Jensen's NVIDIA is Scared? Burry's Bubble Bet and the Selloff Reckoning

Jensen Huang is clearly not having a enjoyable time as his company NvidiaNVDA-- is facing Michael Burry's head-on challenge along with AI bubble whispers and competition.

Now, Nvidia stands as both titan and target. The chipmaker's shares have plunged more than 8% since delivering blockbuster quarterly results that shattered Wall Street's loftiest forecasts, erasing gains that briefly crowned it the world's first $5 trillion company. Now trading 17% below its October peak, Nvidia's descent underscores a broader unease: is the AI frenzy a revolutionary gold rush or a precarious house of cards? As short-sellers like Michael Burry circle, and rivals like Google flex their custom silicon muscles, investors are grappling with a narrative shift that pits unbridled optimism against sobering realities.

The Earnings Paradox

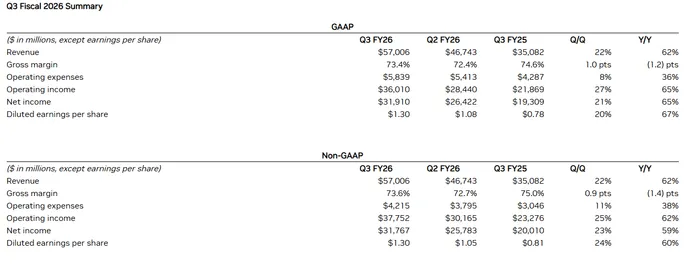

Nvidia's latest quarterly report was a masterclass in dominance. Revenue soared to a record $57 billion, with earnings and guidance trouncing expectations. Jensen Huang, the visionary CEO, painted a picture of insatiable demand for AI infrastructure, dismissing bubble talk as misguided chatter. From his vantage, the surge in data center spending by hyperscalers like Microsoft and Oracle isn't hype—it's the bedrock of a transformative era.

Yet the market's response was a swift rebuke. Shares tumbled, reflecting a disconnect between operational triumphs and investor sentiment. The culprit? A cocktail of concerns that the AI buildout might be overheating. Fears of a capacity glut loom large: if AI adoption falters, tech giants could be saddled with underutilized data centers and mounting debt. Even if demand holds, critics argue the rush to deploy has bred inefficiency, with billions funneled into hardware that may not yield proportional returns.

Compounding this is Nvidia's own strategy of investing in customers, including OpenAI and CoreWeave. These moves, while strategic, evoke ghosts of the dot-com era's vendor financing, where companies propped up demand through circular deals. Carmen Li, CEO of Silicon Data, a GPU market intelligence firm, offers a nuanced take: this isn't a full-blown bubble akin to 2008's leverage-fueled madness, but pockets of overbuild and mispriced expectations warrant caution. Her words resonate in a market where exuberance has given way to scrutiny.

Bubble Fears and Burry's Shadow

No figure embodies the skepticism more than Michael Burry, the prescient investor immortalized in "The Big Short." Burry has wagered over $1 billion against Nvidia and peers like Palantir, labeling the AI ecosystem a web of "circular deals" that mask weak underlying demand. He accuses Nvidia of suspicious revenue recognition, claiming graphics chips depreciate faster than reported and that customer funding loops inflate sales artificially. "Almost all customers are funded by their dealers," Burry quipped on social media, drawing parallels to past frauds.

Nvidia fired back with uncharacteristic vigor, dispatching a memo to analysts that Barron's first revealed. "We are not Enron," the company asserted, rejecting comparisons to the energy giant's debt-hiding debacle or the telecom implosions of WorldCom and Lucent during the dot-com bust. Nvidia emphasized its transparent reporting, debt-free balance sheet, and genuine business model rooted in real demand. Huang echoed this in the earnings call, insisting the AI wave is "very different" from speculative manias.

Burry, undeterred, stood firm: "I stand by my analysis." His critique has amplified market jitters, contributing to Tuesday's 6% drop in Nvidia's stock, which shaved its valuation to around $4.2 trillion. Meanwhile, Alphabet's shares climbed 4%, buoyed by reports of its AI chips gaining traction—a reminder that Nvidia's moat, while deep, isn't impenetrable.

Competition's Rising Tide

The selloff's latest trigger: reports from The Information that Meta Platforms is negotiating billions in deals for Alphabet's AI chips, potentially starting rentals next year and full deployment by 2027. This isn't isolated; Microsoft, Amazon, Alphabet, and Meta have poured resources into custom silicon for years, aiming to curb costs and erode Nvidia's stranglehold on AI accelerators.

Google's Gemini 3 model has fueled optimism that these efforts are bearing fruit. Citi analysts project custom chips swelling to 45% of the AI market by 2028, up from 35% today—a forecast that chips away at Nvidia's narrative of unchallenged supremacy. In a pointed X post, Nvidia congratulated Google on its advances while touting its own generational lead: "Nvidia is a generation ahead of the industry—it's the only platform that runs every AI model and does it everywhere computing is done."

Still, the shift signals a maturing market. Hyperscalers, once captive to Nvidia's ecosystem, are diversifying. Broadcom's role in Alphabet's chip designs adds another layer, hinting at a fragmented landscape where Nvidia's pricing power could erode. Investors aren't just pricing in competition; they're questioning whether the AI infrastructure spend—projected in the trillions—will sustain Nvidia's growth trajectory.

Cramer's Conviction Call

Amid the turmoil, CNBC's Jim Cramer emerges as a bullhorn for resilience. He decries the selloff as "overdone," driven by fear rather than flaws in Nvidia's fundamentals. In Cramer's playbook, AI investing demands steel nerves: "You either believe in artificial intelligence or you should just stay away." He lambasts the herd mentality—buying on highs, selling on dips—that has sidelined many from the Magnificent Seven's epic run.

Drawing from his own regrets, like exiting Alphabet prematurely, Cramer urges patience. Nvidia, like Tesla before it, faces narrative pivots: from EV dominance to autonomy for the latter, and now from chip monopoly to ecosystem architect for Nvidia. The Magnificent Seven—Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla—didn't amass trillion-dollar empires by accident, he argues. Their profits, adaptability, and execution set them apart.

"If you don't like Nvidia, you don't have to own it," Cramer quips. "Nobody's putting a gun to your head." His message: don't let short-term noise eclipse long-term vision. For those with conviction, the dip is an opportunity; for the faint-hearted, safer harbors abound in slower-growth sectors.

Navigating the Storm Ahead

As Nvidia navigates this crossroads, the stakes couldn't be higher. The company's rebuttals and Huang's defiance signal confidence, but the market's verdict remains fluid. Burry's warnings, while contrarian, tap into a vein of doubt about AI's immediacy—will enterprises adopt at the pace tech giants anticipate, or will economic headwinds temper the hype?

Yet fundamentals persist: Nvidia's technology underpins the AI revolution, from cloud computing to autonomous systems. If custom chips nibble at market share, Nvidia's innovation pipeline—spanning software and hardware—could counterpunch. Investors must weigh the bubble risks against the transformative potential, a calculus that has minted fortunes and felled others.

In this selloff reckoning, Nvidia's story is far from over. It's a tale of empire under siege, where visionaries like Huang clash with skeptics like Burry, and the outcome hinges on AI's real-world traction. For now, the throne wobbles, but history favors the bold—provided the foundations hold.

Expert analysis on U.S. markets and macro trends, delivering clear perspectives behind major market moves.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet