Intuitive Surgical Under Pressure in China: Can It Defend Its Position?

Intuitive Surgical ISRG is facing intensifying competitive and policy-driven pressures in China, raising questions around the durability of its positioning in one of its key international growth markets. Management highlighted that provincial tenders increasingly favor local robotic suppliers, reflecting both policy support for domestic manufacturers and a growing number of homegrown competitors with architectures similar to earlier da Vinci systems.

This shift is already affecting performance. In the fourth quarter, Intuitive Surgical’s tender win ratio in China declined amid intensifying price competition and growing traction of local players in regional procurement. Although full-year win rates were slightly higher year over year, the quarterly trend points to increasing near-term volatility and margin pressure.

Pricing dynamics are a key concern. As tenders become more competitive, pricing has “become even more intense,” forcing ISRGISRG-- to balance share preservation with profitability. This environment could compress system ASPs and limit margin expansion, particularly as local players compete aggressively on cost.

Intuitive Surgical’s strategy suggests a measured defense rather than retreat. The company is manufacturing systems locally in China, strengthening its operational footprint and enabling greater pricing flexibility. Its broader ecosystem — including training, digital tools and clinical evidence — remains a key differentiator versus emerging competitors.

ISRG continues to emphasize its ability to compete “at a price point that is healthy,” suggesting confidence in maintaining economic discipline despite competitive pressures.

Overall, while China presents increasing policy and pricing risks, the company’s combination of local manufacturing, ecosystem depth, and clinical validation provides a degree of defensibility.

That said, sustained pressure on tender outcomes indicates that China may evolve into a lower-margin, more competitive market, requiring continued strategic adaptation.

Peer Updates

The players across the medical device sector are feeling the competitive pressure in China. Several big medical device makers have manufacturing base in the country, along with a growing customer base which raises concern about growth prospects of these companies in the region. While ISRG faces significant pressure in China, Globus Medical GMED and Stereotaxis STXS appear to face comparatively lower risk from Chinese competition.

Globus Medical appears relatively insulated from China-specific pricing pressure, though competitive intensity in global markets remains a structural consideration. The company’s differentiation lies in its integrated ecosystem of robotics, navigation and implants through ExcelsiusGPS, which management emphasized as a “one-of-a-kind” unified platform driving workflow efficiency and surgeon adoption.

While there is no particular focus on China, Globus Medical’s strategy of flexible pricing models, including leasing and bundled implant pull-through, suggests readiness to compete in price-sensitive environments. GMED’s vertical integration and innovation-led moat enhance defensibility, but sustained pricing pressure in international markets could test margin durability over time.

Stereotaxis faces lower competition in China due to its smaller scale. However, the company’s prospect may get hurt due to rising global pricing pressure, including China, and ongoing commercialization phase. STXS is attempting to offset pricing risks through a structural shift toward higher-margin disposable revenues, with per-procedure revenue rising from nearly $1,000 to over $5,000 via proprietary catheter integration.

Stereotaxis is building a differentiated ecosystem around GenesisX and digital solutions to enhance value beyond hardware. Manufacturing bottlenecks and limited scale constrain its pricing power. While its technology remains differentiated, Stereotaxis’ competitive position appears more execution-dependent, with defensibility hinging on successful scaling of its ecosystem and recurring revenue model.

ISRG’s Price Performance, Valuation and Estimates

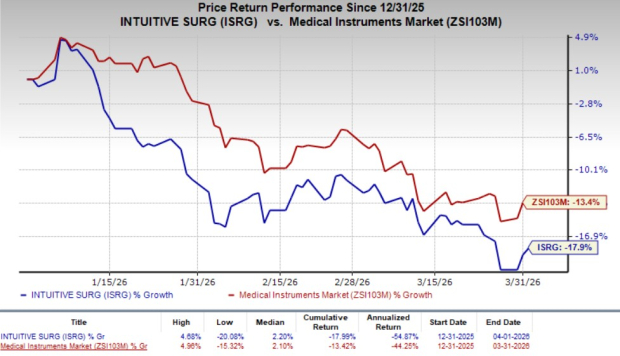

Shares of ISRG have lost 17.9% so far this year compared with a 13.4% decline of the industry.

Image Source: Zacks Investment Research

From a valuation standpoint, Intuitive SurgicalISRG-- trades at a forward price-to-earnings ratio of 44.4, above the industry average. But, it is still lower than its five-year median of 70.78. ISRG carries a Value Score of D.

Image Source: Zacks Investment Research

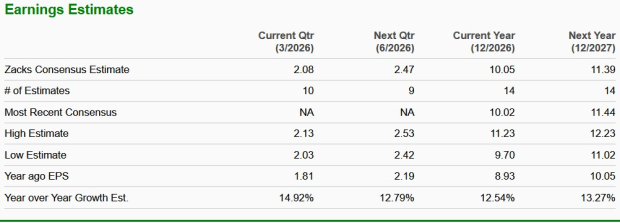

The Zacks Consensus Estimate for Intuitive Surgical’s 2026 earnings implies a 12.5% rise from the year-ago period’s level.

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Stereotaxis Inc. (STXS): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet