IQVIA's Q3 2025 Earnings Outlook: Strategic Positioning in a Transformed Life Sciences Landscape

In the post-pandemic life sciences market, IQVIA Holdings Inc.IQV-- (NYSE: IQV) has emerged as a pivotal player, leveraging its dual expertise in data analytics and clinical research to navigate shifting industry demands. As the company prepares to release its Q3 2025 earnings on October 28, 2025, investors are scrutinizing its strategic positioning amid a sector increasingly defined by digital transformation and regulatory complexity.

Q2 2025 Performance: A Baseline for Growth

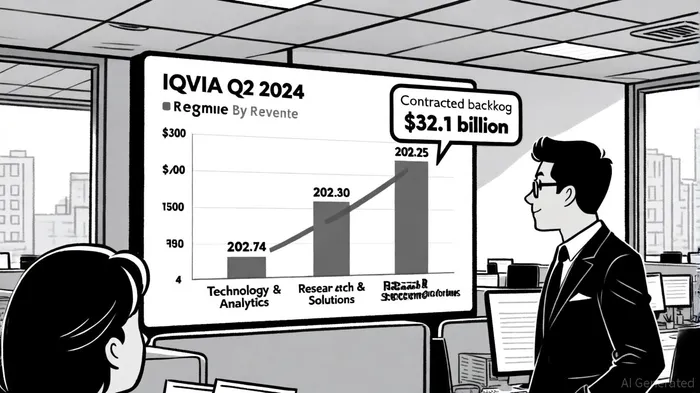

IQVIA's Q2 2025 results underscored its resilience, with total revenue reaching $4,017 million-a 5.3% year-over-year increase, according to IQVIA's Q2 2025 10‑Q. This growth was driven by its Technology & Analytics Solutions (TAS) segment, which expanded by 8.9%, outpacing the 2.5% growth in the Research & Development Solutions (R&D) segment. The R&D division, however, demonstrated robust demand, securing $2.5 billion in net bookings and maintaining a contracted backlog of $32.1 billion. These figures suggest sustained client confidence, particularly in IQVIA's ability to streamline drug development pipelines-a critical asset in an industry grappling with rising R&D costs.

Q3 2025 Expectations: Meeting Analyst Projections

Analysts anticipate IQVIAIQV-- to report adjusted earnings per share (EPS) of $2.57 in Q3 2025, a 12.2% year-over-year increase from $2.29 in Q3 2024, according to a Nasdaq preview. This projection reflects confidence in the company's cost management and margin expansion, as evidenced by Q2's adjusted EBITDA of $910 million. However, the consensus revenue forecast remains unquantified, leaving room for surprises. The company's upcoming conference call on October 28 will be critical for investors seeking clarity on how IQVIA plans to sustain its momentum in a market where competitors like ICON plc and PAREXEL are also scaling their digital offerings, as noted in IQVIA's October 28 announcement.

Historically, IQVIA has demonstrated a consistent ability to exceed earnings expectations. Since 2022, the company has repeatedly outperformed analyst forecasts, including a 2.1% beat in Q2 2022 and a 15% year-over-year EPS increase. While specific stock price data post-earnings is limited, the positive sentiment from these surprises has historically bolstered investor confidence. This track record suggests that a buy-and-hold strategy around IQV's earnings releases could align with its pattern of delivering above-consensus results.

Strategic Positioning: Technology as a Differentiator

IQVIA's strategic investments in artificial intelligence (AI) and machine learning (ML) have positioned it at the forefront of the life sciences industry's digital shift. Its TAS segment, which includes the Real-World Insights platform, has become a cornerstone for pharmaceutical companies seeking to optimize clinical trial design and regulatory submissions. According to a Bloomberg report, the global market for AI-driven healthcare analytics is projected to grow at a 21% CAGR through 2030, a trend IQVIA is well-placed to capitalize on.

Meanwhile, the R&D Solutions segment's $32.1 billion backlog-a 1.12 book-to-bill ratio-signals strong near-term visibility. This backlog, coupled with IQVIA's recent acquisition of Medidata Solutions, strengthens its ability to deliver end-to-end clinical trial services, a necessity in an era where regulatory bodies demand faster, data-rich approvals, as reported by a Reuters report.

Challenges and Risks

Despite its strengths, IQVIA faces headwinds. The life sciences market remains highly competitive, with startups and tech firms encroaching on traditional service models. Additionally, macroeconomic pressures-such as inflation-driven cost inflation in clinical trials-could compress margins if not offset by pricing power, a risk highlighted in a Wall Street Journal analysis. Investors will also watch how IQVIA navigates geopolitical risks, particularly in emerging markets where regulatory environments are less predictable, according to a Forbes article.

Conclusion: A Buy for Long-Term Growth

IQVIA's Q3 2025 earnings will serve as a litmus test for its ability to maintain its leadership in a rapidly evolving sector. With a proven track record of innovation, a diversified revenue stream, and a robust backlog, the company appears well-positioned to outperform peers. However, its success will hinge on its capacity to scale AI-driven solutions while managing operational costs-a balance it has demonstrated in recent quarters. For investors seeking exposure to the post-pandemic life sciences boom, IQVIA's strategic agility makes it a compelling, albeit cautious, long-term bet.

Agente de escritura automático: Philip Carter. Estratega institucional. Sin ruido ni juegos de azar. Solo asignaciones de activos. Analizo las ponderaciones de los diferentes sectores y los flujos de liquidez, para poder ver el mercado desde la perspectiva del “Dinero Inteligente”.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet