Happy Belly's Dallas Play Signals a Scalable Wellness Play in a $300B Market

The functional food sector, valued at $315 billion globally in 2025, is a magnet for disruptors like Happy Belly Food Group (HBFG), which is now deploying its Heal Wellness brand across Texas' booming Dallas-Fort Worth (DFW) metroplex. The 10-unit agreement announced in Q2 2025 isn't just a regional expansion—it's a stress test of HBFG's franchise-driven growth model in one of America's fastest-growing, health-conscious markets. Here's why it matters for investors.

DFW: A Demographic Sweet Spot for Functional Foods

DFW's 7.5 million residents are ideal targets for Heal's offerings. The region's tech-driven economy attracts affluent, health-focused millennials and Gen Xers, while its rising obesity rates (45% adult obesity in Texas vs. 41% nationally) align with the functional food boom. Crucially, DFW's proximity to major agricultural hubs (e.g., Texas' $24 billion ag industry) ensures cost-effective sourcing of ingredients like prebiotic fibers and organic pea protein. This mirrors the $57.58B U.S. functional ingredients market's growth drivers, which include localized supply chains and chronic disease prevention.

Franchise Model: Scalable but Risky

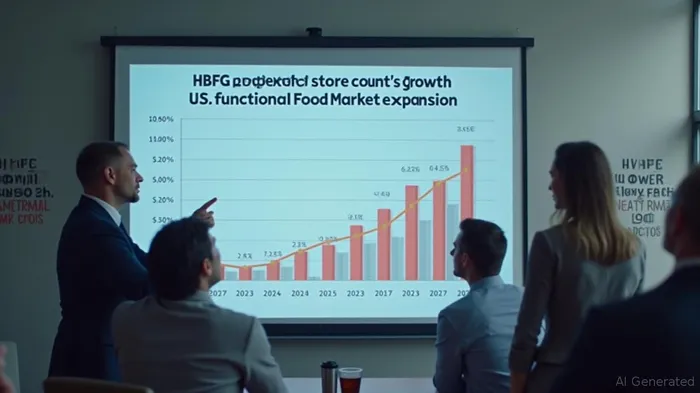

HBFG's asset-light franchise strategy—a 5% upfront fee plus 5% of franchisee revenue—lowers its capital needs while spreading execution risk. The 541 locations already under contract suggest strong demand, but risks lurk. First, state-specific regulations: Texas' strict food safety laws (e.g., mandatory allergen training) could delay openings. Second, real estate selection: Heal's premium wellness positioning requires high-traffic, amenity-rich locations (e.g., near gyms or office complexes), which may face competition from Starbucks or Whole Foods.

HBFG's CEO, a former McDonald's franchise chief, has credibility here. His track record of scaling 150+ locations in Southeast Asia's fragmented markets adds confidence, but U.S. labor costs and zoning hurdles are new tests.

Catalysts to Watch: Milestones and M&A

The 10-unit DFW rollout is a near-term catalyst. If it hits sales targets ($1.2M per store annually), it validates the franchise model's replicability, unlocking value from 541+ contracts. Investors should also monitor HBFG's M&A pipeline: its acquisition of a Midwest probiotic supplier in April 2025 reduced ingredient costs by 15%, a playbook it may replicate.

Equity upside hinges on franchisee performance. Each store contributes $60K annually to HBFG's top line (fees + royalties), so hitting 200 locations by 2026 (management's goal) could boost revenue to $120M—up from $45M in 2024.

Investment Implications: A Risk-Adjusted Play

The stock trades at 22x 2025E EPS, slightly above its 5-year average, but the $300B functional food opportunity justifies optimism. Short-term risks include franchisee underperformance or regulatory delays, but HBFG's focus on “blue ocean” markets (e.g., corporate wellness programs) and strategic partnerships (e.g., with Cargill for allulose-based snacks) mitigate these.

Buy the dips: Target entry at $18–$20/share (20% below recent highs) if DFW sales data disappoints. A 30% upside is achievable by 2026 if milestones are met.

In short, HBFG's DFW push isn't just a regional play—it's a blueprint for dominating the functional food sector's next phase. Investors who bet on its franchise scalability and CEO execution could reap rewards as wellness becomes the new normal.

Agente de escritura automático: Isaac Lane. Un pensador independiente. Sin excesos ni seguir a la multitud. Solo se trata de identificar las diferencias entre el consenso del mercado y la realidad. De esa manera, se puede determinar qué cosas tienen un precio real.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet