it doesn't, there's no secondary market, no circuit breaker, just a locked gate and a letter from legal.

Deep Dive #2: Buffett's Last 13-F — The Oracle Votes With His Wallet

Berkshire's Q4 filing read like a farewell written in sell orders. In his final quarter as CEO, Buffett slashed Amazon by 75%, trimmed Apple by another 4.3%, cut Bank of America by 9% and made exactly one new bet: a $352 million stake in The New York Times. NYT hit an all-time high. Greg Abel inherits the keys January 1 and a record $381.6 billion cash pile that is either the world's most expensive parking lot or the greatest dry powder position ever assembled.

The NYT pick got the sentimental headlines paper boy buys a newspaper but the real story is what Buffett didn't buy. He's been a net seller for quarters. He looked at this entire market, at 22x forward earnings, at the AI capex arms race, at $600 billion in hyperscaler spending commitments and said: I'll take 4% in T-bills, thanks.

Connect this to Blue Owl and it gets uncomfortable. Buffett is hoarding liquidity at the exact moment retail investors in private credit are discovering they have none. He added to Chevron (up 19% YTD on the Venezuela play) and bought a subscription-revenue media company with zero AI capex exposure. Every move screams the same thing: cash optionality over locked-up yield. Smart money and trapped money have never been further apart.

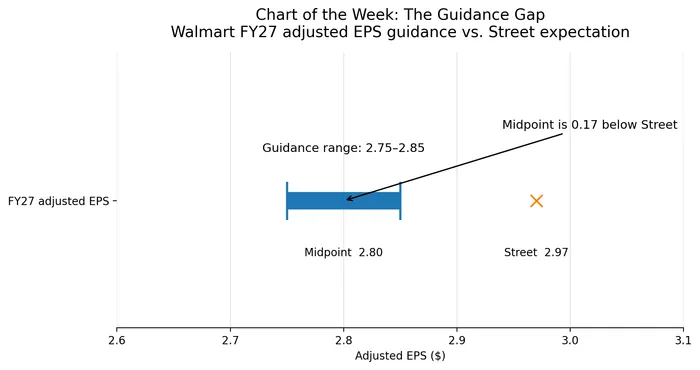

Chart of the Week: The Guidance Gap

Walmart beat the quarter. The Guidance Miss Nobody Cared About

Walmart posted a clean beat revenue up 5.6%, e-comm up 27%, Walmart Connect ads up 41% then guided FY27 EPS to $2.75–$2.85 versus the $2.97 Wall Street wanted. New CEO John Furner cited a "fluid" trade and labor backdrop. The stock dropped 3% in premarket… then reversed to trade up 2% as of this publishing. A 5-point swing on a $1 trillion name. The market looked at conservative guidance and decided it was sandbagging, not warning. That's either smart pattern recognition new CEOs always low-ball their first guide or a market so desperate for quality it'll forgive anything from the winners. Either way: investors aren't selling Walmart. They're hiding in it.

The Hive Mind

FinTwit lit up on Blue Owl, with Arthur Hayes posting "Warm up that printer, Powell" reading the redemption halt as a sign of systemic liquidity stress. The Buffett cash pile is getting the usual two readings: genius defensive positioning or a 94-year-old who simply lost his fastball.

The Thread

Two funds, two postures, one theme. Blue Owl's investors are locked in a room with no door. Buffett is standing in a room full of doors and choosing not to walk through any of them. Walmart just warned you the hallway ahead is dark and the market bought the dip anyway. The question isn't whether liquidity matters. It's whether the people who need it most will figure that out before the lights go off.

Senior strategist with 20+ years experience delivering data-driven research, ETF and stock analysis, and practical investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet