Health Insurance Premium Hikes: A Hidden Drag on Consumer Spending and Market Growth

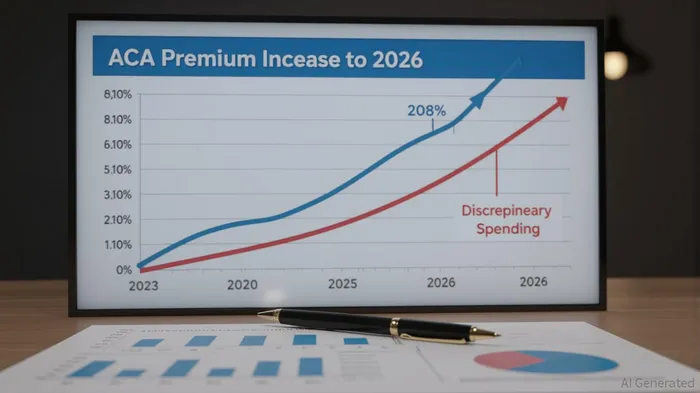

The Affordable Care Act (ACA) Marketplace premium hikes from 2023 to 2026 are not merely a healthcare issue—they are a macroeconomic force reshaping consumer behavior, regional economies, and equity markets. With median proposed increases of 18% for 2026 (up from 7% in 2025), these hikes are driven by a toxic mix of rising medical costs, inflation, and policy uncertainty. The expiration of enhanced premium tax credits at year-end 2025 looms large, threatening to push out-of-pocket premiums up by over 75% for many enrollees. This creates a self-reinforcing cycle: healthier, price-sensitive individuals drop coverage, worsening risk pools and further inflating premiums.

The Macroeconomic Drag: Consumer Spending and GDP

Healthcare already accounts for 18% of U.S. GDP, and ACA premium hikes are accelerating this trend. While higher healthcare spending directly boosts GDP through employment and investment in the sector, the indirect drag on consumer demand is profound. Households facing steeper premiums are reallocating budgets away from discretionary spending. For example, retail apparel searches have stagnated, while luxury goods interest has plummeted. The Congressional Budget Office estimates that 3.8 million people could lose coverage by 2026, compounding the strain on disposable income.

The drag on GDP is twofold. First, rising healthcare costs crowd out spending on other goods and services, slowing broader economic growth. Second, reduced access to affordable care may lower workforce productivity, as unmet health needs lead to absenteeism and reduced efficiency. The Congressional Budget Office projects that up to 2.2 million Americans could forgo coverage by 2026, a loss that could ripple through the economy.

Regional Disparities and Policy Gaps

The impact of ACA hikes is uneven. States that have not expanded Medicaid—such as Texas and Florida—face sharper challenges. In these regions, the coverage gap leaves millions ineligible for subsidies but unable to afford Marketplace plans. For example, a family of four in a non-expansion state earning 200% of the federal poverty level could see premiums jump from $100 to $326 monthly, a 226% increase. Conversely, states like Maryland and Oregon, which have implemented targeted subsidies or utilization management policies for high-cost drugs like GLP-1s, have mitigated some of the financial strain.

The expiration of enhanced tax credits will exacerbate these disparities. By 2035, 4.2 million more people could become uninsured, with the heaviest toll in non-expansion states. This creates a fragmented economic landscape, where regions with weak policy responses face steeper declines in consumer spending and business investment.

Sector-Specific Impacts: Healthcare, Retail, and Financials

Healthcare Sector: Insurers and drugmakers are caught in a cost-containment arms race. Companies like UnitedHealth GroupUNH-- and Anthem are factoring in 8–10% medical trend assumptions for 2026, driven by rising drug costs and provider consolidation. Meanwhile, innovators in telehealth (e.g., Teladoc Health) and generic drugs (e.g., Amneal Pharmaceuticals) are gaining traction as investors seek solutions to affordability crises.

Retail Sector: The shift in consumer priorities is evident. Retailers specializing in discretionary goods—luxury brands, apparel, and travel—are seeing weaker demand. Conversely, pharmacies and medical device firms are benefiting from increased utilization of high-cost treatments. However, this growth is offset by long-term risks: delayed care could lead to higher emergency room visits, straining retail healthcare providers.

Financial Sector: Banks and insurers are recalibrating risk models to account for ACA volatility. The potential expiration of tax credits has led to hedging strategies, including increased allocations to inflation-protected securities (TIPS) and short-term bonds. Financial institutionsFISI-- with significant exposure to ACA markets, such as those underwriting health plans, face margin pressures as premium increases outpace cost controls.

Investment Implications and Hedging Strategies

For investors, the ACA premium hikes present both risks and opportunities. Defensive plays in healthcare innovation and cost-containment technologies are likely to outperform. Conversely, traditional retail and luxury sectors face headwinds as consumer spending shifts.

- Healthcare Sector: Prioritize companies addressing affordability, such as telehealth platforms and generic drug manufacturers. Avoid insurers with high exposure to non-expansion states.

- Retail Sector: Overweight essential goods and medical device firms. Underweight discretionary categories like luxury apparel.

- Financial Sector: Favor institutions with diversified healthcare portfolios and hedging instruments like TIPS. Monitor insurers' rate filings for early signals of risk pool deterioration.

The ACA premium hikes are a macroeconomic wildcard, with the potential to reshape consumer behavior and sector dynamics for years. Investors who recognize this shift early—by hedging against healthcare inflation and capitalizing on innovation—will be better positioned to navigate the evolving landscape.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet