Healthcare Stocks Surge as Tech Faces AI Bubble Fears: November 2025 Sector Rotation Reveals Defensive Winners

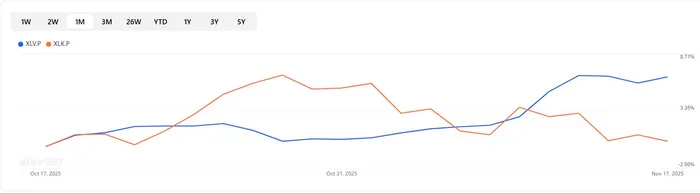

While investors fret over frothy AI multiples and hardware bottlenecks, capital is quietly rotating into healthcare. Month-to-date, Health Care Select Sector SPDR (XLV) leads the S&P 500 sector stack even as Technology (XLK) sags helped by a burst of pharma/biotech strength and attractive relative valuations.

Investor Flows: Healthcare in Demand

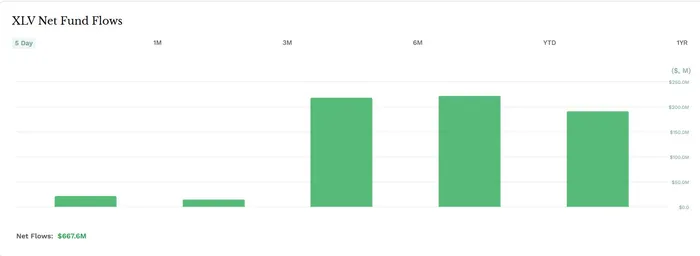

Money is now speaking louder than ever. Healthcare stocks just saw their biggest weekly inflows since January 2021, confirming the sector’s growing reputation as a defensive haven. With higher interest rate volatility and inflation uncertainty clouding growth prospects for tech, investors are seeking stability and resilient cash flows in healthcare.

Source: etf.com

Valuations: Healthcare Remains a Bargain

One key driver behind the rotation is valuation. Even with this month’s tech pullback, technology stocks are still priced at elevated forward P/E multiples. The S&P 500, tracked by the Vanguard S&P 500 ETF (NYSE: VOO), trades at 23x forward earnings, but the Technology Select Sector SPDR Fund (NYSE: XLK) hovers around 30x. Healthcare (XLV), meanwhile, trades at just 20x forward earnings, offering relative value compared to both tech and the broader market and joining traditionally inexpensive sectors like financials, utilities, and energy.

Leaders of the move

Top healthcare performers through mid-November include Eli Lilly (LLY), Henry Schein (HSIC), Amgen (AMGN), Incyte (INCY), Cigna (CI), Steris (STE), and IDEXX (IDXX). Notably, LLY continues to pull the complex higher on obesity/diabetes momentum and pipeline breadth.

Pharma/biotech setup: more than just “defensive”

Beyond staples-like resilience, biotech’s cycle is improving: XBI’s rebound, better market reception to positive clinical data, and a pickup in M&A as Big Pharma fills looming LOE (loss-of-exclusivity) gaps. A cleaned-up small/mid-cap cohort post-drawdown also helps.

Risks to the thesis

AI re-accelerates on capacity adds. If power/transmission constraints ease faster than expected, AI leaders could quickly reclaim market leadership and reverse some rotation.

Policy & pricing. Drug-pricing headlines or reimbursement changes can hit sentiment, especially in managed care and high-exposure therapeutic franchises. (Balance: ongoing M&A and launch execution can offset.)

Watchlist into year-end

LLY: Execution on incretin demand and next-wave readouts; any supply updates.

AMGN: Pipeline/newsflow and Repatha/T-cell therapy optionality; M&A stance.

CI: Utilization trends and margin commentary; managed-care sentiment swing factor.

Selective biotech (XBI proxy): Data/M&A cadence sustaining the group’s higher lows.

Bottom line

If AI is pausing to catch its infrastructural breath, healthcare looks like the market’s relief valve: cheaper on earnings, richer in catalysts, and less tethered to the power-hungry AI build-out. For diversified investors, keeping a quality-tilted healthcare sleeve makes sense as November’s rotation plays out—while staying nimble for an eventual AI second wind.

This article is for informational purposes only and is not investment advice.

Quickly compare XLV, XLK, XBI side by side with our ETF Compare Tool

Market Radar delivers concise, daily trading ideas by tracking everything from options activity and market sentiment to high-profile political trades.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet