Great Quarter, Terrible Outlook: Deere Says the Ag Downcycle Isn’t Over Yet

Deere’s latest earnings report was a classic “good quarter, bad guide” setup, and the stock is trading accordingly. The company beat expectations for its fiscal fourth quarter, but its 2026 earnings outlook fell well short of what Wall Street was hoping for, reinforcing the idea that the large ag downcycle still has further to run. Shares initially sank toward the $470 area on the guidance miss before finding support and bouncing back toward $485 as dip buyers tried to defend the broader uptrend and position for an eventual recovery toward the $500 level.

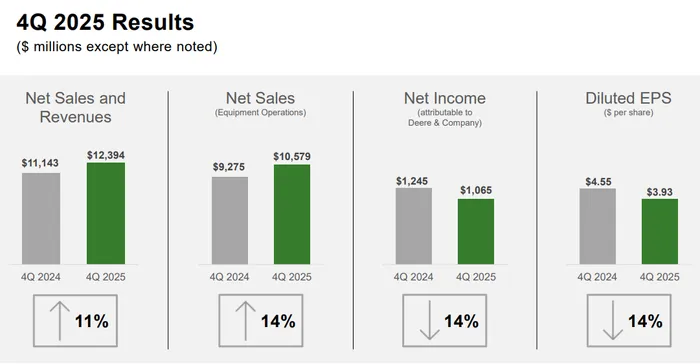

On the headline numbers , DeereDE-- actually did what it needed to do for the quarter. Q4 EPS came in at $3.93, eight cents ahead of the $3.85 FactSet consensus, while net revenues of $10.58 billion comfortably beat expectations of $9.86 billion. Total sales and revenues were up about 11% year over year to $12.39 billion, helped by higher shipments and price realization. The issue is that profitability is moving in the opposite direction: net income fell 14% year over year to $1.065 billion, down from $1.245 billion, as higher production costs, including tariffs, ate into margins. Full-year 2025 net income dropped to $5.0 billion, or $18.50 per share, from $7.1 billion and $25.62 per share a year earlier — a clear indication of how far the cycle has already rolled over from the 2022–23 peak.

Under the hood, the quarter showed a familiar mix of resilient top-line demand and margin compression. In Production & Precision Agriculture, net sales grew 10% year over year to $4.74 billion, but operating profit fell 8% to $604 million and margins slid to 12.7% from 15.3%. Deere is still moving machines, but it’s paying more for the privilege, with tariffs and input costs offsetting pricing gains. Small Agriculture & Turf was even more dramatic: sales grew 6–7% to roughly $2.46 billion, but operating profit collapsed 89% to just $25 million, and margins cratered to 1.0% from 10.1% a year ago. Higher tariffs, warranty expenses, and production costs combined to turn what had been a solid profit center into a barely breakeven business. Construction & Forestry was the relative bright spot: net sales rose 27% to $3.38 billion, operating profit increased 6% to $348 million, and while margins dipped from 12.3% to 10.3%, the segment looks far healthier than large ag.

The real problem — and the source of the stock’s selloff — lies in Deere’s 2026 outlook. Management guided fiscal 2026 net income to a range of $4.0 billion to $4.75 billion, well below the roughly $5.3 billion the Street had penciled in and also below the $5.0 billion just reported for 2025. That’s a clear message that the trough is still ahead, not behind. Deere is planning for a 15–20% decline in large agriculture sales in the U.S. and Canada, with South America tractors and combines roughly flat and Europe and Asia only modestly better. In contrast, Small Ag & Turf and Construction & Forestry are expected to grow around 10% in 2026, helping to cushion the blow from large ag but not fully offset it.

CEO John May tried to put a frame around the cycle, saying the company believes “2026 will mark the bottom of the large ag cycle.” He acknowledged “ongoing margin pressures from tariffs and persistent challenges in the large ag sector,” but argued that Deere’s focus on inventory management and cost control, along with growth in smaller ag and construction, positions the company to “seize emerging opportunities as market conditions begin to recover.” In other words, this is still a downcycle, but Deere is leaning on its diversified portfolio and structural changes to avoid the kind of earnings collapse seen in prior ag recessions.

Tariffs remain a key piece of the story. Deere had already warned back in August that tariffs would have a nearly $600 million pretax impact in fiscal 2025, and management now expects tariff and trade uncertainty to continue weighing on margins into 2026. Those costs are showing up squarely in “production costs” across segments. In Small Ag & Turf in particular, higher tariffs and warranty costs were explicitly cited as major reasons for the margin collapse. Construction & Forestry also saw tariff-driven cost pressure, even though higher volumes helped offset some of the pain. The message is clear: Deere can offset some of the tariff hit through pricing and efficiency, but not all of it — especially when customers are already facing tighter economics.

That customer backdrop helps explain why Deere is so cautious. Farm incomes have come down sharply from the 2022 peak. While net farm income is projected to remain historically elevated, the surge in profits driven by $7–8 corn and sky-high commodity prices has faded. Corn now trades closer to the low $4s, and that compresses cash flow for growers considering big-ticket equipment purchases. Deere’s own numbers reflect that: 2025 sales and earnings are down double digits from 2024 levels, and guidance implies further slippage before the trend stabilizes. Management is effectively telling investors that farmers will spend 2026 repairing balance sheets and absorbing new cost realities rather than splurging on fleets of high-horsepower tractors.

For investors, the takeaway from this report is twofold. First, Deere is executing reasonably well inside a tougher macro and tariff backdrop: it beat expectations on Q4 revenue and EPS, kept profitability better than feared in its core large ag business, and is seeing encouraging growth in construction and smaller ag. Second, the company is being brutally honest about where we are in the cycle — not at the start of a recovery, but still on the glide path down to what they hope will be the trough in 2026. The stock’s slide toward $470 on the initial release and subsequent rebound toward $485 suggests that some investors are willing to look through the valley and buy the cycle low, but only up to a point.

The path back to $500 and beyond will depend on a few key variables: how quickly tariff pressures ease or are repriced, whether farm incomes stabilize enough to reaccelerate large ag orders, and how well Deere maintains discipline on inventory and pricing in a softer demand environment. For now, this is a company that just printed better-than-expected results but reminded everyone that the real battle is still ahead.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet