U.S. ISM Manufacturing New Orders Dives to 46.4: A Sector Divide Emerges

The June U.S. ISM Manufacturing New Orders Index plummeted to 46.4, its lowest level since 2020, signaling a deepening contraction in industrial demand. This decline has created a stark divide between sectors: Construction/Engineering stocks face headwinds, while Consumer Finance firms may see tailwinds as economic uncertainty drives credit demand. Here's how investors should position for this divergence.

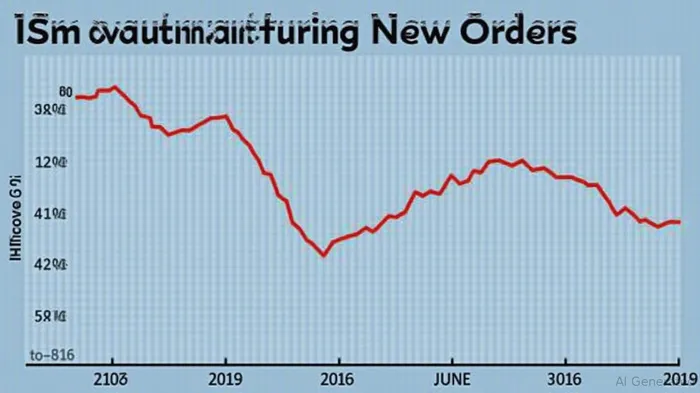

The Numbers Tell a Story of Weakening Demand

The ISM New Orders Index, a bellwether for manufacturing health, has now contracted for eight consecutive months. June's reading of 46.4 marks a sharp drop from May's 49.3 and falls below the 50 threshold separating expansion from contraction. The decline reflects reduced capital spending, trade policy uncertainty, and slowing global demand—factors that disproportionately impact cyclical industries.

Why This Matters for Investors

The ISM data isn't just about factories—it's a harbinger of sector-specific risks and opportunities. Let's break down the implications:

1. Construction/Engineering: Caught in the Crossfire

The Construction/Engineering sector is acutely sensitive to the ISM New Orders Index because it relies on industrial demand for materials, equipment, and infrastructure projects. With the index in freefall, key pain points emerge:

- Material Costs and Supply Chain Strains: Tariffs on steel, aluminum, and critical minerals continue to inflate costs. For example, CaterpillarCAT-- (CAT) recently noted 8% higher steel prices in its Q2 earnings call.

- Project Delays: Geopolitical tensions and trade disputes have slowed global supply chains, delaying construction timelines.

- Lower Capital Spending: Firms are delaying investments in new facilities or upgrades amid uncertainty.

Investment Takeaway: Reduce exposure to Construction/Engineering equities. Overweight defensive plays or consider short positions in industrials until the ISM index stabilizes above 50.

2. Consumer Finance: A Safe Haven in Uncertain Times

While manufacturing sputters, Consumer Finance firms—such as credit card issuers and fintechs—are benefiting from two trends:

- Increased Credit Demand: Economic anxiety often boosts borrowing for mortgages, auto loans, and personal credit. JPMorgan ChaseJPM-- (JPM) reported a 12% rise in Q2 credit card balances.

- Stable Interest Rate Environment: Even if the Fed pauses hikes, existing rate levels support net interest margins for banks.

Investment Takeaway: Overweight Consumer Finance stocks. Look for firms with robust underwriting standards (e.g., Wells FargoWFC-- (WFC)) and exposure to digital payments (e.g., Square (SQ)).

The Fed's Tightrope Walk

The Federal Reserve will face mounting pressure to pause its rate-hiking cycle if the ISM decline persists. A prolonged contraction could tip the Fed toward prioritizing growth over inflation control, which would:

- Boost bond markets: Lower rate hike expectations could drive Treasury yields lower, benefiting utilities and REITs.

- Weaken the dollar: A dovish Fed might reduce pressure on the greenback, aiding dollar-sensitive sectors like gold miners (e.g., NewmontNEM-- (NEM)).

Final Call: Pivot to Defensive Plays

The ISM New Orders Index has become a critical dividing line for investors. Until the data stabilizes, avoid sectors tied to industrial demand and favor financial services. Monitor these key catalysts in the coming weeks:

- July 5: Durable Goods Orders report for further signs of manufacturing weakness.

- July 18: FOMC minutes to gauge policy sentiment.

The bottom line: This isn't just a manufacturing slowdown—it's a sector realignment. Play defense now, and reposition once the data turns.

Sumérjase en el mundo de las finanzas mundiales con Epic Events Finance.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet