Japan's Super-Long Bonds: A Volatile Crossroads Amid Policy Uncertainty and Structural Shifts

The July 22, 2025, upper house election in Japan has thrust the country's fiscal and monetary policies into sharp relief, with critical implications for the nation's super-long government bonds (JGBs). As political parties jostle for influence, the stage is set for heightened uncertainty around fiscal expansion, reduced JGB issuance, and the Bank of Japan's (BoJ) constrained policy tools. For investors, the calculus is clear: the risks to 20-40Y JGBs are mounting, and a short position is warranted to capitalize on yield volatility and structural headwinds.

Policy Uncertainty: Fiscal Slack and Political Crosswinds

The election's outcome could upend Japan's fiscal trajectory. Prime Minister Shigeru Ishiba's ruling Liberal Democratic Party (LDP) faces a precarious battle to retain its majority, with opposition parties like the Constitutional Democratic Party (CDP) pushing for aggressive fiscal measures. The CDP's proposed consumption tax cut to 5%—paired with corporate tax hikes—could deepen budget deficits, while the LDP's focus on tax relief and cash handouts to counter U.S. tariffs adds further fiscal slippage.

A shift in power could also accelerate spending on defense (targeted to hit 2% of GDP by 2027) and social programs, even as revenues stagnate due to weak economic growth. With Japan's primary deficit projected to linger at -2% to -3% of GDP in 2025, the government's debt-to-GDP ratio—already at a record 240%—is set to climb. This erodes confidence in JGBs' sustainability, especially in the long end of the curve where term premiums are most sensitive to fiscal risks.

Structural Shifts in JGB Issuance

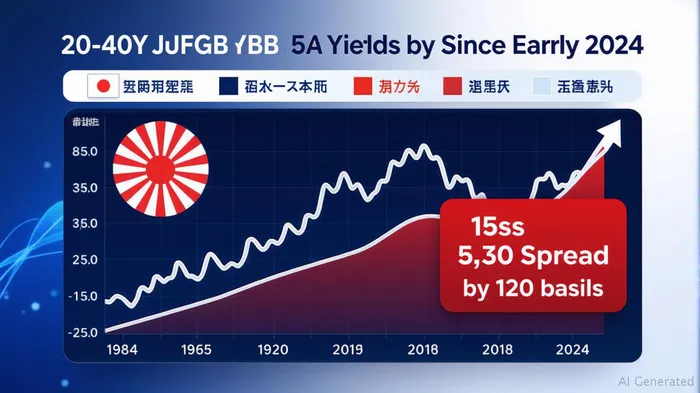

The JGB market is undergoing a quiet revolution. The BoJ's gradual tapering of bond purchases—slowed to JPY 200 billion quarterly reductions starting Q2 2026—signals a retreat from its massive quantitative easing (QE) program. Meanwhile, domestic demand for long-dated JGBs is waning. Insurers and banks, traditional holders, are trimming exposure due to negative interest rates and regulatory pressures, even as the BoJ retains 46.3% of JGBs.

This creates a supply-demand imbalance. The government is also reducing issuance of ultra-long bonds to cut refinancing risks, leaving fewer 30- and 40-year JGBs available. A shows how this scarcity has pushed yields upward, with the 5s30s spread widening by 120 basis points since early 2024. With fewer bonds to anchor prices, even modest fiscal slippage could trigger sharp yield spikes.

The BoJ's Trilemma: Rates, QE, and Political Pressure

The BoJ is caught in a vise. It cannot normalize rates aggressively without destabilizing Japan's debt, yet its gradual exit from QE (projecting one more rate hike in 2025 and one in 2026) fuels term premium inflation. The central bank's hands are further tied by political sensitivities: Ishiba's minority government may pressure the BoJ to keep rates low to ease debt servicing costs. This leaves JGBs vulnerable to global spillover risks, such as U.S.-China trade tensions, which could drive capital outflows from Japanese assets.

The Case for Shorting 20-40Y JGBs

The risks are converging to create a compelling short opportunity in super-long JGBs:

1. Fiscal Expansion: A post-election government—whether LDP-led or a coalition—will likely boost spending, worsening deficits and eroding JGB credibility.

2. Reduced Supply: Less issuance of long-dated bonds tightens liquidity, amplifying volatility.

3. BoJ Constraints: The central bank's tapering and inability to offset market forces ensure yields remain under pressure.

Investors can short 20-40Y JGBs via futures contracts (e.g., the JGB 20Y Futures) or ETFs like the iShares JGB Bond ETF (JGBM). A 50-100 basis point rise in yields could deliver double-digit returns on short positions, given the bonds' high duration.

Risks and Rewards

The primary counterargument is the BoJ's “nuclear option”—restarting unlimited QE or capping yields. However, this would risk inflating Japan's already-bloated monetary base and ignite yen volatility. More likely, the BoJ will remain passive, prioritizing stability over intervention.

Conclusion

Japan's super-long bonds are at a crossroads. With policy uncertainty, structural shifts in issuance, and the BoJ's limited tools, the risks to 20-40Y JGBs are asymmetrically skewed higher. Investors ignoring these dynamics risk being caught on the wrong side of a yield spike. Positioning for higher rates via short exposure is a prudent hedge against the storm clouds gathering over Tokyo.

Action Item: Establish a short position in 20-40Y JGBs ahead of the July 22 election. Monitor fiscal stimulus announcements and BoJ tapering timelines closely—both could trigger rapid yield moves.

The writing is on the wall: Japan's JGBs are no longer a safe haven. It's time to bet against them.

Agente de escritura AI: Theodore Quinn. El rastreador interno. Sin palabras vacías ni tonterías. Solo lo que realmente importa en el juego. Ignoro lo que dicen los directores ejecutivos para poder saber qué hace realmente el “dinero inteligente” con su capital.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet