Hawkish Kevin Warsh Nominated as Fed Chair: QT Accelerate, Volatility Ahead

U.S. President Donald Trump announced the nomination of former Federal Reserve Governor Kevin Warsh as the next Chair of the Federal Reserve. With the uncertainty resolved, U.S. equities rallied in the short term.

During Trump’s first presidential term, both Jerome Powell and Kevin Warsh were considered for the Fed Chair role, with Powell ultimately selected. Warsh’s nomination this time means that both of Trump’s preferred candidates will have led the Federal Reserve.

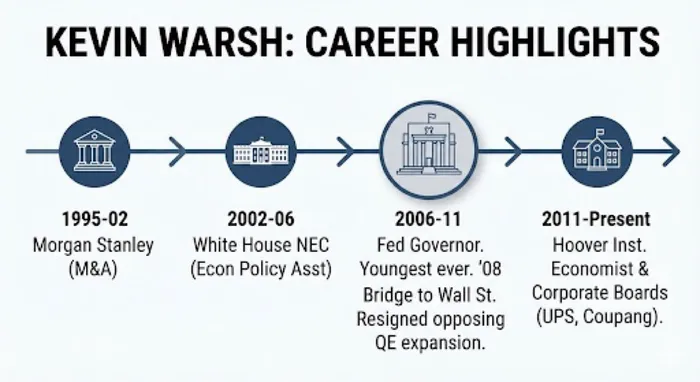

Warsh served as a Federal Reserve Governor from 2006 to 2011, spanning the 2008 Global Financial Crisis, giving him extensive crisis-management experience. During his tenure at the Fed, Warsh was known for his hawkish monetary policy stance. In recent years, however, he has shifted toward supporting Trump’s tariff policies and faster rate cuts, earning Trump’s favor.

Deutsche Bank notes that if Warsh becomes Fed Chair, his policy framework could feature a distinctive combination of rate cuts alongside balance sheet reduction (QT).

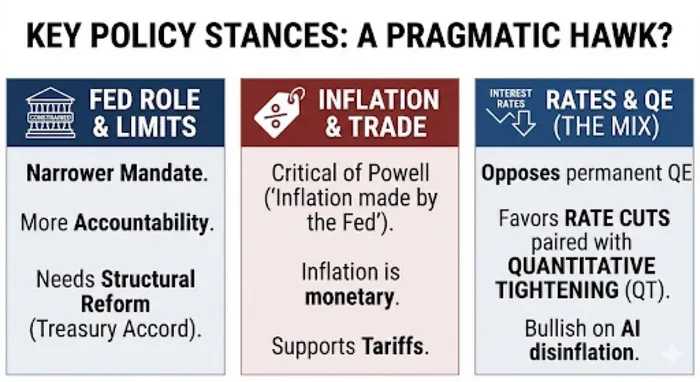

China Merchants Securities believes Warsh is the most hawkish among the potential candidates, placing greater emphasis on discipline and Federal Reserve independence while supporting quantitative tightening. In the short term, this would be negative for U.S. Treasuries and positive for the U.S. dollar index. Although Warsh currently aligns with Trump’s policy stance, divergence could emerge in the medium term, potentially leading to renewed political pressure similar to what Powell faced, increasing volatility in risk assets.

“If the President wanted someone weak, I wouldn’t get this job,” Warsh once said during an interview, underscoring his commitment to defending the Fed’s independence rather than simply following Trump’s directives.

Notably, Warsh has long criticized quantitative easing (QE) and the Federal Reserve’s excessive protection of financial markets—the so-called “Fed Put.” If U.S. equities experience significant volatility, Warsh may choose to remain on the sidelines rather than intervene to rescue markets.

Sonu Varghese, Global Macro Strategist at Carson Group, noted that Warsh has historically been a hawk, despite recently echoing Trump’s calls for rate cuts. If Warsh enters the Fed advocating aggressive rate cuts, his credibility in persuading others of the need for further easing may be limited. This could result in a deeply divided FOMC that ultimately does not cut rates at all. In the near term, a potentially more hawkish Fed could increase market volatility.

In a recent in-depth interview, Warsh stated bluntly that inflation is the Federal Reserve’s responsibility and cannot be blamed on external factors. Addressing the dilemma of high interest rates, he argued that reducing the balance sheet could create room for lower rates: “If we quiet the printing press a bit, interest rates could actually be lower.”

Warsh pointed out that after the Great Moderation, the Fed mistakenly believed inflation was dead and maintained an excessively large balance sheet during non-crisis periods. “When you print a trillion here and a trillion there, inflation will eventually show up,” he warned. The Fed’s failure to unwind stimulus during the relatively stable 2010–2020 period forced it to cross more red lines during real crises, such as the pandemic, contributing to today’s inflationary consequences.

As a potential successor to the Fed Chair, Warsh has outlined a clear policy path: by restraining money creation, nominal interest rates can be lowered. This represents a crucial incremental insight—Warsh may favor controlling inflation through quantitative tightening, thereby creating room to reduce policy rates.

This approach is logically consistent with the Trump administration’s desire to lower borrowing costs. Warsh refers to this framework as “pragmatic monetarism,” arguing that the Federal Reserve and the Treasury must each “do their own jobs”: the Fed should manage interest rates, while the Treasury manages fiscal accounts. The two should reach a “new accord” to address rising debt servicing costs, rather than operating with blurred boundaries as in the past.

In response to concerns about “radical reform,” Warsh offered reassurance. He emphasized that the goal is not to “tear down” the Federal Reserve, but to rejuvenate it. He likened the process to restoring a great golf course—drawing inspiration from the past without being constrained by it. Warsh envisions not a recessionary U.S. economy, but an AI-driven productivity boom reminiscent of the Reagan era. With rational policymaking, he believes the U.S. economy will demonstrate remarkable resilience.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet