Should You Invest in Capital One Stock Despite Its Premium Valuation?

At a glance, Capital One Financial Corporation COF stock appears to trade at a premium when compared with the industry at large. The company’s current forward 12-month price/earnings (P/E) ratio of 9.42 is above the industry average of 8.07. Also, COF’s P/E (F12M) ratio is above its medium over the past five years, which suggests some level of overvalued trading compared with historical norms.

COF is overvalued compared with two of its closest peers, Ally Financial ALLY and OneMain Holdings, Inc. OMF. Ally Financial has a P/E (F12M) ratio of 7.71 and OneMain has a forward 12-month P/E ratio of 7.06.

COF’s P/E (F12M) Ratio

Image Source: Zacks Investment Research

Thus, COF’s not-so-favorable valuation may compel investors to stay away from the stock. This is primarily because, in the case of worsening industry conditions, premium stocks are at risk of valuation reversion to the mean, which results in a sharp decrease in the stock price.

However, investors should not avoid Capital OneCOF-- completely just because of its premium valuation. Before making any investment decision, it is advisable to look at the company’s fundamentals and growth prospects to see if the higher valuation is justified or not.

Factors Aiding Capital One’s Growth

Robust Credit Card Business: The credit card business is COF’s core earnings engine, underpinned by its scale, data-driven underwriting and strong brand presence in the U.S. consumer finance market. Credit cards have been central to COF’s business model and remain its largest revenue source.

While in May 2024, the company ended its card partnership with Walmart, its 2017 acquisition of Cabela's Incorporated’s credit card operations bodes well. Post the Discover Financial acquisition (closed May 2025), Capital One became one of the largest U.S. credit card issuers by balances, significantly boosting scale and revenues.

In 2025, the credit card segment’s net revenues witnessed a year-over-year rise of 40.5%. Loans held for investment within the segment surged 72% year over year, while purchase volumes improved 27%. Despite an intensely competitive environment, strong growth opportunities in card loans and purchase volumes are expected to continue, supporting the segment’s performance.

Inorganic Expansion Efforts: Capital One has been pursuing opportunistic acquisitions over the years, which have been driving its revenues. In January 2026, COFCOF-- announced a $5.15-billion deal to acquire fintech firm Brex, expanding into corporate cards and business payments beyond traditional consumer credit. In May 2025, it acquired Discover Financial in an all-stock transaction valued at $35.3 billion, reshaping the landscape of the credit card industry, creating a behemoth and unlocking substantial value for shareholders (the deal is expected to be more than 15% accretive to adjusted EPS by 2027).

In 2023, COF acquired Velocity Black, bolstering the delivery of exceptional consumer experiences attributable to its innovative technology. Other notable acquisitions include ING Direct USA, HSBC's U.S. Credit Card Portfolio and TripleTree. These have been instrumental in transforming the company from a monoline credit card issuer into a diversified financial services firm with a significant presence in retail banking, commercial lending and digital banking platforms.

Revenue Strength: Capital One’s NII has witnessed a compound annual growth rate (CAGR) of 13.4% over the five years ended 2025. Also, its net interest margin (NIM) expanded to 7.84% in 2025 from 6.88% in 2024 and 6.63% in 2023.

Though the company’s total revenues declined marginally in 2020, the metric witnessed a five-year (2020-2025) CAGR of 13.4%.

COF’s Revenue Trend

Image Source: Zacks Investment Research

Despite the three interest-rate cuts in 2025, Capital One’s NII and NIM are expected to keep benefiting from robust demand for card loans and Capital One’s efforts to scale businesses.

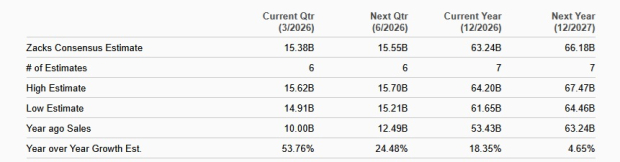

The Zacks Consensus Estimate for COF’s 2026 and 2027 revenues is pegged at $63.24 billion and $66.18 billion, respectively, which indicates year-over-year growth rates of 18.4% and 4.7%.

COF’s Sales Estimates

Image Source: Zacks Investment Research

Solid Balance Sheet: As of Dec. 31, 2025, Capital One had total debt (securitized debt obligations plus other debt) of $51 billion. The total cash and cash equivalents balance was $57.4 billion. Additionally, the company holds investment-grade long-term senior debt ratings of Baa1, BBB and A- from Moody’s Investor Service, Standard and Poor’s, and Fitch Ratings, respectively. This renders the company favorable access to the debt market.

Capital One’s focus on maintaining a strong capital and balance sheet position supports its capital distribution activities. After slashing the quarterly dividend 75% in 2020 based on the Federal Reserve’s requirements, COF restored it to 40 cents per share in the first quarter of 2021. In July 2021, the company hiked its dividend 50% to 60 cents per share and also announced a special dividend of 60 cents per share.

In November 2025, the company raised its quarterly dividend 33.3% to 80 cents per share. Also, Capital One has a share repurchase plan in place. In October 2025, its board of directors authorized the repurchase of up to $16 billion of shares. As of Dec. 31, 2025, $14.1 billion worth of authorization was available for repurchase. Given its earnings strength and solid liquidity position, the company’s enhanced capital distribution plans look sustainable.

Analyzing Capital One’s Price Performance

In the past year, COF shares have lost 0.1%, underperforming the industry and the S&P 500 Index’s 19.9% and 17.6% rallies, respectively. Also, the company’s performance compares unfavorably with that of Ally Financial and OMF.

Ally Financial shares have gained 9.8% and the OneMain stock has rallied 4.1% in the past year.

1-Year Price Performance

Image Source: Zacks Investment Research

How to Approach Capital One Stock Now

As one of the largest credit card issuers in the country, COF benefits from a diversified customer base that spans prime to subprime segments, allowing it to generate attractive yields while actively managing risk. Its long-standing investment in analytics and digital capabilities enables more precise credit decisioning, dynamic pricing and early identification of stress in borrower behavior, supporting resilient revenue generation across credit cycles.

However, if the 10% cap on credit card interest is implemented and enforced, Capital One’s interest income could drop significantly, since cards issued today often yield much more than 10%. The company’s profit margins may shrink, pressuring earnings.

Steadily rising expenses and weak credit quality remain other major woes for the company. Over the last five years (2020-2025), non-interest expenses witnessed a CAGR of 15.2% due to higher marketing costs and inflationary pressures.

If we look at COF’s earnings estimate revisions, it is clear that analysts are not bullish on the stock. Over the past month, the Zacks Consensus Estimate for the company’s 2026 and 2027 earnings of $20.20 and $24.72, respectively, has been revised lower.

COF’s Estimate Revision Trend

Image Source: Zacks Investment Research

While COF’s credit card franchise is expected to remain a central driver of earnings growth and shareholder value creation, investors should not rush to buy the stock now and should wait for an attractive entry point, given its premium valuation. Yet, those who already own the stock should hold on to it as the company is less likely to disappoint in the long run.

Currently, COF carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Capital One Financial Corporation (COF): Free Stock Analysis Report

Ally Financial Inc. (ALLY): Free Stock Analysis Report

OneMain Holdings, Inc. (OMF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet