Intel's Strategic Turnaround: Why Skepticism Still Outweighs Optimism for Near-Term Investors

The semiconductor sector is riding a wave of optimism in 2025, fueled by AI-driven demand for high-bandwidth memory (HBM), data center expansion, and advanced manufacturing capabilities. Global revenue is projected to hit $697 billion this year, with AI-related applications alone driving a 70% surge in HBM sales, according to a Q3 2025 industry report. Yet, for IntelINTC-- (INTC), the narrative remains mired in skepticism. Despite aggressive strategic pivots-ranging from foundry ambitions to AI accelerator development-the company's valuation metrics and operational performance continue to raise red flags for near-term investors.

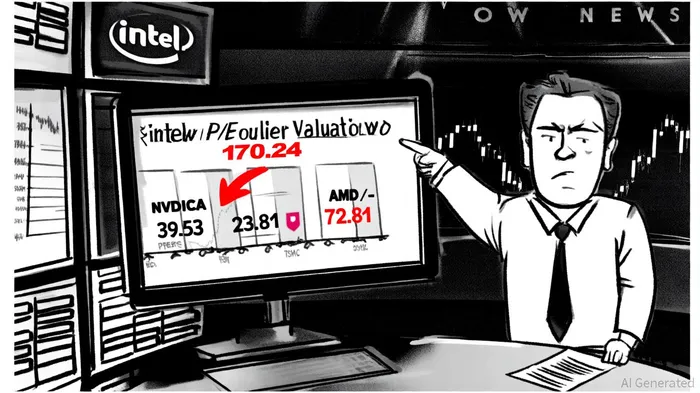

Valuation Realism: A Tale of Disconnection

Intel's forward P/E ratio of 170.24 and EV/EBITDA of 22.09 are staggering, especially when juxtaposed against its peers. NVIDIA trades at a forward P/E of 39.53, while TSMC, the foundry giant, commands a more modest 23.81, per FinanceCharts' PE averages. Intel's EV/EBITDA of 22.09 far exceeds its 3-year (15.29) and 5-year (13.32) averages, signaling a disconnect, per a FinanceCharts EV/EBITDA chart. The company's trailing twelve months (TTM) EBITDA of $9.2 billion, coupled with a -38.64% profit margin, underscores its inability to translate revenue into profitability, according to StockAnalysis statistics.

This valuation disconnect is further amplified by the sector's broader momentum. The average forward P/E for the semiconductor industry is 64.16, reflecting investor confidence in AI-driven growth, per CSIMarket industry P/E data. However, Intel's metrics suggest it is being valued more for potential than performance. With a foundry business still hemorrhaging cash-reporting a $2.9 billion GAAP net loss in Q2 2025-and a client computing segment shrinking year-over-year, the company's ability to justify such lofty multiples remains unproven, according to a Ricentral MarketMinute.

Sector Momentum vs. Execution Gaps

The semiconductor sector's growth is undeniably structural. AI demand has spurred a 30% revenue growth forecast for 2025, with NVIDIA's data center revenue hitting $41.1 billion in Q2 alone, according to that report. TSMC's 30% revenue growth projection and SK Hynix's 40% HBM market share highlight the sector's resilience, per the same report. Yet, Intel's strategic initiatives-while ambitious-lag in execution.

The company's foundry business, a cornerstone of its turnaround plan, is still unprofitable. Despite securing a $5 billion partnership with NVIDIA and an $8.9 billion government-backed equity stake, Intel's foundry division operates at a loss, with operating losses exceeding $3 billion in Q2 2025, as noted in MarketMinute coverage. Analysts like Citi question its ability to compete with TSMC, noting its "money-losing" status and reliance on anchor customers for its 14A process node, according to the Ricentral MarketMinute. Meanwhile, its AI ambitions-centered on Gaudi accelerators and enhanced Xeon processors-face an uphill battle against NVIDIA's dominance in the AI infrastructure space, according to a GPU Wars roundup.

Analyst Sentiment: A Cautionary Outlook

Recent analyst ratings reinforce the skepticism. Of 13 analysts covering Intel in Q3 2025, 10 issued neutral or bearish ratings, with the average 12-month price target at $22.31-a 5.55% drop from prior estimates, according to a Sahm Capital roundup. This cautious stance reflects concerns over Intel's profitability, debt load, and the time required to scale its foundry business. While the company's $20 billion 2025 capital expenditure plan and new manufacturing facilities in Ohio and Arizona signal long-term potential, the near-term investors are left grappling with the reality of declining margins and unmet operational targets, per an Investing.com transcript.

Conclusion: A Long-Term Bet, Not a Quick Win

Intel's strategic initiatives-foundry expansion, AI integration, and domestic manufacturing-position it for long-term relevance in a reshaped semiconductor landscape. However, the near-term outlook remains clouded by valuation overreach, operational losses, and a sector that is outpacing its execution. For investors, the key takeaway is clear: while the sector's momentum is undeniable, Intel's journey from a struggling chipmaker to a profitable growth story will require patience, capital, and a tolerance for risk that many may find unpalatable. Until the company can bridge the gap between ambition and performance, skepticism will likely outweigh optimism.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet