Killer Bees Market Brief April 09, 2026

The Sting

Here's a fun exercise: try to withdraw a fifth of your money from a $36 billion fund. Blue OwlOWL-- investors did exactly that in Q1. They got a quarter of what they asked for. The fund's fine, management says. The loans are performing. So why is everyone trying to leave?

The Slow-Motion Queue at the Exit

Here's what happened. Moody's cut its outlook on Blue Owl Credit Income Corp (OCIC) to negative on Tuesday, citing "significantly higher-than-peer redemption requests" in Q1. The numbers tell the story better than the rating action does: investors asked to pull nearly 22% of OCIC's shares. At Blue Owl's technology-focused vehicle, the number was 40.7%. Both funds capped withdrawals at 5%. So roughly four out of every five dollars that wanted out... didn't get out.

Blue Owl says the requests came from a "very limited number of investors." Moody's flagged that concentration as its own risk if a few big holders are spooked, and they can't leave, they'll just re-queue next quarter. And the quarter after that. This isn't a bank run in the classic sense, because there's a gate.

This isn't just Blue Owl. Moody's revised its outlook on the entire U.S. BDC sector to negative all $400 billion of it. S&P already cut Cliffwater's $33 billion fund to negative in March. Morgan Stanley, JPMorgan, BlackRock all capping redemptions somewhere. Nearly $14 billion in redemption requests hit BDCs in early 2026. The private credit industry sold itself to retail and wealth investors on a simple premise: bank-like yields without bank-like volatility. The asterisk was always liquidity. Quarterly redemption windows sound fine until everyone shows up at the same window.

The strange part? The actual loans look fine. Non-accruals at 0.6% of cost among the lowest in the peer group. This isn't people fleeing bad credit. It's people fleeing the structure itself. They don't trust the marks, they don't trust the gates, and they definitely don't trust that the exit will still be open six months from now if something actually breaks.

The $1 Trillion Insurance Bet You Didn't Know You Made

So where did all this private credit end up? Partially in your insurance policy. U.S. life insurers now hold nearly $1 trillion in private credit roughly one-sixth of their total investment assets. About $280 billion of that barely maintains investment-grade status. Another $70 billion is already junk.

The dollar figure is one thing. The plumbing is another. PE-owned insurers are using structures called "rated note feeder funds" to repackage private credit as investment-grade. An NAIC report found some ratings were inflated by six notches. The report was quietly taken down nearly a year ago. And at PE-owned insurers, related-party investments now average 76% of surplus meaning the same shop that originates the loan also manages the insurer that buys it. Nobody in that chain has an incentive to say the asset is worth less than what's on the books.

Treasury Secretary Bessent has been flagging this since February, warning that retirement accounts shouldn't become "a dumping ground" for "rotten assets." Treasury is now convening state and international insurance regulators through early May. But insurance is regulated at the state level 50 different regulators, no unified federal authority. Treasury can host a meeting. It can't write a rule. The NAIC's own president has flagged transparency in life insurance portfolios as a top 2026 priority, which tells you how much transparency currently exists: not enough for the regulators themselves.

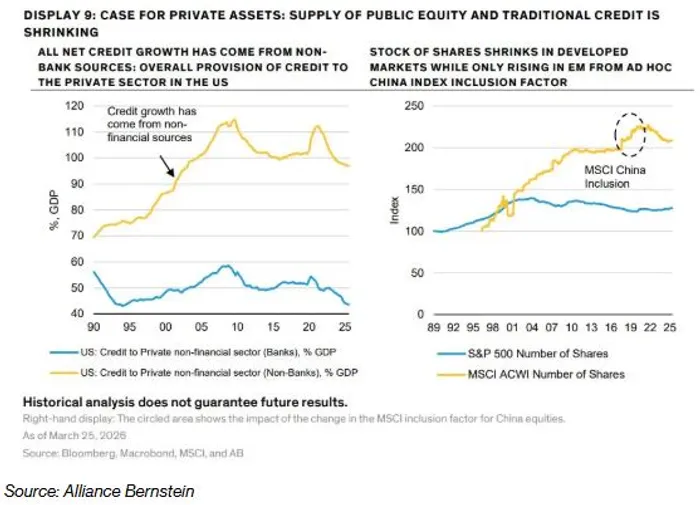

Chart of the Week: The Quiet Takeover

Source: Alliance Bernstein, Inigo Fraser-Jenkins. March 25, 2026.

Looking at the left panel, every dollar of net credit growth to the U.S. private sector is now coming from non-banks. Bank lending as a share of GDP has basically gone nowhere. On the right the stock of publicly listed equity is shrinking. S&P 500 share count has been falling for years. The ACWI only looks flat because MSCI added China. Take that out and global public equity supply is contracting. Private credit isn't some niche in an alternatives allocation. It's become the backbone of how American companies actually get financed.

The Hive Mind

FinTwit is split. The "this is 2008 again" crowd is loud but not particularly specific about which loans are going bad (answer: not many, yet). The more interesting thread is from credit analysts pointing out that the real risk isn't defaults it's what happens to manager economics when AUM shrinks 5% a quarter for a year straight. Blue Owl shares hit record lows.

The Thread

Two stories, one theme: private credit wasn't sold as private credit. It was sold as yield-with-liquidity, and the liquidity part is turning out to be fiction. When a trillion dollars of that fiction is sitting inside insurance companies backing your annuity rated by agencies that may have inflated scores by six notches, overseen by 50 state regulators with no shared playbook you don't need a default cycle. You just need people to ask: what are these things actually worth?

Senior strategist with 20+ years experience delivering data-driven research, ETF and stock analysis, and practical investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet