IBM Tops Estimates and Hikes $14B FCF—So Why Is the Stock Plunging 6% on Red Hat Jitters?

IBM tops on revenue and EPS, lifts guidance—yet the stock slumps as investors parse decelerating software signals, mixed signings, and a mainframe-heavy mix. In Q3 , Big Blue delivered $2.65 in adjusted EPS (vs. $2.45 est.) on $16.33B in revenue (vs. $16.09B est.), with gross margins expanding and free cash flow tracking ahead of plan. The upside was driven by Infrastructure (z17 mainframe cycle) and steady Software, while Consulting grew modestly. The concerns: slowing growth inside Red Hat, questions around 2026 comps once the z17 tailwind fades, and softer consulting signings. Shares are ~6% lower pre-market —consistent with a tech tape that’s been unforgiving to “beats-but-not-perfect”—with $263 flagged as a key support on the pullback.

What beat, what missed vs. expectations

- EPS: $2.65 vs. $2.45 expected—clean upside on better mix and operating leverage.

- Revenue: $16.33B vs. $16.09B expected—broadly ahead, aided by strong Infrastructure and in-line Software.

- Margins: GAAP gross margin 57.3% (+110 bps Y/Y); non-GAAP 58.7% (+120 bps). Operating income of $1.62B was essentially in line.

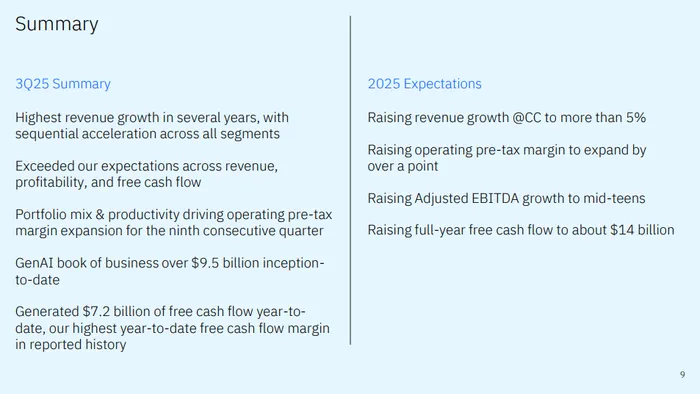

- Guide: IBMIBM-- raised full-year constant-currency revenue growth to “>5%” (from “at least 5%”) and FY free cash flow (FCF) to ~$14B (from $13.5B).

Software: solid headline growth, but cracks under the hood

IBM’s Software revenue rose ~10% to ~$7.2B (about in line with StreetAccount/FactSet views). Within that:

- Automation: +24% Y/Y—standout performance, a clear beneficiary of AI-enabled productivity projects.

- Data & AI (ex-TP): +8% Y/Y—healthy, helped by the expanding watsonx stack and AI services pull-through.

- Transaction Processing: -1% Y/Y—continuing secular drift.

- Red Hat / Hybrid Cloud: headline +14% Y/Y but decelerating from +16% last quarter (UBS notes ~12% CC vs. 14% prior). UBS flags RHEL growth moderating to mid-single digits from abnormal mid-teens, a headwind for Red Hat’s forward cadence.

Takeaway: Software didn’t disappoint at the top line, but the rate of growth decelerated in the all-important Red Hat layer. That’s material because the multi-year IBM story depends on software compounding faster than Infrastructure cycles. The market is discounting that risk today.

Infrastructure: z17 does the heavy lifting (great now, tougher comp later)

Infrastructure revenue jumped ~17% to ~$3.6B, with Hybrid Infrastructure +28%, IBM Z +61%, and Distributed Infrastructure +10%. The new z17 cycle is tracking as IBM’s strongest ever—UBS notes z17 is up ~30% vs. z16—which both powers the Q3 beat and sets up difficult comps in 2026 as the cycle matures. That cyclicality is likely one reason the stock isn’t rewarded for today’s print.

Consulting: better revenue, questions on signings quality

Consulting rose ~3% to ~$5.3B (above ~$5.24B est.), with Intelligent Operations +5% and Strategy & Tech +2%. Management cited growing demand for AI services (digital workers, automation programs). Still, multiple analysts noted weaker signings versus hopes—fueling skepticism about near-term growth acceleration despite a healthy backlog.

Free cash flow: the core of the bull case

IBM’s FCF is the investor focus—and Q3 reinforced momentum.

- Q3 FCF: ~$2.4B, up Y/Y.

- YTD FCF: ~$7.2B, the highest 9-month FCF margin IBM has reported.

- FY25 outlook: ~$14B FCF, raised from $13.5B.

- Management emphasized operating leverage (adj. EBITDA up ~22% Y/Y; +290 bps margin expansion) and portfolio mix as drivers. With a quarterly dividend of $1.68 per share, the FCF outlook underwrites cash returns, selective M&A, and continued AI investments.

AI and the “book of business”

IBM spotlighted an AI “book of business” > $9.5B (up from $7.5B last quarter). That figure aggregates signed work and pipeline across Software and Consulting tied to watsonx, automation, and gen-AI deployments. Management highlighted Automation as a particular outperformer and referenced client wins (e.g., Deutsche Telekom, S&P Global) embedding watsonx into workflows. Partnerships—including with Anthropic and xAI—extend IBM’s model/tooling reach, while Granite 4.0 expands the first-party model family inside watsonx.

Outlook color

Guidance now calls for “more than 5%” constant-currency revenue growth in 2025, mid-teens adj. EBITDA growth, operating pretax margin expansion >1 pt, and ~$14B FCF. Management said Software growth should run approaching double digits for the full year, with Red Hat mid-teens “at the low end,” Automation double-digit, and Transaction Processing low single-digit decline. They also pointed to double-digit revenue growth in Q4 and “accelerated growth heading into 2026”—a claim the market is discounting until Red Hat’s re-acceleration shows up in prints and signings.

Quantum: any news?

Quantum remains a strategic focus, but no material incremental financial update was called out this quarter. IBM continues to invest in quantum hardware/software roadmaps and ecosystem development; however, quantum did not feature as a near-term revenue or margin driver in the Q3 discussion. The commercial story here is still long-dated.

How the tape is reading it

Despite headline beats and higher guidance, IBM is down ~6% premarket. The setup: a big YTD rally (high expectations), a z17-skewed beat that raises 2026 comp anxiety, and Red Hat deceleration right where the growth multiple lives. UBS, for example, reiterated Sell (PT to $210 from $200), arguing key software metrics are “increasingly worrisome” into CY26 even as the mainframe program looks stellar now. Technically, $263 is a near-term level to watch; a hold there would keep the longer uptrend intact.

Bottom line

IBM posted a clean beat and raised both sales and FCF outlooks—exactly what you want to see. Yet the quality of growth matters: Infrastructure strength is welcome but cyclical, while Software must carry the mantle into 2026+; that makes Red Hat’s slowdown the most important data point in the quarter. If IBM can re-accelerate Red Hat, sustain Automation’s double-digit growth, and convert its $9.5B AI book into durable ARR, today’s dip could prove technical. If not, the market’s caution will look prescient.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet