Hawkish Cut or January Shock? Fed Meeting Has Markets on Edge as Succession Drama Looms

The Federal Reserve’s final meeting of 2025 looks less like a routine year-end check-in and more like a stress test of its “data-dependent” mantra in a world short on data and long on politics. Policymakers convene Tuesday and are widely expected to deliver a third consecutive 25 bp rate cut on Wednesday at 2 p.m. ET, taking the funds rate to 3.50–3.75%. The real question for markets isn’t what happens this week, but what—if anything—Chair Jerome Powell is willing, and still able, to signal about 2026.

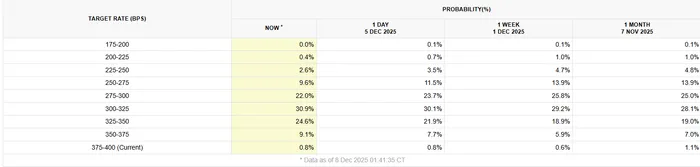

Futures markets put the odds of a cut in the high-80s to 90% range, but pricing beyond December is murky. The CME curve shows only about a 25% chance of another move in January and then a fuzzy cluster of expectations for one to three cuts in 2026. The consensus on the Street is for a “hawkish cut”: the Fed trims rates this week, then effectively tells markets to get comfortable with a long pause. Goldman SachsGS-- is one of the notable outliers, arguing Powell could surprise by keeping the door open to a January move—an upside risk for equities in a market braced for a tough-talking Fed.

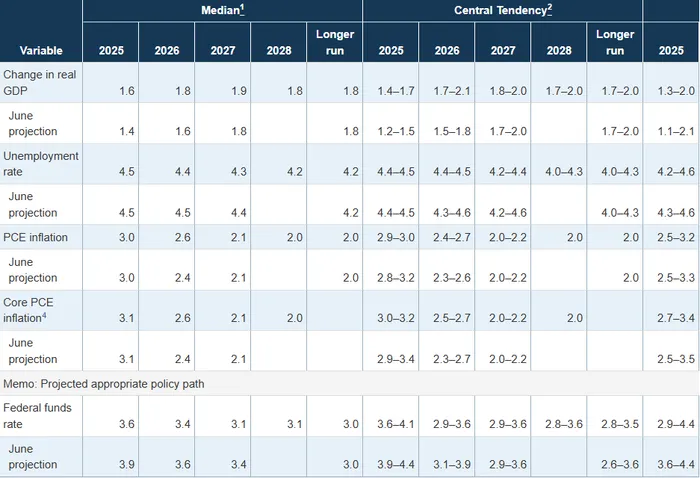

The updated Summary of Economic Projections (SEP) and dot plot will be the first place investors look for that signal. In September, the median projections mapped out a very gentle glide path: three cuts in 2025 followed by just one more in 2026 and another in 2027. For 2026, the Fed saw real GDP at 1.8%, unemployment at 4.4%, headline and core PCE at 2.6%, and the funds rate at 3.4%. By 2027, growth nudged up to 1.9%, unemployment dipped to 4.3%, inflation fell back to roughly 2.1%, and the policy rate only drifted down to 3.1%. In other words: disinflation in progress in 2026, inflation effectively back at target in 2027, yet rates still structurally higher than the pre-COVID era.

Dot Plot:

The September dot distribution told the same story. Most officials clustered between roughly 3.50–3.75% for 2025, sliding to the low-3s in 2026–27 and converging around a longer-run “neutral” rate near 2.5–2.75%. Cuts were coming, but this was slow normalization, not a sprint back to zero. On Wednesday, markets will be watching for three things: whether the 2026 and 2027 medians inch lower (signaling a bit more comfort with easing), whether the unemployment path is revised up to reflect a softer labor market, and whether any officials push the longer-run neutral rate higher again—a hawkish tell.

Complicating all of this is the Fed’s own admission that it’s flying through some data fog. The extended government shutdown has delayed key labor reports, robbing officials of an updated unemployment rate at precisely the moment when the jobs narrative is most contested. Private data like ADP are flashing weakness in small businesses and cyclical sectors, while initial claims remain surprisingly low. Consumer confidence has slumped to levels more consistent with recession than soft landing. It is not an ideal backdrop for “data-dependent” forward guidance, and markets know it.

That’s why the evolution of the statement language will carry so much weight. In the most recent statement, the Fed described economic activity as expanding at a “moderate pace,” noted that job gains had slowed and unemployment had edged up but remained low, and conceded that inflation had “moved up” earlier in the year and was still “somewhat elevated.” Crucially, the Committee judged that downside risks to employment had risen and cited this shift in the balance of risks as justification for its 25 bp cut to 3.75–4.00%. At the same time, it announced plans to end balance-sheet runoff on December 1, formally concluding quantitative tightening.

September Summary if Economic Projections:

On Wednesday, small tweaks to those sentences will be the tells. Any upgrade of growth language, or softer reference to employment risks, would skew hawkish. Acknowledgment that inflation pressures are easing again, or a stronger emphasis on labor-market deterioration, would nudge the message in the other direction. Markets will also want clarity on the stance of the balance sheet now that QT is over—does the Fed see its current holdings as roughly stable, or is a distant discussion of reinvestment and eventual balance-sheet expansion back on the table?

Layered on top of the macro debate is a Fed that is more openly divided than at any point in Powell’s tenure. At the last meeting, Stephen Miran dissented in favor of a larger 50 bp cut, while Kansas City Fed President Jeffrey Schmid preferred no cut at all. That two-sided dissent underscored the Committee’s split between a dovish camp focused on labor-market risk, a hawkish camp worried about sticky inflation and financial stability, and a shrinking center trying to move in 25 bp increments. This week, with several regional presidents openly questioning the need for another cut, the dissent count could rise further. Three or more “no” votes—or another push for a larger cut from Miran—would signal a Fed that is losing its internal consensus just as Powell’s term winds down.

And this is where the politics intrude. Powell is increasingly viewed as a lame-duck chair, with markets already gaming out a potential transition to a Trump-appointed successor. Kevin Hassett is widely seen as a leading candidate, and while it’s unlikely, there has even been speculation that Trump could try to upstage the press conference by announcing Powell’s replacement while the chair is still at the podium. That headline probably never hits—but the fact that traders even discuss the scenario tells you how much the succession risk is in the air.

CME Fed Fund Futures- December 2026 Outlook:

Hassett’s perceived fingerprints on the recent steepening of the curve only heighten the stakes. Some in the market blame his policy proposals and rhetoric for pushing up term premia and helping drive long-end yields higher. That makes this meeting doubly sensitive: Powell is trying to guide expectations for the 2026 path at the same time investors are starting to discount the possibility that a more dovish, politically aligned chair could be steering the Committee before those projections ever play out. If markets conclude that the incoming regime will lean harder on cuts and tolerate higher inflation, long yields may stay elevated even as the Fed trims at the front end—exactly the opposite of what a textbook easing cycle is supposed to deliver.

For markets, the combination—a likely cut, a dot plot still pointing to a very gradual path, a fractured Committee, and a chair whose influence may be fading—tilts expectations toward a hawkish outcome. The base case is a “last good cut” message: rates come down 25 bp, but the statement and SEP imply a long pause, with any future reductions tightly conditioned on clearer evidence of weak growth or disinflation. That would support the dollar, pressure long yields, and keep equities choppy into year-end.

The upside surprise, oddly, is that Powell sounds less hawkish than feared and leans into the rising risks to employment, the data gaps, and the possibility of another move as soon as January. In a year where every twist in Fed communication has whipsawed risk assets, traders will be listening less to the 25 bp move itself and more to whether Wednesday feels like the end of Powell’s easing cycle—or just the last chapter before someone else starts writing the script.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet