KeyBank's ESG Opaque Practices: A Cautionary Tale for Investor Trust and Shareholder Value

In the evolving landscape of corporate governance, ESG (Environmental, Social, and Governance) transparency has emerged as a cornerstone of investor trust and long-term value creation. Yet, KeyBank's recent refusal to release the findings of its 2024 racial equity audit has sparked a crisis of credibility, raising urgent questions about the bank's commitment to accountability and its ability to compete in an era where stakeholders demand measurable progress on social equity. This case study underscores how opaque ESG practices can erode investor confidence, damage reputations, and ultimately undermine financial performance.

The Audit That Wasn't: A Governance Misstep

KeyBank's decision to withhold the results of its racial equity audit—conducted by Covington & Burling LLP—has drawn sharp criticism from community groups, investors, and ESG-focused stakeholders. The bank's assertion that the audit found “no significant issues” rings hollow in the context of its historical underperformance in lending to Black and low- and moderate-income (LMI) borrowers. As the National Community Reinvestment Coalition (NCRC) pointed out, KeyBank's audit was a reactive measure, initiated only after pressure from shareholders and advocacy groups, not a proactive step toward addressing systemic inequities.

The lack of transparency is particularly damaging in a post-SCOTUS affirmative action landscape, where financial institutionsFISI-- are under heightened scrutiny to demonstrate tangible progress in DE&I (Diversity, Equity, and Inclusion) initiatives. By refusing to share the audit's findings, KeyBank has failed to meet the expectations of stakeholders who view ESG disclosures as a critical component of corporate accountability. This opacity contrasts starkly with the strategies of peers like U.S. Bank and PNC, which have adopted proactive ESG disclosure frameworks aligned with global standards such as the Global Reporting Initiative (GRI) and the Task Force on Climate-related Financial Disclosures (TCFD).

Investor Trust in Jeopardy

Empirical studies underscore the direct link between ESG transparency and investor confidence. A 2024 study published in the Journal of Management & Governance found that voluntary ESG disclosures reduce idiosyncratic volatility and downside tail risk, particularly in the early stages of public market participation. For KeyBank, the absence of such disclosures has likely exacerbated uncertainty among investors.

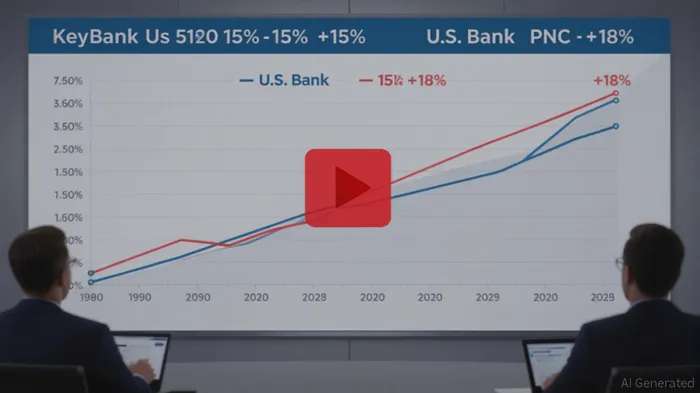

The data tells a clear story: KeyBank's stock underperformed its regional bank peers in 2025, with a 12-month trailing return of -8% compared to U.S. Bank's +15% and PNC's +18%. This underperformance reflects broader concerns about the bank's ESG governance and its readiness to adapt to shifting regulatory and social norms. As ESG-linked assets surpass $50 trillion globally, investors are increasingly prioritizing institutions that demonstrate transparency and measurable progress on social and environmental issues. KeyBank's reluctance to share audit results risks alienating a growing segment of the market.

A Broader Risk for Financial Institutions

KeyBank's case is not an isolated incident but a symptom of a larger challenge facing financial institutions: the tension between reputation management and substantive action. While the bank's leadership has emphasized its “commitment to fostering an inclusive culture,” the absence of concrete evidence—such as the audit's findings—has fueled perceptions of deflection. This aligns with findings from a 2021 study on ESG-washing in the mutual fund industry, which highlighted how misaligned rhetoric and action can erode trust and invite regulatory scrutiny.

The risks extend beyond investor relations. Regulatory bodies are increasingly scrutinizing ESG disclosures for accuracy and completeness. The EU's Corporate Sustainability Reporting Directive (CSRD) and U.S. SEC guidelines, for instance, mandate standardized ESG reporting, penalizing institutions that fail to meet transparency benchmarks. KeyBank's opaque approach could expose it to heightened regulatory risk, particularly as global standards for ESG reporting converge.

Lessons from the Competition

In contrast to KeyBank's approach, institutions like Standard Chartered, Bank of AmericaBAC--, and HSBCHSBC-- have demonstrated how transparent ESG practices can drive both trust and financial performance. Standard Chartered's 2025 Transition Plan, for example, set science-based targets for reducing emissions and was externally verified to build credibility. Similarly, Bank of America's $300 billion commitment to sustainable financing by 2030 has positioned it as a leader in ESG-linked lending, attracting capital from ESG-focused investors.

These case studies reinforce the importance of aligning ESG strategies with measurable, publicly disclosed goals. By embedding transparency into their governance frameworks, these institutions have not only strengthened stakeholder trust but also enhanced their competitive positioning in a market where ESG performance is increasingly tied to valuation metrics.

Investment Implications and Recommendations

For investors, KeyBank's ESG governance risks present a cautionary tale. The bank's refusal to release the audit results signals a lack of alignment with the expectations of a market that increasingly values transparency and accountability. While KeyBank's core financials remain stable, its ESG-related risks could weigh on long-term shareholder value, particularly as ESG factors become more integrated into credit ratings and investment decisions.

Investors should consider the following:

1. Due Diligence on ESG Disclosures: Scrutinize the quality and completeness of ESG reporting when evaluating financial institutions. KeyBank's opacity contrasts sharply with the detailed disclosures of its peers.

2. Diversification: Allocate capital to institutions with robust ESG frameworks, such as U.S. Bank or PNC, which have demonstrated a commitment to transparency and measurable progress.

3. Engagement: Advocate for stronger ESG governance practices through shareholder engagement, pressuring KeyBank to adopt standardized reporting and share audit findings.

In the long term, financial institutions that prioritize transparency over reputation management will be better positioned to navigate the evolving ESG landscape. KeyBank's current approach, however, suggests a misalignment with the expectations of a market that increasingly values accountability. As ESG governance becomes a critical determinant of competitive advantage, the bank's reluctance to embrace transparency could prove costly for both its stakeholders and its shareholders.

In conclusion, KeyBank's refusal to release its racial equity audit results highlights the growing risks of opaque ESG practices in an era where transparency is non-negotiable. For investors, the lesson is clear: ESG governance is not just a compliance exercise but a strategic imperative that shapes trust, regulatory outcomes, and long-term value. Institutions that fail to adapt risk being left behind in a market that rewards accountability and penalizes ambiguity.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet