Jobless Claims Signal Labor Market Resilience: A Contrarian Play in Cyclical Stocks

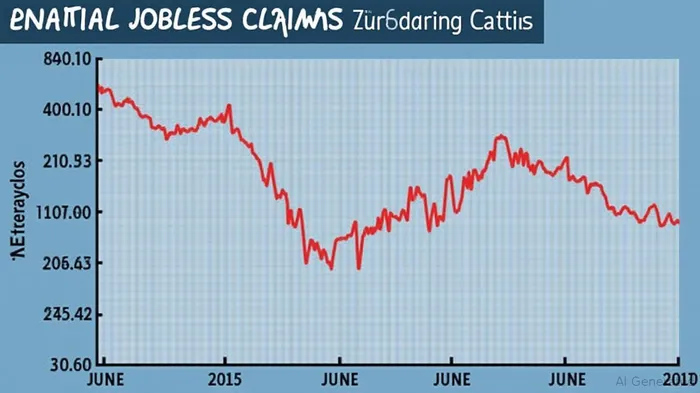

The latest unemployment claims data for the week ending June 21, 2025, offers a critical clue for investors seeking contrarian opportunities in economically sensitive sectors. Seasonally adjusted initial jobless claims fell to 236,000—a 10,000 drop from the prior week and well below the 244,000 consensus estimate—marking the lowest level since February 2024. This robust reading, paired with a declining four-week moving average of 245,000, underscores a labor market far more resilient than the recession fears currently plaguing markets. For investors, this is a green light to re-risk portfolios into undervalued cyclical sectors like industrials and materials, which have been unfairly punished by macro pessimism.

The Contrarian Case: Low Layoffs = Corporate Health

The obsession with “peak earnings” and “rolling recessions” has led investors to overlook a basic truth: companies aren't laying people off. Initial jobless claims—a leading indicator of labor market health—have now averaged below 250,000 for 52 consecutive weeks, a streak not seen since the late 1960s. This signals that employers, even in sectors like retail and tech, remain reluctant to reduce headcount despite profit pressures. Why? Because demand, while muted, is still sufficient to justify retaining workers.

This dynamic matters most for cyclical sectors. Industries like industrials and materials rely on sustained demand from manufacturers, construction firms, and exporters. Persistent low layoffs suggest that end-market demand is holding up, even if growth is tepid. For example, industrial companies like CaterpillarCAT-- or 3MMMM--, which have seen their stocks languish on recession fears, could see earnings beat estimates if their customers' hiring stability translates to steady orders.

Navigating the Noise: Why Rising Continuing Claims Don't Tell the Whole Story

Critics may point to the rise in continuing unemployment claims to 1.974 million—the highest since November 2021—as a sign of labor market softening. But this metric is a lagging indicator. The increase likely reflects structural factors: severance packages delaying benefit eligibility for some federal workers (e.g., those affected by the Department of Government Efficiency's reforms) and a prolonged post-pandemic adjustment period where workers are slower to exit unemployment. The Fed's recent decision to hold rates steady, citing “labor market resilience,” reinforces this view.

The Investment Play: Re-Risk into Undervalued Cyclical Equities

The data suggests now is the time to rotate into industrials and materials. Consider:

1. Valuations are cheap relative to fundamentals. The price-to-earnings ratio of the S&P Industrials Index is 16.8x, below its five-year average of 19.2x, despite consistent cash flow.

2. Supply chain stability. Low layoffs in logistics and manufacturing sectors reduce the risk of disruptions, a key concern for investors in 2023.

3. Inflation tailwinds for materials. While headline inflation is moderating, commodities like copper and steel—critical for construction and manufacturing—are gaining traction as China's stimulus and U.S. infrastructure spending picks up.

Stocks to consider:

- Caterpillar (CAT): Exposed to global construction and mining markets, its valuation is 13.5x forward earnings, down from 16.5x in early 2024.

- United States Steel (X): Materials stocks have underperformed broader indices, yet steel demand from autos and infrastructure could rebound.

- Deere (DE): Agriculture equipment sales often correlate with farm profitability, which remains strong despite input cost pressures.

Risks and the Fed's Role

The Fed's caution on inflation and employment is a double-edged sword. While low jobless claims support the case for re-risking, the central bank's reluctance to cut rates could limit gains. Investors should monitor the four-week moving average of initial claims: a sustained rise above 260,000 would signal a meaningful slowdown.

Conclusion: The Labor Market is the Canary—It's Singing Resilience

The data is clear: the labor market isn't collapsing. Initial jobless claims remain a bright spot in an otherwise gloomy macro picture. For investors, this is a contrarian opportunity to buy into industrials and materials at discounted valuations, positioning for a recovery in economic sensitivity. The path forward isn't without risks, but the labor market's resilience suggests the economy—and these sectors—are far from done.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet