HP's Undervalued Potential: A Contrarian Case for the Post-Pandemic Tech Landscape

For contrarian value investors, the key to unlocking alpha lies in identifying companies that have been unfairly punished by market sentiment but retain strong fundamentals. HPHPQ-- Inc. (HPQ) fits this mold perfectly. Despite its role as a cornerstone of the global tech infrastructure, HP has been consistently undervalued by investors, even as its historical resilience and improving financial metrics suggest a compelling opportunity in the post-pandemic landscape.

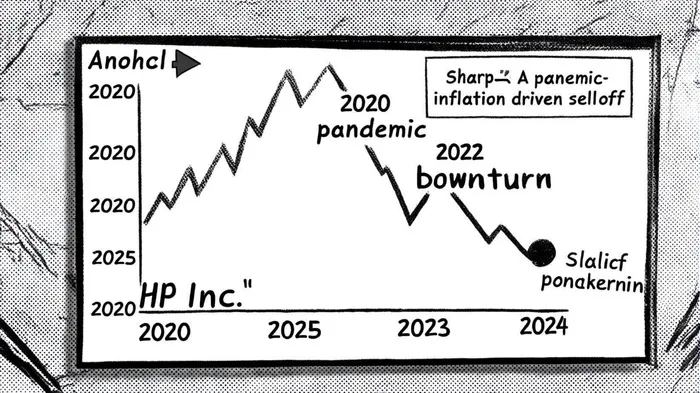

Historical Resilience: A Track Record of Bouncing Back

HP's stock has weathered multiple economic storms with a pattern of sharp declines followed by robust recoveries. During the 2008 financial crisis, HPQHPQ-- fell 27.58% but rebounded 43.14% in 2009, according to StockAnalysis's HPQ statistics. The pandemic-induced sell-off in 2020 saw a 33.28% drop, yet the stock surged 57.29% in 2021, per StockAnalysis. Even the 2022 downturn, which erased 26.4% of its value, was followed by a 12.1% recovery by 2024 in the same dataset. This cyclical pattern underscores HP's ability to adapt to macroeconomic headwinds, a trait critical for long-term value creation.

Discounted Valuation: Metrics That Scream "Buy"

HP's valuation metrics are strikingly out of step with its peers. As of September 2025, HP trades at a forward P/E of 8.11 and an EV/EBITDA of 7.19, both far below the Information Technology sector's averages of 40.65 and 27.25, respectively, according to Siblis Research. The price-to-book (P/B) ratio of 0.46 further highlights its undervaluation, as the technology hardware industry trades at a P/B of 38.96 based on NYU Stern P/B data. These metrics suggest HP is priced for mediocrity, despite generating $2.84 billion in free cash flow (FCF) over the past 12 months (StockAnalysis).

The disconnect between HP's valuation and its fundamentals is even more pronounced when considering its FCF trends. While 2023 saw a 19.47% decline in FCF to $2.978 billion (StockAnalysis), the company rebounded with a 6.01% increase in 2024 to $3.157 billion (StockAnalysis). Analysts project a 5-year EPS growth of 6.04% (StockAnalysis), outpacing the sector's modest revenue growth forecast of 1.50% (StockAnalysis). This suggests HP is not only stabilizing its cash flow but also positioning itself for gradual improvement.

Long-Term Cash Flow Potential: A Contrarian Edge

HP's ability to generate consistent FCF, even during downturns, is a testament to its operational discipline. The company's recent focus on cost optimization and margin expansion-such as reducing capital expenditures and improving working capital efficiency-has bolstered its cash flow resilience, as explained in Investopedia's free cash flow guide. For value investors, this is a critical differentiator. While tech giants with high P/E multiples rely on speculative growth, HP offers a more grounded path to value creation through disciplined capital allocation.

Moreover, HP's low valuation multiples provide a margin of safety. At current levels, the stock trades at a 70% discount to its 5-year average P/E of 14.5 (StockAnalysis). With a consensus price target of $30.29 (12.31% above the current price) (StockAnalysis), the potential for re-rating is substantial, particularly if macroeconomic conditions stabilize and demand for hybrid work infrastructure persists.

Risks and Realities

No contrarian bet is without risks. HP's P/B ratio of 0.46 reflects a historically low book value, which could signal asset write-downs or weak profitability, as discussed in AccountingInsights' P/B guide. Additionally, the company's exposure to the cyclical hardware market means it remains vulnerable to shifts in corporate spending. However, these risks are already priced into the stock, making them less relevant for long-term investors focused on intrinsic value.

Conclusion: A Contrarian Play for the Patient Investor

HP Inc. is a classic value stock: undervalued, resilient, and with a strong cash flow foundation. Its historical ability to recover from downturns, coupled with valuation metrics that diverge sharply from industry averages, makes it an attractive candidate for contrarian investors. While the road to recovery may not be linear, the margin of safety and long-term potential justify a closer look. In a market obsessed with AI-driven growth stories, HP offers a refreshing counterpoint-a reminder that value investing still works, even in the tech sector.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet