Intel Credit Rating Cut to BBB, Outlook Turns Negative Amid Weak Demand and Mounting Competition

Intel, once the titan of the semiconductor world, is now navigating stormy waters. On Monday, Fitch Ratings cut the company’s credit rating from BBB+ to BBB, with a negative outlook, placing the chipmaker just two notches above junk status.

It’s the latest blow in what has become a relentless series of challenges for IntelINTC-- — a company that not so long ago dominated the global processor market but now faces an existential reckoning.

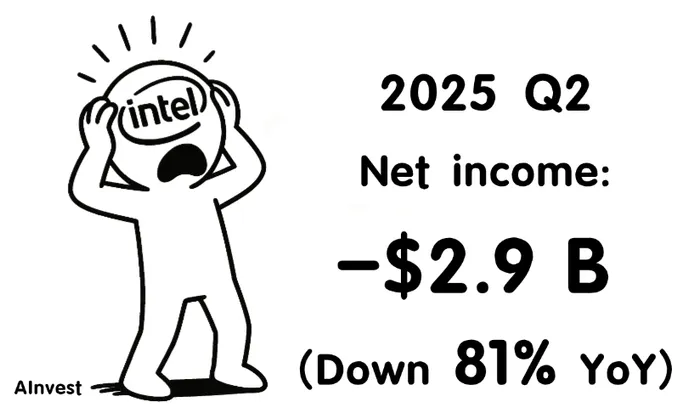

$29 Billion in Losses: A Wake-Up Call

Just two weeks ago, Intel reported a staggering $2.9 billion net loss for Q2 of its 2025 fiscal year — an 81% increase from the $1.6 billion loss in the same quarter last year. The scale of the red ink stunned investors and analysts alike, especially as the loss came despite a modest rebound in quarterly revenue.

The market’s verdict was swift and punishing. In the past month alone, Intel’s stock has shed 11.36%, dragging its market cap down to $85.3 billion — barely a fraction of AMD’s towering $286.6 billion valuation.

Cost-Cutting, Restructuring, and Retreats

Intel hasn’t stood still in the face of these pressures. In a bid to reverse its sliding fortunes, the company has launched a sweeping set of restructuring measures. These include:

- Cutting 15% of its workforce

- Scrapping multiple fabrication plant projects in Europe

- Delaying progress on its high-profile wafer plant in Ohio

- But despite these “bold medicine” efforts, Fitch remained unconvinced.

Fitch’s Warning: “Execution Risk Is High”

In its downgrade report, Fitch cited “intensifying challenges in maintaining product demand” amid fierce competition from the likes of AMDAMD--, BroadcomAVGO--, NXP SemiconductorsNXPI--, and QualcommQCOM--. Sluggish demand in consumer electronics and enterprise hardware has only deepened the operational strain.

“The credit metrics remain weak,” Fitch analysts wrote. “A rating recovery will require stronger end-market demand, successful product refreshes, and meaningful net debt reduction over the next 12–14 months.”

Fitch also pointed to elevated execution risk, suggesting that Intel’s financial structure — already weaker than many of its peers — could come under further stress if its turnaround falters.

Still a Giant, but One Under Siege

Intel continues to dominate legacy markets like PC chips and traditional enterprise servers, but even here, the ground is shifting. AMD has carved out a massive lead in server chips, while Qualcomm is pushing hard into PC silicon.

Fitch emphasized that Intel’s competitive position, while strong, is “deteriorating relative to peers with more resilient financials and stable market positions.”

To regain its lost ground, the firm concluded, Intel must:

- Boost PC chip shipments

- Aggressively cut debt

- Execute flawlessly in a highly dynamic market

Liquidity Is Not the Issue — For Now

One silver lining: Intel’s liquidity remains “solid,” according to Fitch. As of June 28, the company held $21.2 billion in cash, cash equivalents, and short-term investments, plus access to $7 billion in unused credit.

But liquidity alone won’t restore lost investor confidence.

The Bigger Picture: Wall Street Is Losing Patience

Fitch’s move follows in the footsteps of other major agencies. S&P Global downgraded Intel to BBB in December 2024, and Moody’s did the same for its senior unsecured debt in August 2024.

The message from the rating agencies is clear: Intel is no longer being judged on its past dominance but on its ability to survive a rapidly evolving, brutally competitive future.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet