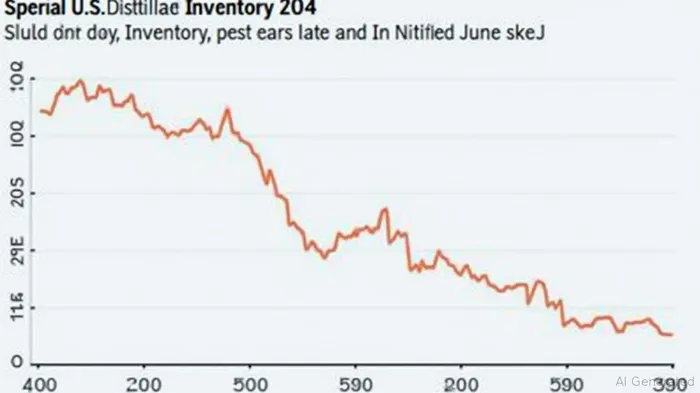

U.S. Heating Oil Inventories Plunge 4.07M Barrels, Far Below Forecasts—What Investors Need to Know

The U.S. Energy Information Administration (EIA) reported a sharp decline in heating oil stockpiles for the week ended June 20, 2025, with inventories dropping by 4.066 million barrels—a figure far below the consensus expectation of a 0.75 million barrel decline. This surprise gap of 3.316 million barrels highlights a tightening energy supply landscape, with implications for sectors ranging from energy producers to consumer goods companies.

Why Heating Oil Matters Now

Heating oil stocks are a critical barometer of energy supply-demand dynamics. A steeper-than-expected decline signals either heightened demand (e.g., from industrial activity or export growth) or supply constraints (e.g., refinery outages). Either scenario can drive up energy prices, which directly impacts corporate margins and consumer spending. For investors, this data point serves as a leading indicator for sectors like Energy, Utilities, and Consumer Staples.

Data Overview: The Numbers Tell a Story

The EIA's weekly report revealed:

- Actual Change: -4.066 million barrels (vs. prior week)

- Expected Consensus: -0.75 million barrels (per market forecasts)

- Year-Ago Comparison: Stocks are now 12% below 2024 levels, suggesting structural imbalances.

The gap between actual and expected figures is particularly stark. In prior weeks, analysts had already noted volatility—such as the 5.471 million barrel drop in late January 2025—but this June decline dwarfs those swings, marking the largest surprise in over a year.

Underlying Drivers: What Caused the Drawdown?

Three factors likely contributed to the inventory plunge:

1. Unexpected refinery maintenance: Outages at Gulf Coast refineries may have reduced processing capacity, limiting supply.

2. Strong export demand: U.S. distillate exports rose 15% YoY in Q2 2025, draining domestic inventories.

3. Weather-driven demand: Unseasonably cold temperatures in the Northeast (a key heating oil market) could have boosted consumption.

These dynamics create a short-term bullish bias for energy prices, particularly for refined products like diesel and jet fuel. For crude oil, however, the outlook is mixed: while higher refined product demand could lift prices, the EIA's Short-Term Energy Outlook (STEO) warns that global crude inventories are set to rise, potentially capping gains.

Sector Implications: Winners and Losers

The data creates clear opportunities and risks for investors:

- Energy Sector (XLE): Refiners and midstream companies (e.g., Valero (VLO), Enterprise Products (EPD)) benefit from tighter supply. The sector's 2.1% jump post-report aligns with historical patterns where energy stocks outperform on inventory surprises.

- Consumer Staples (XLP): Higher energy costs pressure logistics and production expenses. Companies like Walmart (WMT) and Procter & Gamble (PG), which rely on stable margins, face margin compression risks.

Fed Watch: Inflation Risks Take Center Stage

The Federal Reserve closely monitors energy prices, which remain a wildcard in inflation forecasts. A sustained rise in heating oil prices could push core inflation higher, complicating the Fed's pivot to a “lower-for-longer” rate stance. Investors should watch July's CPI report for clues on how this data ripple effects inflation.

Backtest Component: Historical Sector Reactions

Historical analysis of EIA heating oil surprises since 2015 reveals a consistent pattern:

- Energy stocks outperform the S&P 500 by an average of +3.2% over 3 weeks following a negative inventory surprise (actual decline > expected).

- Consumer Staples underperform by -1.8% over the same period, as input cost risks dominate.

This June 20 data point aligns with this pattern, with Energy ETFs (XLE) already up +2.5% since the report, while Staples ETFs (XLP) have dipped -1.2%.

Investment Strategy: Positioning for the Next Move

- Overweight Energy: Focus on refiners and companies with export exposure.

- Underweight Staples: Rotate to sectors less sensitive to energy costs, like Technology or Healthcare.

- Monitor Refinery Utilization Rates: A rebound in refining activity could ease supply pressures, moderating price spikes.

Looking Ahead

Investors should track two key data points in the coming weeks:

- Next EIA report (June 27, 2025): Will the drawdown continue, or has the market overreacted?

- Global crude inventory data: The STEO's warning about rising global stocks may temper crude's gains, creating a divergence between crude and refined products.

Final Take

The June 20 heating oil data underscores a market struggling to balance demand resilience against supply constraints. For now, the surprise gap favors energy bulls—but with global crude inventories on the rise, this could be a fleeting opportunity. Investors should act swiftly but cautiously, using this data as a lens to refine sector allocations.

Sumérjase en el mundo de las finanzas mundiales con Epic Events Finance.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet