Jan. CPI Watch: Will Price Hikes Drive an Upside Surprise?

The U.S. January CPI report is about to be released. January nonfarm payrolls significantly exceeded expectations. If inflation also surprises to the upside, the Federal Reserve will almost certainly refrain from cutting rates in the first half of the year—and may even hold rates steady throughout the entire year.

Several investment banks expect that due to the “January effect” of annual price resets and the pass-through of tariff costs, core inflation may rebound on a month-over-month basis. However, a potential moderation in services inflation could be viewed as a positive signal by the Fed.

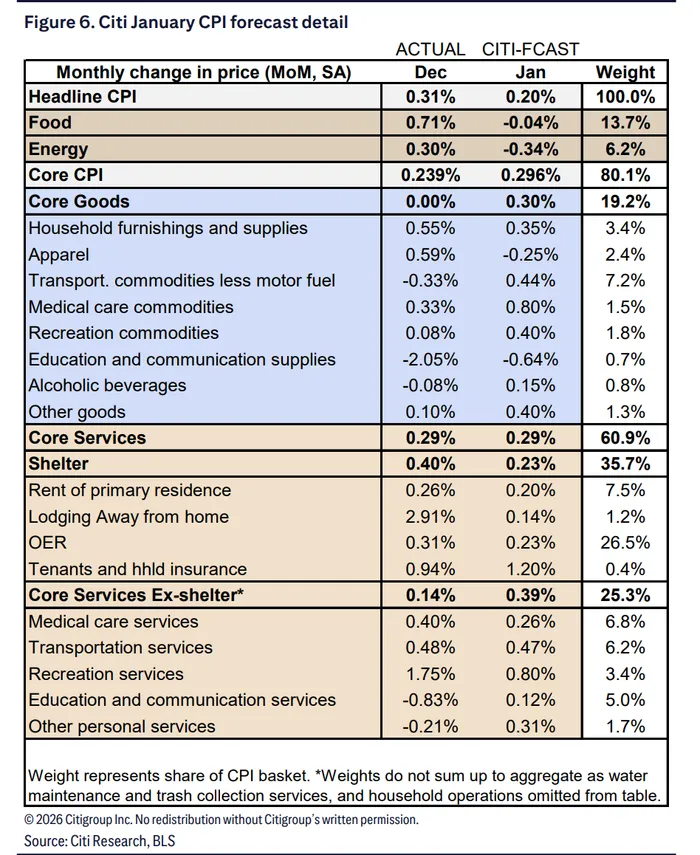

The market broadly expects January core CPI to rise around 0.3% month-over-month. UBSUBS-- is more aggressive, forecasting a potential increase of as much as 0.38%.

Goods Inflation: January Price Resets Take Center Stage

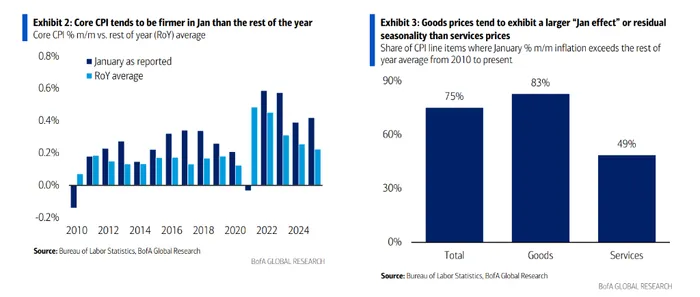

At the start of the year, businesses typically adjust prices in bulk. Bank of AmericaBAC-- notes that January is often a hotter month for inflation data, projecting core goods prices to rise 0.40% month-over-month (0.35% excluding used cars), a clear acceleration from December. This reflects increased tariff pass-through and typical early-year pricing adjustments.

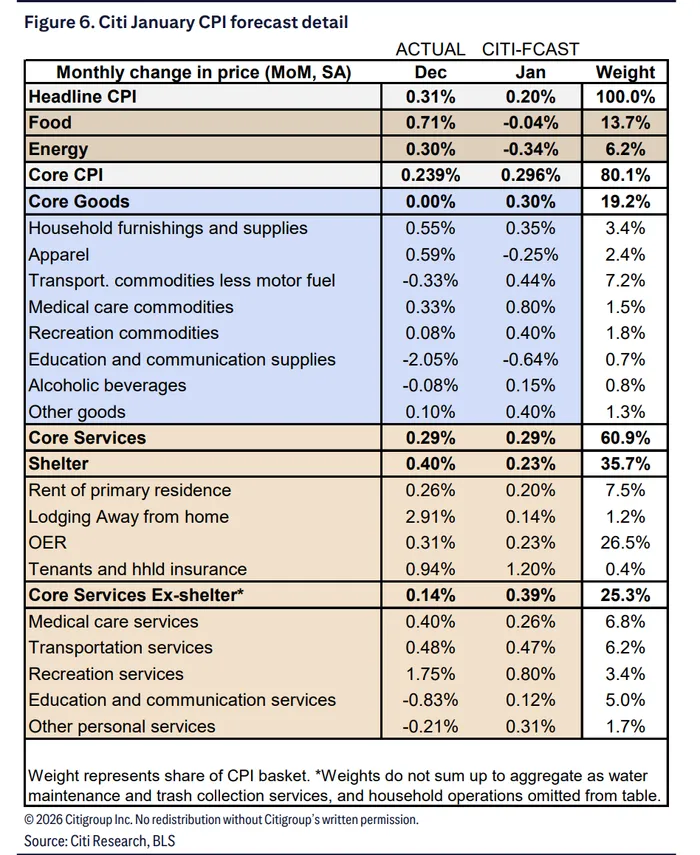

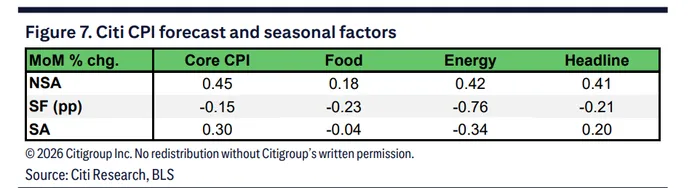

Citi holds a similar view, forecasting core goods prices to rise 0.31%, the strongest increase since 2023. CitiC-- analysts highlight furniture (+0.35%), auto parts (+0.75%), and medical goods (+0.8%) as categories where sellers are using the January pricing window to pass through tariff costs.

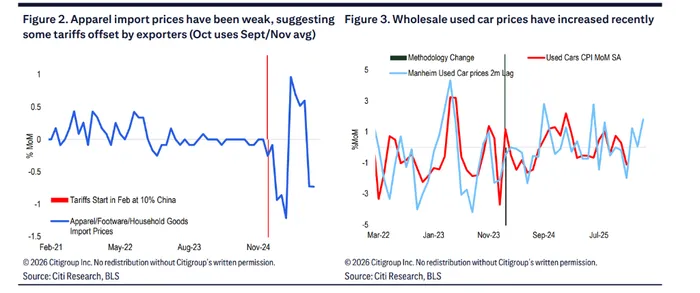

However, Citi expects apparel prices to decline 0.25% month-over-month in January, partly due to lower import prices, suggesting that foreign producers may be absorbing some tariff costs.

UBS issues the strongest warning on upside inflation risks. Citing the Adobe Digital Price Index (DPI) and data from Harvard’s Pricing Lab, UBS notes a sharp rise in online goods prices in January. It also points to measurement distortions: delayed CPI data collection in November created sampling issues that are expected to reverse in January, potentially adding about 5 basis points to core goods and airline fares.

UBS models suggest core CPI could land within a wide range of 0.28% to 0.56% month-over-month.

Services Inflation: Signs of Moderation?

Turning to services inflation, Citi forecasts core services (excluding housing) to rise 0.39% month-over-month. While still elevated, this is significantly below the roughly 0.7% average seen in January over the past two years. Citi argues that if residual seasonal price increases in services prove weaker than usual, it would signal easing underlying inflation pressures.

On housing inflation, views are relatively aligned. Citi expects shelter prices to rise 0.23%, maintaining that the broader downtrend remains intact. UBS projects owners’ equivalent rent (OER) to increase 0.26%, roughly in line with pre-pandemic averages, suggesting long-term rental trends are cooling.

UBS again plays the inflation watchdog, noting that certain volatile components distorted by data collection issues in December—such as a sharp drop in moving and storage services and a spike in video rental services—may reverse in January, pushing headline readings higher.

Inflation May Peak Soon, According to Some Banks

Bank of America characterizes the current inflation environment as “not too hot, not too cold.” Although inflation has remained above the Fed’s 2% target over the past five years, unless demand-driven inflation re-accelerates significantly or inflation expectations become unanchored, the Fed’s near-term stance will likely remain guided primarily by labor market data.

BofA forecasts January core PCE at 0.29% month-over-month, with year-over-year growth around 3.0%.

Citi is more optimistic, arguing that January and February data are critical in reshaping market perceptions of inflation persistence. If inflation prints continue to undershoot expectations during the typically seasonally strong early-year period, it could convince hawkish officials that sticky inflation is no longer the dominant concern.

Citi maintains its expectation of at least 75 basis points of rate cuts this year.

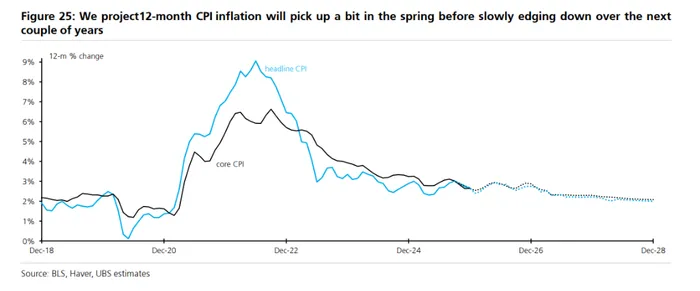

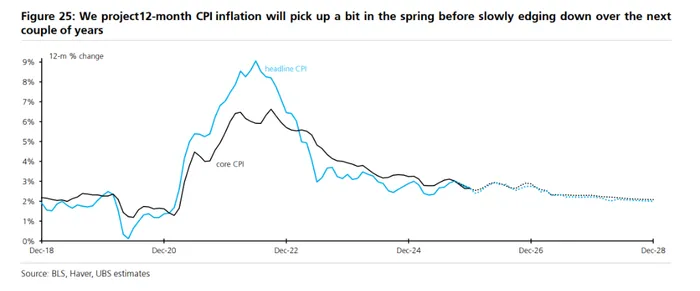

Although UBS anticipates firmer short-term data, it expects inflation to peak in the spring and then gradually decline over the coming years. UBS projects headline CPI year-over-year to fall to 2.41% in January, while core CPI may ease slightly to 2.57%, the lowest level since March 2021.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet