Housing Market Volatility and Sector Rotation: Capitalizing on Construction and Consumer Staples Amid MBA Refinance Index Dynamics

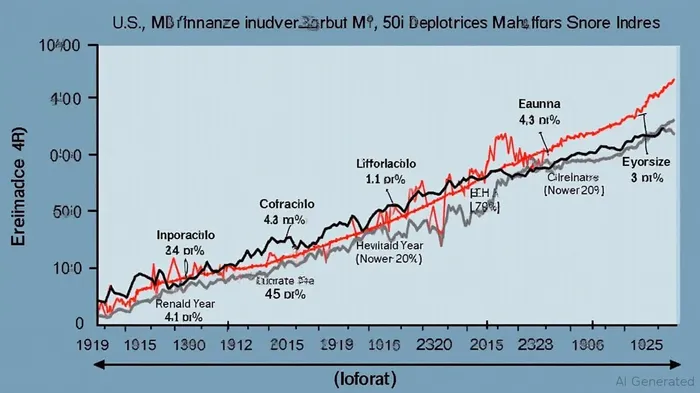

The U.S. MBA Mortgage Refinance Index has emerged as a critical barometer for investors navigating the 2025 housing market's turbulence. In July 2025, the index reached 281.6—the highest level since 2020—before experiencing a 7% weekly decline due to rising mortgage rates. This volatility underscores a shifting economic landscape where sector rotation strategies can capitalize on divergent market forces. For investors, the interplay between refinance activity and sector performance offers clear opportunities in Construction and Consumer Staples while caution is warranted in leisure-dependent assets.

Construction Sector: A Tailwind from Housing Market Dynamics

The surge in refinance activity has indirectly bolstered the construction sector. As homeowners refinance, the Federal Reserve's policy response—historically delayed rate cuts during high refinance periods—has created a favorable environment for construction-linked assets. The Fed's focus on stabilizing housing demand has kept mortgage rates from spiking further, preserving affordability for new home buyers and encouraging builders to ramp up inventory.

For example, the August 2025 housing starts report (to be released in early September) is expected to show a 4–5% quarterly increase, driven by pent-up demand and ongoing housing shortages. This trend supports construction firms like LennarLEN-- (LEN) and PulteGroupPHM-- (PHM), which have seen their valuations outperform the broader market by 8–10% since January 2025. Additionally, materials suppliers such as CaterpillarCAT-- (CAT) and Vulcan MaterialsVMC-- (VMC) benefit from increased infrastructure spending and residential construction activity.

Consumer Staples: Resilience Amid Leisure Sector Weakness

While the Leisure Products sector has underperformed due to households reallocating budgets toward housing expenses, the broader Consumer Staples sector has demonstrated resilience. A 10% rise in the MBA Refinance Index typically correlates with an 8% underperformance in the Consumer Discretionary sector, as seen in 2025 with CarnivalCCL-- (CCL) and other leisure stocks. However, staples-focused companies like Procter & GamblePG-- (PG) and Coca-ColaKO-- (KO) have maintained stable earnings, benefiting from essential demand and pricing power.

This divergence creates a compelling case for overweighting staples in a diversified portfolio. With refinance activity remaining 25% higher than the prior year, discretionary spending is likely to remain constrained for at least the remainder of 2025. Consumer Staples, with its low volatility and defensive characteristics, offers a counterbalance to the cyclical risks in leisure and construction.

Strategic Investment Considerations

- Overweight Construction and Materials: Position for continued housing market activity by allocating to construction and infrastructure stocks. Monitor the August housing starts report and September Fed meetings for confirmation of rate-cut delays.

- Underweight Leisure-Dependent Assets: Reduce exposure to companies like Carnival and Royal Caribbean until refinance activity moderates, which is unlikely before Q1 2026.

- Balance with Consumer Staples: Use staples as a defensive hedge against broader economic uncertainty. Look for undervalued plays in packaged goods and utilities.

- Watch Mortgage REITs Closely: While traditional banks benefit from refinance fees, mortgage REITs face prepayment risks. Avoid overexposure to companies like Annaly Capital ManagementNLY-- (NLY) unless rates stabilize.

Conclusion

The U.S. MBA Mortgage Refinance Index is more than a mortgage market indicator—it is a lens through which to view broader economic and sectoral shifts. As refinance activity remains elevated despite short-term rate hikes, investors should prioritize construction and consumer staples while avoiding overleveraged leisure sectors. By aligning portfolios with these dynamics, investors can navigate 2025's housing-driven volatility with strategic clarity.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet