Housing Market Deterioration: A Systemic Risk to Consumer Spending and Economic Growth

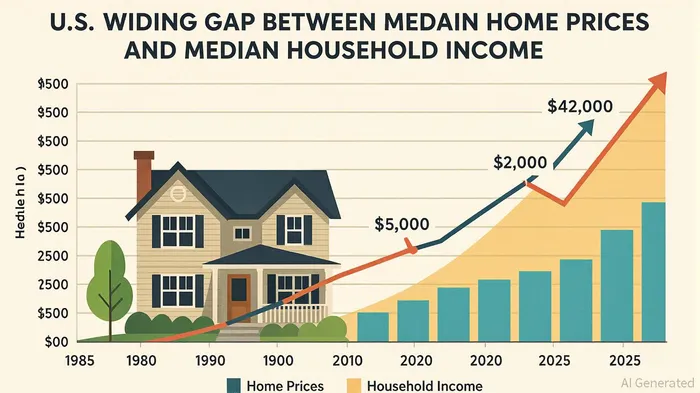

The U.S. housing market is at a crossroads. For decades, homeownership has been the cornerstone of American wealth accumulation, but the affordability crisis now threatening households across the country risks unraveling this foundation. By 2025, the median home price-to-income ratio has soared to 4.6, up from 3.5 in 1985, while mortgage rates hover stubbornly above 6.5%. This combination of elevated prices, constrained supply, and rising borrowing costs is not just a housing issue—it is a systemic risk to consumer spending, household balance sheets, and broader economic growth.

The Affordability Crisis: A Drag on Household Balance Sheets

The data is unequivocal: housing costs now consume a staggering 44.6% of the median household's income, far exceeding the 30% threshold deemed sustainable. In cities like Los Angeles (12.2) and San Francisco (10.0), the price-to-income ratio has reached levels that render homeownership a distant dream for most. Even in more affordable regions, the burden is mounting. A 20% down payment on a median-priced home requires over a year's worth of income for many households, while monthly mortgage payments account for 35% of their earnings.

This strain is reshaping household behavior. Savings rates have plummeted as families divert resources to housing, while discretionary spending—on everything from travel to education—has contracted. The Federal Reserve's rate hikes, intended to curb inflation, have inadvertently exacerbated the problem. With 30-year fixed rates at 6.8%, refinancing incentives are scarce, locking in a “lock-in effect” that keeps inventory low and prices elevated. Meanwhile, the shadow of the 2008 crisis looms: while today's homeowners hold stronger equity positions, the risk of a prolonged correction remains, particularly in overvalued coastal markets.

Regional Disparities and the Path to Correction

The housing market's pain is not evenly distributed. The South and West, where inventory has rebounded and prices have softened, are seeing early signs of correction. Austin, Texas, for example, has experienced a 15% drop in median prices over three years, while Miami's market has cooled by 19%. These regions, however, face their own challenges: population outflows and weak demand threaten to deepen declines. In contrast, the Northeast and Midwest remain stubbornly tight, with limited supply and restrictive zoning laws keeping prices high.

The Federal Reserve's reluctance to cut rates aggressively—fearing a surge in demand that could reignite price inflation—means affordability will remain a drag on consumer confidence. Yet, the market is not without opportunity. Undervalued real estate sectors in the South and West, where inventory is rising and prices are stabilizing, present a compelling case for long-term investors. Similarly, financial institutionsFISI-- that can navigate the shifting landscape—whether through mortgage innovation or policy-driven reforms—stand to benefit from a market recalibration.

Investment Opportunities in a Shifting Landscape

For investors, the key lies in identifying sectors poised to thrive amid—or profit from—the current turmoil.

Undervalued Real Estate Markets

Regions like Louisiana and Texas, where Zillow predicts price declines of 5% or more by 2026, offer attractive entry points. Houma and Lake Charles, for instance, are seeing inventory rise and demand wane, creating a buyer's market. REITs and developers with exposure to these areas could see gains as prices stabilize and construction activity picks up.Financial Sector Plays

Mortgage lenders and insurance companies are navigating a high-rate environment. While traditional banks face margin compression, non-bank lenders like Quicken Loans (QLOAN) and PennyMac (PMT) are adapting with flexible products. Additionally, companies specializing in risk mitigation—such as insurance providers offering coverage for price declines—could see demand as uncertainty persists.Policy-Driven Sectors

A potential shift in housing policy—whether through zoning reforms, federal land development, or expanded affordable housing programs—could unlock value in construction and infrastructure. Companies like LennarLEN-- (LEN) and D.R. Horton (DHI), which have scaled back operations in high-cost markets, may pivot to regions with more favorable conditions.

The Road Ahead: A Call for Strategic Patience

The housing market's deterioration is not a fleeting blip but a structural challenge with far-reaching implications. For households, the burden of unaffordable housing will continue to weigh on savings and consumption. For policymakers, the task is to balance rate stability with supply-side solutions. And for investors, the opportunity lies in identifying undervalued assets and sectors that can weather—or capitalize on—the storm.

The lesson from 2008 is clear: a housing crisis can ripple through the economy for years. But today's market, with its stronger equity positions and tighter lending standards, is less vulnerable to a catastrophic collapse. What remains is a landscape of risk and reward, where strategic patience and a nuanced understanding of regional dynamics will separate the winners from the losers.

As the market recalibrates, one thing is certain: the path to recovery will not be linear. But for those willing to look beyond the headlines, the rewards could be substantial.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet