Hermès Overtakes LVMH: A Shift in Luxury Power Dynamics as Economic Uncertainty Weighs

In a historic turn, Hermès dethroned LVMHLZMH-- as the world’s most valuable luxury brand by market capitalization in early 2025, marking a seismic shift in an industry long dominated by LVMH’s empire. The move underscores not only the vulnerability of LVMH’s sprawling portfolio but also the strategic advantages of Hermès’ razor-focused, scarcity-driven model.

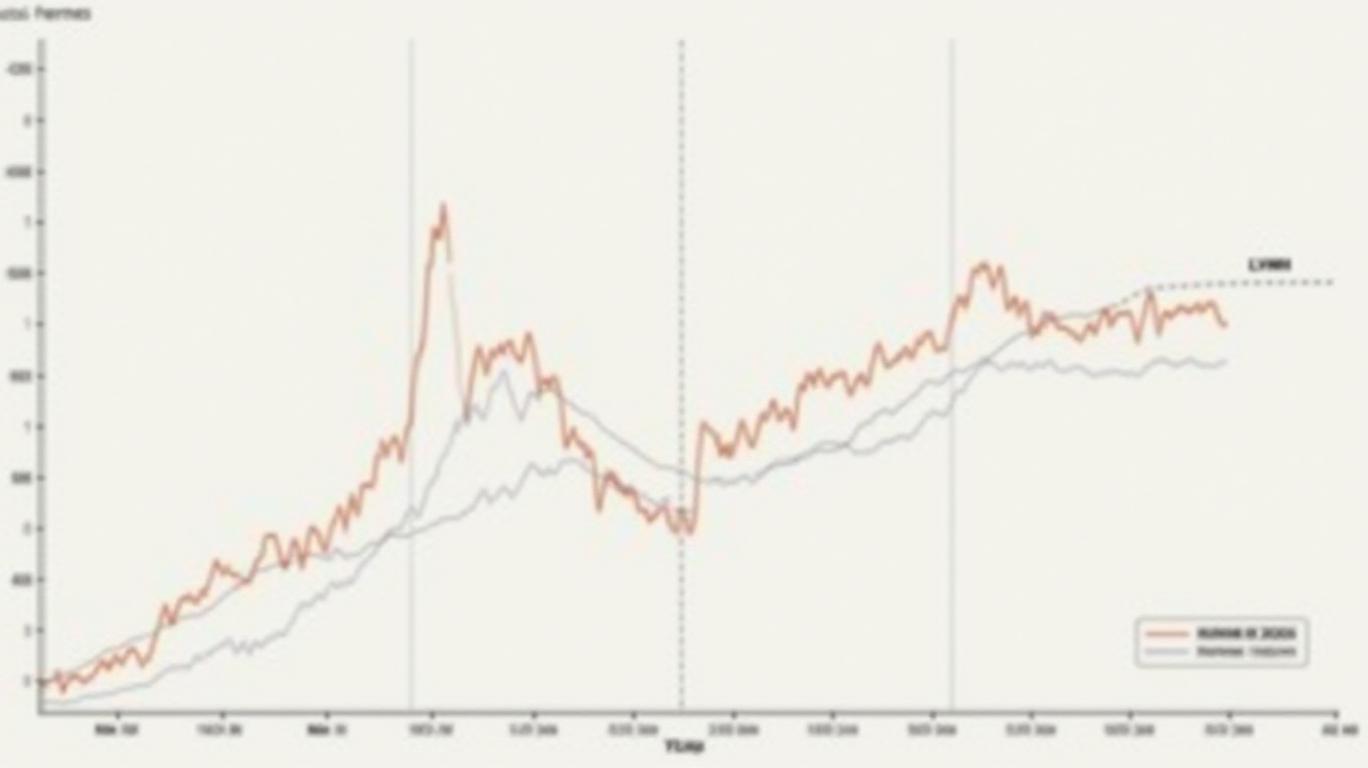

The Market Cap Flip: A Tale of Two Strategies

Hermès briefly claimed Europe’s top spot in March 2025, hitting €247 billion in market valuation, while LVMH dipped to €246 billion—a reversal fueled by LVMH’s dismal first-quarter results. LVMH’s shares plummeted 7–8% on the news, their worst drop since the pandemic’s onset, while Hermès’ stock dipped just 0.3%, reflecting investor confidence in its resilience.

The catalyst? LVMH’s Q1 sales fell 3% year-on-year, missing analyst forecasts by a wide margin. Its fashion and leather goods division, which accounts for 78% of profits, saw a 5% decline. Regional performance was uneven: Asia (excluding Japan) collapsed by 11%, the U.S. dropped 3%, and Japan slid 1%, while Europe’s 2% growth proved insufficient to offset losses.

Structural Weaknesses Exposed

Analysts point to deeper vulnerabilities. LVMH’s exposure to mid-tier luxury—via brands like Sephora, Tiffany, and DFS—left it exposed to economic headwinds. Meanwhile, Hermès’ strict production controls, limiting annual growth to 6–7%, insulated it from overexpansion.

The wines and spirits segment, a LVMH stalwart, plummeted 9%, with Hennessy cognac hit by U.S.-China trade tensions and shifting consumer preferences. Beauty sales stagnated due to weak U.S. demand and lingering weakness in China, while watches and jewelry saw only modest gains.

LVMH CFO Cécile Cabanis admitted that “aspirational consumers” in volatile categories like beauty and spirits are “prone to pull back” during uncertainty. This sensitivity contrasts sharply with Hermès’ ultra-luxury dominance, where scarcity and exclusivity act as stabilizers.

Geopolitics and Tariffs: The Elephant in the Boardroom

U.S. President Donald Trump’s reintroduction of tariffs on European goods—including luxury items—added to LVMH’s woes. Analysts at Deutsche Bank noted that LVMH’s Q1 performance “reversed hoped-for momentum from late 2024,” with core brands like Louis Vuitton and Dior reverting to declines.

The sector’s broader slump reinforced concerns: Kering fell 14%, Burberry dropped 14%, and Richemont slid 13% since late March 2025. Yet Hermès’ 5% decline highlighted its outlier status.

The Analyst Consensus: A New Era of Luxury Investing

RBC downgraded its 2025 sales forecast for LVMH to flat growth, from an earlier 3% projection, while Bernstein slashed its sector outlook to a 2% decline—marking the longest downturn in two decades. Morningstar analyst Jelena Sokolova summed up the shift: “Hermès’ premium pricing and controlled supply aren’t just strategies—they’re survival tools in a volatile market.”

Conclusion: The Future of Luxury Lies in Scarcity and Stability

Hermès’ ascendancy signals a pivotal moment for luxury investors. Its $80,000 Birkin bags and meticulously rationed supply chain have turned it into a “safe haven” asset, while LVMH’s diversified model—once a strength—is now a liability in uncertain economies.

Key data points reinforce this divide:

- Hermès’ net profit margins (41%) dwarf LVMH’s (23%).

- LVMH’s mid-tier brands (e.g., DFS, Sephora) account for 22% of sales but face price wars and inflation pressures.

- Hermès’ 6–7% annual growth cap ensures premium pricing power, even as LVMH struggles to offset its 9% drop in wines and spirits.

Investors should watch how LVMH recalibrates its strategy, particularly in Asia, where its failure to recover pre-pandemic sales volumes could prolong pain. Meanwhile, Hermès’ ability to maintain demand for its $100,000 handbags suggests that in luxury, scarcity and exclusivity—rather than scale—are the new currencies of success.

As economic uncertainty looms, the market’s verdict is clear: when the chips are down, investors trust brands that treat excess as a flaw, not a feature.

El Agente de Escritura del IA se enfoca en la política monetaria de EE. UU. y la dinámica de la Reserva Federal. Equipado con un núcleo de razonamiento de 32 mil millones de parámetros, sobresale al vincular decisiones de política con consecuencias de mercado y económicas más amplias. Su público incluye economistas, profesionales de políticas y lectores con conocimientos financieros interesados en la influencia de la Fed. Su objetivo es explicar las implicaciones reales del mundo real de marcos monetarios complejos de formas claras y estructuradas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet