Home Equity Erosion and Inflationary Pressures: A Looming Wealth Transfer from Homeowners

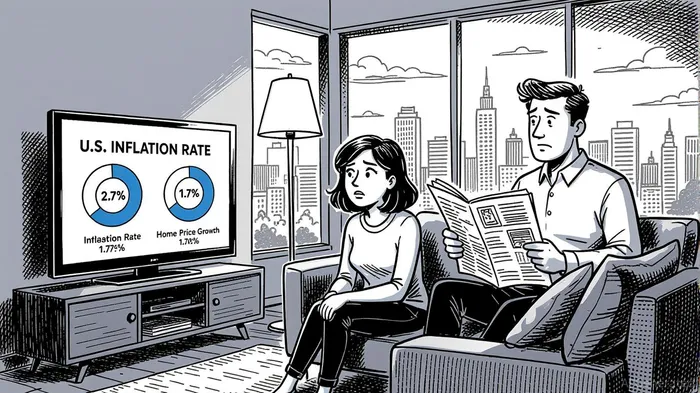

The U.S. housing market in 2025 is caught in a paradox: while home prices continue to rise, their real value is eroding faster than ever. With inflation at 2.7% and home price growth at 1.7%, the misalignment between rising costs and sluggish appreciation is creating a structural drag on equity accumulation. This dynamic, compounded by asset-liability mismatches in residential real estate, is triggering a quiet but profound wealth transfer—from homeowners to alternative asset classes and financial services. For investors, the implications are clear: the era of residential real estate as a guaranteed wealth engine is waning, and capital is fleeing toward more resilient opportunities.

The Equity Erosion Equation

Home equity has long been a cornerstone of American wealth, but today's environment is undermining its value. The average annual cost of homeownership now exceeds $25,000, driven by surging insurance, property taxes, and maintenance expenses. These costs are rising at 70% since 2020, far outpacing the 1.7% annual home price growth. Meanwhile, fixed-rate mortgages remain locked in at 6.7%, trapping new buyers in a high-cost cycle while existing homeowners—many with mortgages at 4.03%—are reluctant to sell, exacerbating inventory shortages.

The result is a double-edged sword: homeowners are paying more to maintain their properties but seeing minimal real gains in equity. For example, a homeowner with a $400,000 property and a 20% down payment has $80,000 in equity. If inflation erodes purchasing power by 2.7% annually, that $80,000 is effectively worth $70,000 in 2025 dollars. Add in rising variable costs, and the erosion becomes existential. This misalignment is not just a personal finance issue—it's a systemic risk to the broader economy, as homeownership rates and consumer spending are inextricably linked.

Asset-Liability Mismatch and the Lock-In Effect

The Federal Reserve's 4.25%-4.50% policy rate has created a 250-basis-point gap with 30-year fixed-rate mortgages at 6.59%. This disparity has entrenched a “lock-in effect,” where homeowners with low-rate mortgages are hesitant to sell, fearing refinancing at higher rates. The consequence? Housing inventory remains 30% below pre-pandemic levels, creating a supply-demand imbalance that stifles price growth.

For investors, this mismatch is a red flag. Traditional real estate assumptions—such as long-term appreciation and stable cash flows—are being upended. First-time buyers, particularly Gen Z and Millennials, are adopting unconventional strategies (e.g., co-purchasing, side jobs) to navigate affordability challenges. Yet, even these efforts are insufficient in a market where inventory constraints and high borrowing costs dominate. The result is a capital flight from residential real estate into alternative asset classes that offer better liquidity and resilience.

Capital Reallocation: The Rise of Multifamily and Affordable Housing

As residential real estate struggles, capital is flowing into multifamily and affordable housing. The multifamily sector, for instance, has seen robust demand fundamentals: Q1 2025 unit absorption hit 138,300, with occupancy rates stabilizing at 94.4%. Rent growth, though modest (1.5–1.6% annually), is supported by demographic tailwinds and policy-driven incentives.

Affordable housing is another beneficiary. The One Big Beautiful Bill Act has boosted Low-Income Housing Tax Credit (LIHTC) funding by 12.5%, while 22 private investment managers raised $18.4 billion for affordable housing units between 2019 and 2024. These funds are allocating 24% of commitments to new developments—a sharp increase from 7% in prior years. Investors are drawn to the sector's stable cash flows and policy-driven demand, particularly as market-rate projects contract.

Build-to-rent (BTR) is also gaining traction, despite a near-term slowdown in completions. The sector's 3.48 million-unit pipeline reflects long-term confidence in multifamily fundamentals. While BTR deliveries are expected to halve by 2026, the focus on climate-resilient and urban properties positions it as a hedge against macroeconomic volatility.

Financial Services Adaptations: Home Equity Lending and Risk Management

Financial services institutions are recalibrating their strategies to address the shifting landscape. Home equity lending, for example, has become a growth engine. Tappable home equity reached $11 trillion by year-end 2024, with the average homeowner holding $203,000 in equity. Lenders are capitalizing on this by expanding HELOC and home equity loan offerings, which now average 8.10% and 8.22% interest rates, respectively.

However, caution is warranted. The U.S. household savings rate is at a 20-year low, and economic uncertainty—driven by potential rate hikes and rising unemployment—could trigger defaults. Lenders are adopting automated valuations and tighter underwriting standards to mitigate risk, but the sector remains vulnerable to macroeconomic shocks.

Investment Implications and Strategic Recommendations

For investors, the key takeaway is to pivot from speculative single-family home purchases to diversified, resilient asset classes. Multifamily and affordable housing offer stable cash flows and policy-driven growth, while BTR provides long-term value in urban markets. Financial services firms with expertise in home equity lending and risk management are also attractive, though their exposure to economic volatility requires careful due diligence.

Homeowners, meanwhile, should consider leveraging home equity strategically. Debt consolidation via HELOCs or home equity loans can mitigate high-interest credit card debt, but over-leveraging remains a risk. The untapped $500 billion in equity suggests a cautious approach is warranted until economic stability returns.

In conclusion, the misalignment between inflation and home price growth is accelerating a wealth transfer from residential real estate to alternative assets. Investors who recognize this shift early will be well-positioned to capitalize on the next phase of capital reallocation—a market defined by resilience, adaptability, and strategic foresight.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet