The Hidden Financial Costs of Overspending on Credit Cards and How to Mitigate Them

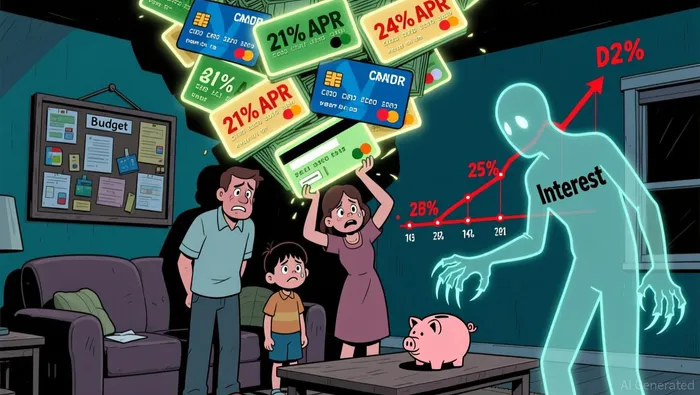

The average American's relationship with credit cards has become a high-stakes game of financial whack-a-mole. With interest rates climbing to stratospheric levels and debt accumulation outpacing income growth, the hidden costs of overspending are no longer abstract-they're existential. As of Q3 2025, the average credit card interest rate for all cards stands at 21.39%, while new offers hit a staggering 24.04%. These numbers aren't just statistics; they're a ticking time bomb for consumers who carry balances. For every dollar spent on a card with a 22% APR, you're effectively paying $0.22 in interest before you've even touched the next paycheck.

The scale of the problem is equally alarming. By July 2025, the average credit card debt per American had ballooned to $6,492, with 46% of cardholders carrying a balance. This isn't just a millennial crisis-Gen Xers and boomers are equally implicated, with 55% and 44% of those demographics, respectively, struggling to pay off their cards. The consequences? A staggering 64% of debtors have delayed or avoided major financial decisions, from home purchases to retirement planning, because of their obligations.

But the true hidden cost isn't just the interest-it's the corrosive effect on credit scores. Total credit card balances are projected to hit $1.136 trillion by year-end, yet delinquency rates remain stubbornly stable. This paradox suggests a shift in consumer behavior: people are taking on more debt but managing it more cautiously. However, high APRs remain a vulnerability, particularly for those with lower credit scores, who face the highest rates and the steepest climb to financial recovery.

But the true hidden cost isn't just the interest-it's the corrosive effect on credit scores. Total credit card balances are projected to hit $1.136 trillion by year-end, yet delinquency rates remain stubbornly stable. This paradox suggests a shift in consumer behavior: people are taking on more debt but managing it more cautiously. However, high APRs remain a vulnerability, particularly for those with lower credit scores, who face the highest rates and the steepest climb to financial recovery.

Here's where the strategy must pivot. Credit scores are no longer just about payment history-they're influenced by medical debt reporting rules, new scoring models like VantageScore 4.0, and even how rent or BNPL (Buy Now, Pay Later) payments are treated. For example, unpaid medical debts under $500 are no longer reported, a change that could spare millions from unnecessary score damage. Yet, the same can't be said for credit cards. A single missed payment, even by a day, can slash a score by 100 points or more.

To mitigate these risks, consumers must adopt a multi-pronged approach. First, monitor credit reports religiously. Errors are common, and catching them early can prevent long-term damage. Second, automate payments to ensure on-time payments, which remain the single most critical factor in credit scoring. Third, avoid maxing out credit cards. Utilization rates above 30% send red flags to lenders, even if payments are made on time.

Policymakers are also stepping in. Bipartisan proposals to cap credit card interest rates could alleviate pressure on borrowers, potentially saving billions in unnecessary fees. While these measures are still in the legislative pipeline, individuals can't wait for Washington-they need to act now.

For investors and financial advisors, the lesson is clear: credit card debt isn't just a personal finance issue; it's a systemic risk. As delinquency rates stabilize and consumers grow more disciplined, the broader economy may avoid a debt-driven downturn. But for individuals, the stakes remain high. The path forward lies in strategic debt management-paying balances in full, leveraging new credit scoring rules, and treating credit cards as tools, not lifelines.

In the end, the hidden costs of overspending aren't just in the interest charges. They're in the lost opportunities, the dented credit scores, and the long-term financial paralysis that follows. The time to act is now-before the next interest rate hike turns a manageable debt into a generational burden.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet