HubSpot Pivoting Toward Margin Expansion: Is the Growth Sustainable?

HubSpot, Inc. HUBS is increasingly pivoting toward margin expansion, marking a transition from a pure growth-oriented SaaS firm to one focused on profitable scaling. At the core of this improving margin trend is management’s focus on balancing growth investments with cost discipline, ensuring that incremental revenue translates to the bottom line.

A major lever behind this margin expansion is HubSpot’s push toward high-value customers. The company has witnessed strong growth in larger deals and enterprise-like customers, with high-value contracts growing rapidly. These customers typically deliver better unit economics through larger deal sizes, lower churn and higher lifetime value, enabling HubSpotHUBS-- to improve both gross and operating margins over time. In addition, increased multi-product adoption deepens customer relationships and drives higher revenue per account without proportionate increases in sales and marketing costs.

Management has guided toward continued operating margin improvement, with expectations of nearly 20% margins in 2026 and longer-term targets approaching the mid-20% range. The combination of upmarket expansion, AI-driven efficiency, improved monetization and disciplined cost control positions the company to deliver durable profitability.

Other Firms Focusing on Margin Improvements

Salesforce, Inc. CRM is focusing on cost rationalization, workforce restructuring and tighter capital allocation, while also emphasizing higher-margin subscription and platform revenues. Its “Customer 360” ecosystem and AI layer allow it to upsell existing enterprise clients, improving revenue per customer without proportionate cost increases. This combination of enterprise pricing power + operating discipline is helping Salesforce expand operating margins, positioning it as a mature SaaS compounder rather than a pure growth story.

Adobe Inc. ADBE is benefiting from a structurally high-margin subscription model and has been pushing margins further via price increases, bundling and AI-driven upselling. Adobe’s strategy centers on premium enterprise positioning, where customers are less price-sensitive and more focused on ROI, enabling consistent gross margin strength. In addition, it has been optimizing its cost base by consolidating platforms and leveraging shared infrastructure across Creative Cloud and Experience Cloud.

HUBS’ Price Performance, Valuation and Estimates

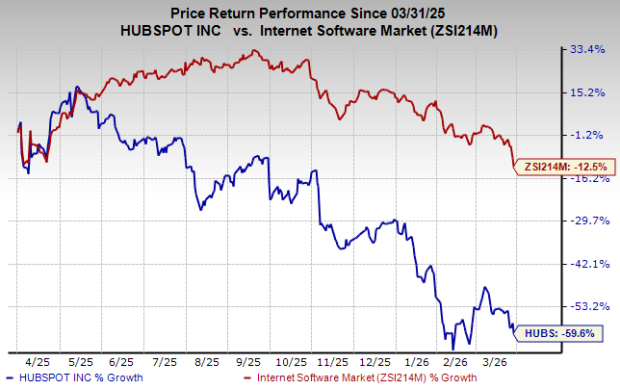

HubSpot stock has plummeted 59.6% over the past year compared with the industry’s decline of 12.5%.

Image Source: Zacks Investment Research

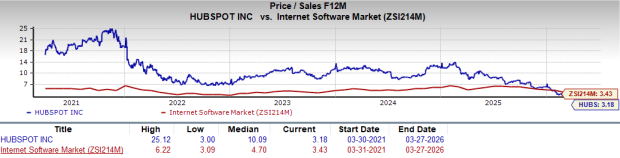

From a valuation standpoint, HUBSHUBS-- trades at a forward price-to-sales ratio of 3.18, below the industry tally of 3.43.

Image Source: Zacks Investment Research

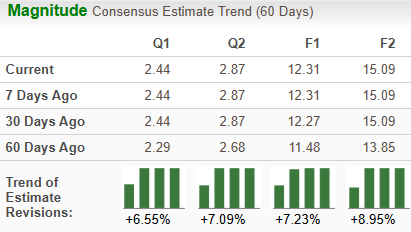

The Zacks Consensus Estimate for HUBS’ earnings for 2026 has been raised 7.2% over the past 60 days.

Image Source: Zacks Investment Research

HubSpot currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Salesforce, Inc. (CRM): Free Stock Analysis Report

Adobe Inc. (ADBE): Free Stock Analysis Report

HubSpot, Inc. (HUBS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet