IRWD Stock Down 14% in a Month: Time to Buy, Sell or Hold the Stock?

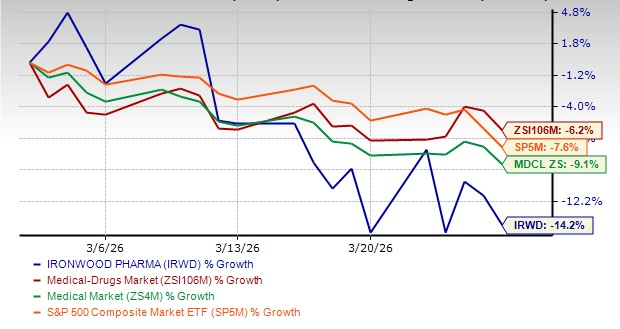

Shares of Ironwood Pharmaceuticals IRWD have witnessed a sharp decline over the past month, primarily due to softer sales of its sole marketed product, Linzess (linaclotide), during the fourth quarter of 2025. The stock has plunged 14.2% over the past month, while the industry has decreased 6.2%. IRWDIRWD-- shares have also underperformed the sector and the S&P 500 in this timeframe, as seen in the chart below.

Image Source: Zacks Investment Research

Linzess is approved for the treatment of irritable bowel syndrome with constipation (IBS-C) in adults and pediatric patients aged seven years and above. The drug is also approved for treating functional constipation in children and adolescents aged six to 17 years.

Despite gaining momentum in recent times, Linzess sales were soft during the fourth quarter of 2025, resulting in a reduced share of net profit for IronwoodIRWD--. Per management, the decline in Linzess sales was largely due to gross-to-net rebate adjustments and higher pricing pressure from the Medicare Part D redesign, and not underlying demand.

Let’s analyze Ironwood’s strengths and weaknesses to understand how to play the stock amid the recent share price drop.

IRWD’s Top Line Aided by Strong Partnerships for Linzess

Ironwood markets Linzess in the United States in collaboration with drug giant AbbVie ABBV. The companies equally share Linzess’ brand collaboration profits and losses in the United States.

Ironwood’s top line primarily comprises revenues recorded under its collaborative arrangements with ABBVABBV-- for the development and commercialization of Linzess in the United States.

Although Ironwood’s share of net profit from the sales of Linzess in the United States declined 15% year over year in 2025, Linzess’ prescription demand remained strong during this period, underscoring management’s optimism for sustained growth in 2026.

Ironwood also has partnerships with Astellas Pharma and AstraZeneca AZN for the development and commercialization of Linzess in Japan and China, respectively. Under these agreements, Ironwood receives royalty payments from these companies based on net Linzess sales in those markets.

The above collaborations act as a source of revenues in the form of royalties for Ironwood.

IRWD’s Strong 2026 Outlook on Linzess Demand

Though Linzess sales were soft during the fourth quarter of 2025, Ironwood expects a strong rebound and improvement in Linzess’ sales in 2026 and subsequently its share of net profit from the sales of the drug in the United States.

Ironwood expects total revenues of $450-$475 million in 2026. The revenue outlook for 2026 indicates an increase of 54% year over year at the midpoint compared with 2025.

The rebound is expected to come mainly from improved net pricing after a list-price cut and continued prescription growth. Ironwood is also focusing on Linzess’ label expansion efforts to support long-term growth.

Notably, effective Jan. 1, 2026, Linzess’ list price was reduced to help maintain patient access. Despite the price cut, management expects Linzess’ net sales to increase year over year in 2026, as the lower list price will reduce certain mandatory government rebates. Fewer rebate payments should translate into higher net revenues in 2026.

IRWD's Key Pipeline Update

Ironwood is making good progress with the development of apraglutide, its next-generation GLP-2 analog.

The company is developing apraglutide for treating patients with short bowel syndrome (“SBS”) with intestinal failure (“IF”) who are dependent on parenteral support (“PS”). Ironwood recently met with the FDA and aligned on key elements of a confirmatory phase III study design, which will evaluate apraglutide in patients with SBS-IF.

Initiation of clinical sites for the study is expected to begin in the second quarter of 2026.

Ironwood acquired the rights to develop and commercialize apraglutide following the acquisition of VectivBio in June 2023.

Though still in the early days, management believes that if successfully developed, apraglutide holds the potential to become a blockbuster drug.

IRWD’s Valuation and Estimate Revision

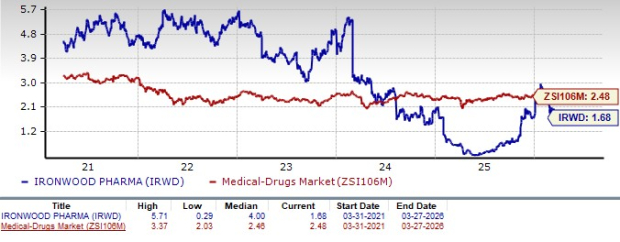

From a valuation standpoint, Ironwood is trading at a discount to the industry. Going by the price-to-sales (P/S) ratio, the stock currently trades at 1.68 times trailing 12-month sales value, lower than 2.48 times for the industry. Also, the stock is trading below its five-year mean of 4.00.

Image Source: Zacks Investment Research

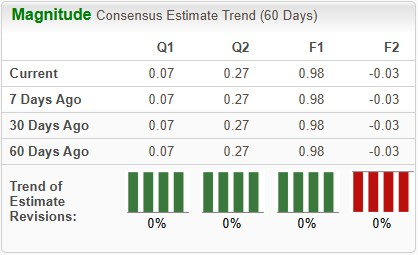

The Zacks Consensus Estimate for 2026 earnings per share (EPS) has remained stable at 98 cents over the past 30 days. During the same time frame, loss per share estimates for 2027 have also remained stable at 3 cents.

Image Source: Zacks Investment Research

Stay Invested in IRWD Stock

We suggest investors retain this Zacks Rank #3 (Hold) stock for now. The fact that it is trading at a discount compared to the industry, buoyed by the upbeat guidance for Linzess in 2026, is likely to keep investors optimistic.

Also, Ironwood’s recent approach of strengthening the Linzess franchise while progressing apraglutide, which holds blockbuster potential, positions it for long-term growth and profitability.

Despite the recent price fall, Ironwood’s ongoing developments with Linzess, pipeline progress and steady earnings estimates also indicate analysts' optimistic outlook for the stock. However, the company’s heavy reliance on a single product for revenues and growth remains a concern.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AstraZeneca PLC (AZN): Free Stock Analysis Report

Ironwood Pharmaceuticals, Inc. (IRWD): Free Stock Analysis Report

AbbVie Inc. (ABBV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet