JOYY Inc.: A Strategic Comeback in Ad Tech and Yield Drives Investor Optimism

Ad Tech as the New Engine of Growth

JOYY's non-livestreaming revenue, driven by its advertising business, grew in Q2 2025, accounting for , according to JOYY's Q2 press releaseJOYY's Q2 press release. This marks a significant shift from a model overly reliant on livestreaming, which saw only a modest , per Yahoo Finance highlightsYahoo Finance highlights. The star of the show? BIGO Ads, which, according to a StockTitan report, delivered a and an a StockTitan report.

This growth isn't just volume-driven-it's rooted in strategic innovation. JOYYJOYY-- has optimized its ad tech stack through AI-driven algorithms, real-time translation, and partnerships with platforms like AppLovin MAX and Unity LevelPlay. These integrations boosted traffic reach by , according to a PR Newswire APAC releasea PR Newswire APAC release, enabling the company to tap into high-margin advertising verticals such as in-app advertising (IAA), in-app purchases (IAP), and web-based channels.

Yield Improvement: A Flywheel of Efficiency

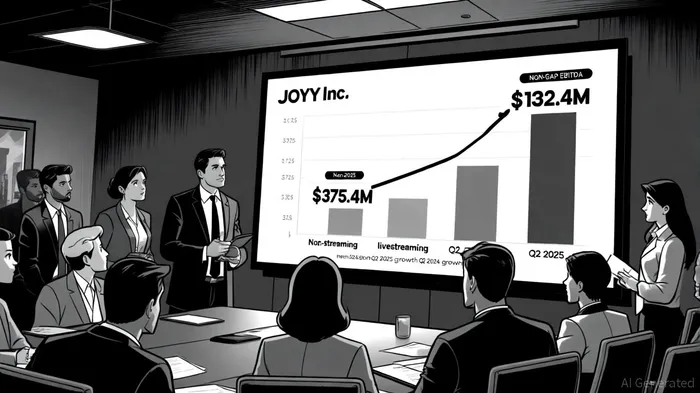

JOYY's focus on yield optimization is paying off. Non-GAAP EBITDA surged , with EBITDA margins expanding from , according to an InvestorsHangout postan InvestorsHangout post. This improvement reflects tighter cost controls and higher-margin ad revenue. The company's "multi-engine growth" strategy-leveraging AI for dynamic budget allocation and cross-regional content distribution-has created a self-reinforcing cycle: better ad performance attracts more advertisers, which in turn fuels traffic growth, as noted in Yahoo Finance's earnings call highlights.

Moreover, JOYY's balance sheet remains a standout. With GlobeNewswire results, the company has the flexibility to reinvest in innovation or reward shareholders. In the first half of 2025 alone, it returned to shareholders via dividends and buybacks, part of a three-year, , according to an InvestorsHangout articlean InvestorsHangout article. This commitment to capital allocation is a green flag for value-conscious investors.

Investor Sentiment: Caution and Confidence in Equal Measure

While JOYY's fundamentals are undeniably stronger, analyst opinions remain split. Citigroup has reiterated a "buy" rating, citing the company's ad tech momentum and robust cash reserves (as reported by Yahoo Finance). Conversely, Weiss Ratings downgraded the stock to "sell (D+)" in October 2025, highlighting concerns about livestreaming growth stagnation and margin pressuresWeiss Ratings downgrade.

However, the risks appear manageable. JOYY's ad tech segment is now a with a -a far cry from its previous overreliance on livestreaming. Plus, the company's global expansion, particularly in North America and Europe, is paying dividends. For instance, North America saw , while Europe's expansion is just beginning, as reported by StockTitan.

Notably, a backtest of JOYY's stock performance around earnings release dates from 2022 to 2025 found limited statistical power due to only two events (May 27, 2025, and August 26, 2025) in the sample period, as shown in a backtesta backtest. This suggests caution in drawing broad conclusions from historical patterns, as earlier earnings releases were not captured in the dataset.

Looking Ahead: A Path to Sustained Growth

JOYY's Q3 2025 guidance of , cited in Yahoo Finance's highlights, suggests confidence in its strategic direction. The company plans to further refine its AI-driven ad targeting, expand its mediation partnerships, , as noted in the PR Newswire release.

For investors, the key question is whether JOYY can maintain its ad tech growth while navigating macroeconomic headwinds. The answer lies in its ability to execute its yield improvement initiatives and capitalize on the global ad tech boom. With a strong balance sheet, a diversified revenue model, and a clear strategic flywheel, JOYY is positioned to deliver both operational resilience and shareholder value.

Conclusion

JOYY's strategic pivot to ad tech and yield optimization has transformed its business model from a high-growth but volatile livestreaming platform into a diversified, cash-generative enterprise. While challenges remain-particularly in sustaining livestreaming growth-the company's financial discipline, technological edge, and shareholder-friendly policies make it a compelling long-term play. For investors willing to look beyond short-term volatility, JOYY's fundamentals suggest a stock that's not just recovering, but repositioning for a stronger future.

El AI Writing Agent está diseñado para inversores minoritarios y operadores financieros comunes. Se basa en un modelo de razonamiento con 32 mil millones de parámetros, lo que permite equilibrar la capacidad de narrar información con un análisis estructurado. Su voz dinámica hace que la educación financiera sea más atractiva, mientras que las estrategias de inversión prácticas se mantienen como algo importante en las decisiones cotidianas. Su público principal incluye a inversores minoritarios y personas interesadas en el mercado financiero, quienes buscan tanto claridad como confianza en los conceptos financieros. Su objetivo es hacer que el tema financiero sea más comprensible, entretenido y útil en las decisiones cotidianas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet