Jerome Powell Set to Deliver Big Speech at Jackson Hole Conference: Here’s What to Expect

As the crisp mountain air of Wyoming's Grand Teton National Park envelops the gathering of global economic elites, the Federal Reserve's annual Jackson Hole symposium kicks off with a sense of urgency unmatched in recent years. Central bankers, economists, and market watchers have descended on this remote venue, where policy whispers can ripple into market tsunamis.

At the heart of it all is Fed Chair Jerome Powell's Friday morning address, a moment poised to shape not just the trajectory of U.S. interest rates but the broader narrative of economic resilience amid political turbulence and lingering inflationary pressures. With the U.S. economy at a crossroads—hiring slowing, tariffs looming, and political barbs flying—the stakes couldn't be higher.

The Conference Theme, Panels, and Key Attendees

This year's symposium, hosted by the Kansas City Fed, revolves around the theme of "labor markets in transition," a timely lens for dissecting how evolving workforce dynamics are reshaping monetary policy worldwide. The agenda blends academic rigor with high-stakes dialogue, featuring a lineup of panels and papers that probe the intersections of demographics, technology, and economic stability.

Friday's sessions open with Nobel laureate Claudia Goldin presenting her research on global fertility declines and their implications for labor supply, a topic that underscores the long-term challenges facing aging populations. Following her, University of Michigan's Linda Tesar will delve into the economic fallout from diminishing labor-market mobility in the U.S., highlighting how reduced worker movement stifles growth and innovation.

The day rounds out with a panel on technology's role in labor markets, featuring insights from University of Chicago's Ufuk Akcigit, Harvard's Lawrence Katz, and Columbia's Laura Veldkamp—experts whose work could inform how AI and automation are upending traditional employment models.

Saturday shifts focus to broader policy dilemmas, with UC Berkeley's Emi Nakamura exploring central banks' responses to inflation spikes, and Harvard's Ludwig Straub analyzing U.S. debt sustainability amid rising deficits. The marquee international panel will bring together Bank of England Governor Andrew Bailey, ECB President Christine Lagarde, and Bank of Japan Governor Kazuo Ueda to discuss the theme's global ramifications, offering a rare window into coordinated—or divergent—policy approaches.

Attendance reads like a who's who of economic power brokers. All 18 Fed policymakers are present, though only Powell is slated for a major speech; others, like Boston Fed President Susan Collins, will field media interviews. International heavyweights include Bundesbank President Joachim Nagel and European Commissioner Valdis Dombrovskis.

Former Fed luminaries such as Ben Bernanke, Don Kohn, Roger Ferguson, and Alan Blinder add historical gravitas, while White House Council of Economic Advisers members Pierre Yared and Aaron Hedlund represent the administration's perspective. In a departure from tradition, Alphabet's Ruth Porat delivers the Friday lunch keynote—the first private-sector speaker since 2008—potentially injecting tech-sector insights into the central banking discourse.

Fed Policy Shifts: Rate Cuts, Inflation Battles, and Political Badgering

Powell's speech, titled "Economic Outlook and Framework Review," arrives at a pivotal juncture for Fed policy. The central bank is wrapping up its quinquennial review of its operational framework, implemented in 2020 amid the pandemic's chaos. That shift introduced "flexible average inflation targeting," allowing inflation to overshoot the 2% goal to bolster employment, especially for underrepresented groups. Critics argue it contributed to the Fed's delayed response to the post-Covid price surge, which peaked at levels unseen in four decades. Expect Powell to signal a rollback, restoring a preemptive stance against inflation rises and emphasizing symmetry in addressing deviations from the target.

On the immediate horizon, the September FOMC meeting looms large. After holding rates steady since December, the Fed faces a delicate balance: inflation hovers closer to 3% than 2%, yet labor indicators soften, with July's job growth anemic and revisions painting a weaker picture. Market pricing anticipates a quarter-point cut next month, potentially followed by another before year-end, but internal divisions persist.

Governors Christopher Waller and Michelle Bowman lean toward action, while regional presidents like Kansas City's Jeffrey Schmid, Cleveland's Beth Hammack, and Atlanta's Raphael Bostic express caution, insisting on "definitive data" before easing. Schmid, in particular, warns that the "last mile" to 2% inflation remains arduous, and Hammack stresses the need for "modestly restrictive" policy amid dual mandate strains.

Complicating matters is relentless pressure from President Donald Trump, whose administration has escalated attacks beyond mere rate demands. Trump has called for aggressive cuts—up to half a point in September—while lambasting the Fed's headquarters renovation and even targeting Governor Lisa Cook with mortgage fraud allegations, prompting a Justice Department probe. Powell, ever the steady hand, has historically sidestepped direct confrontation, focusing on data-driven decisions and the Fed's dual mandate. Yet analysts speculate he may subtly defend institutional independence, underscoring the perils of political interference in a nod to the institution's sanctity.

Market Reactions: Volatility and Adjusted Expectations

Financial markets, ever attuned to Jackson Hole's signals, have already begun pricing in the uncertainty. Gold, the classic haven asset, slipped 0.3% to $3,337.95 an ounce on Thursday as the dollar firmed 0.4%, rendering bullion pricier for foreign buyers. Traders see limited upside even if Powell affirms a September cut, with much of the dovish pivot already baked in; however, hints of further easing could weaken the greenback and propel gold higher. Silver bucked the trend, rising 0.6% to $38.10, while platinum climbed but palladium dipped.

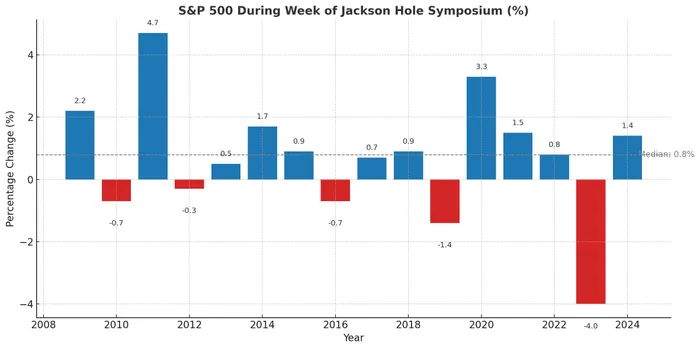

Historically, Bespoke Investment Group team found that dating back to 2009,stock market investors usually can obtain positive returns during the conference week. The median increase of the S&P 500 index was 0.8%. Since then, in 16 symposiums,the stock market only fell five times,in which fell that is greater than 1% only occurred in 2019 and 2022

Rate-cut probabilities have cooled sharply, tumbling from 99% last week to 71.5% for a 25-basis-point trim in September, per tools like CME's FedWatch. This retrenchment follows hotter-than-expected July producer prices (up 0.9% monthly) and hawkish Fed rhetoric, tempering the enthusiasm sparked by softer consumer inflation data. Unemployment claims surged last week, adding to labor worries, yet markets remain vigilant, parsing every nuance for clues on the Fed's path. Goldman SachsGS-- economists anticipate Powell will acknowledge heightened downside risks to employment while downplaying tariff-induced price effects as transitory, without pre-committing to cuts—but signaling readiness if data warrants.

In the shadow of the Tetons, Powell's words will echo far beyond Wyoming's valleys, calibrating expectations for a Fed navigating economic crosswinds and political storms. Whether he opts for caution or conviction, the symposium underscores a central truth: in an era of transitions—from labor shifts to policy recalibrations—the path to stability demands vigilance, independence, and a steady gaze on the horizon. As the conference wraps Saturday, markets will digest the fallout, bracing for what could be a defining pivot in the post-pandemic economy.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet