Graphs Worth 1000 Words: What Are the Impacts of Trump's Tariffs?

Former President Donald Trump is once again wielding tariffs as a policy tool, but this time, it may backfire. A recent New York Fed survey revealed that businesses expect cost increases in 2025 to surpass those of the previous year. This will likely add further pressure to domestic inflation.

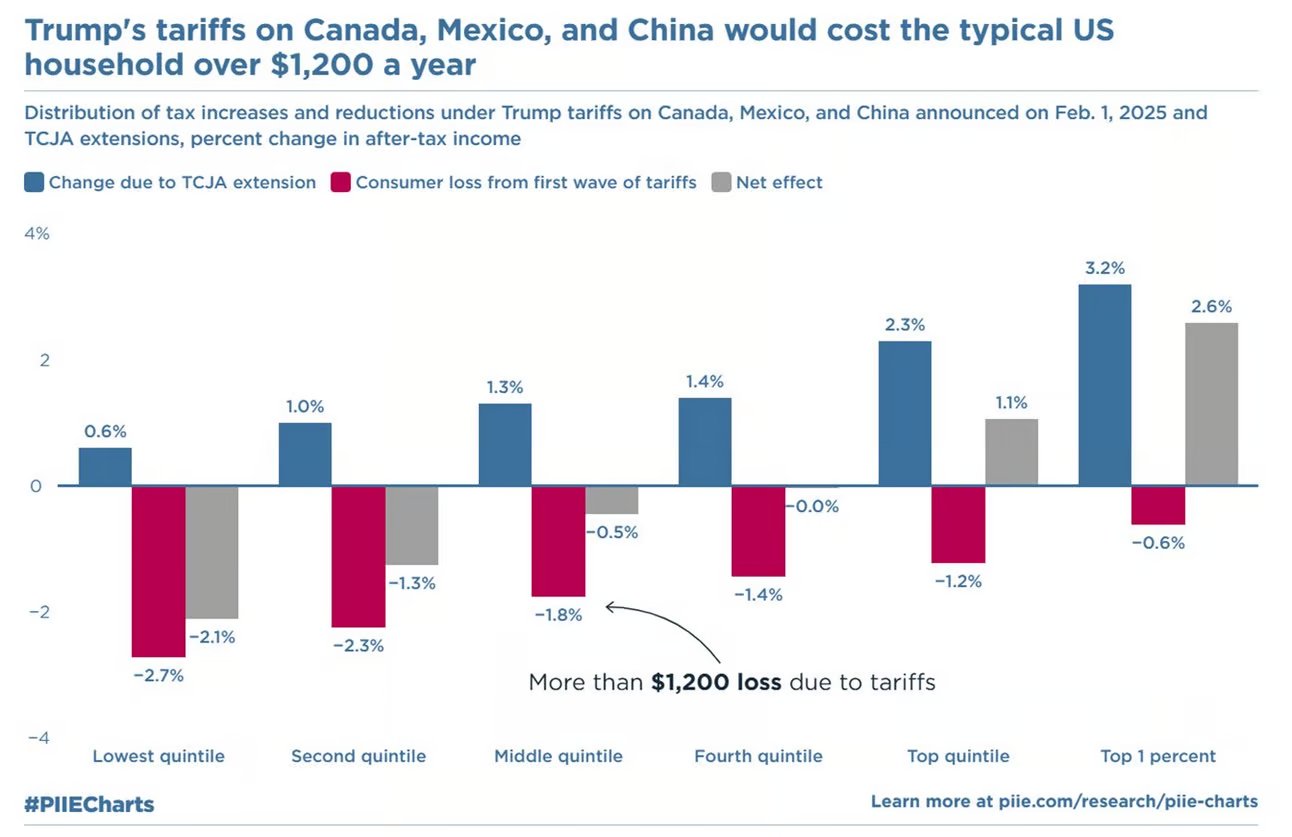

Additionally, research shows that Trump's tariff policies could cost the average American middle-class household an extra $1,200 annually. Lower-income groups would bear a disproportionately higher burden, while wealthier Americans would actually benefit from the extension of Trump's tax cuts. In fact, all Americans—except for the richest 20%—will pay more in tariffs than they will receive from Trump's tax reductions.

Which Industries Will Be Affected?

Which Industries Will Be Affected?

As shown in the following chart, if Trump imposes a 25% tariff on Canada, U.S. energy prices will spike significantly—energy being a key driver of inflation.

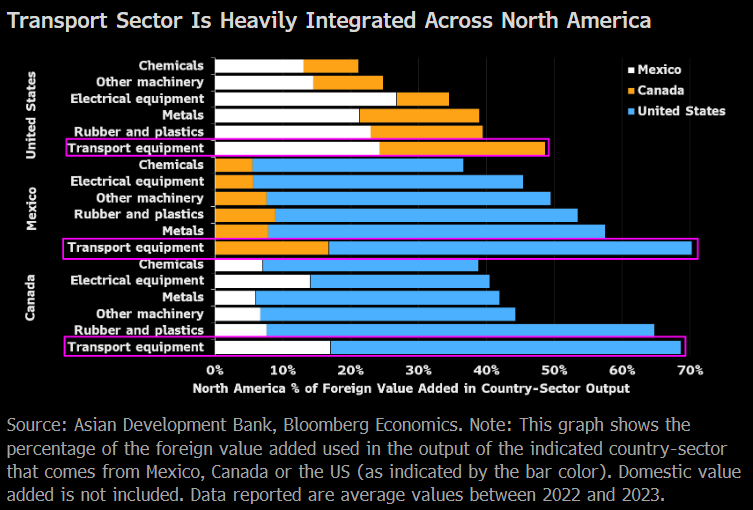

The North American automotive industry is another major concern, as supply chains across the U.S., Canada, and Mexico are deeply intertwined. Over 80% of critical auto components imported by U.S. manufacturers come from Canada and Mexico. Imposing tariffs on these goods would, in effect, be a tax on American businesses and consumers.

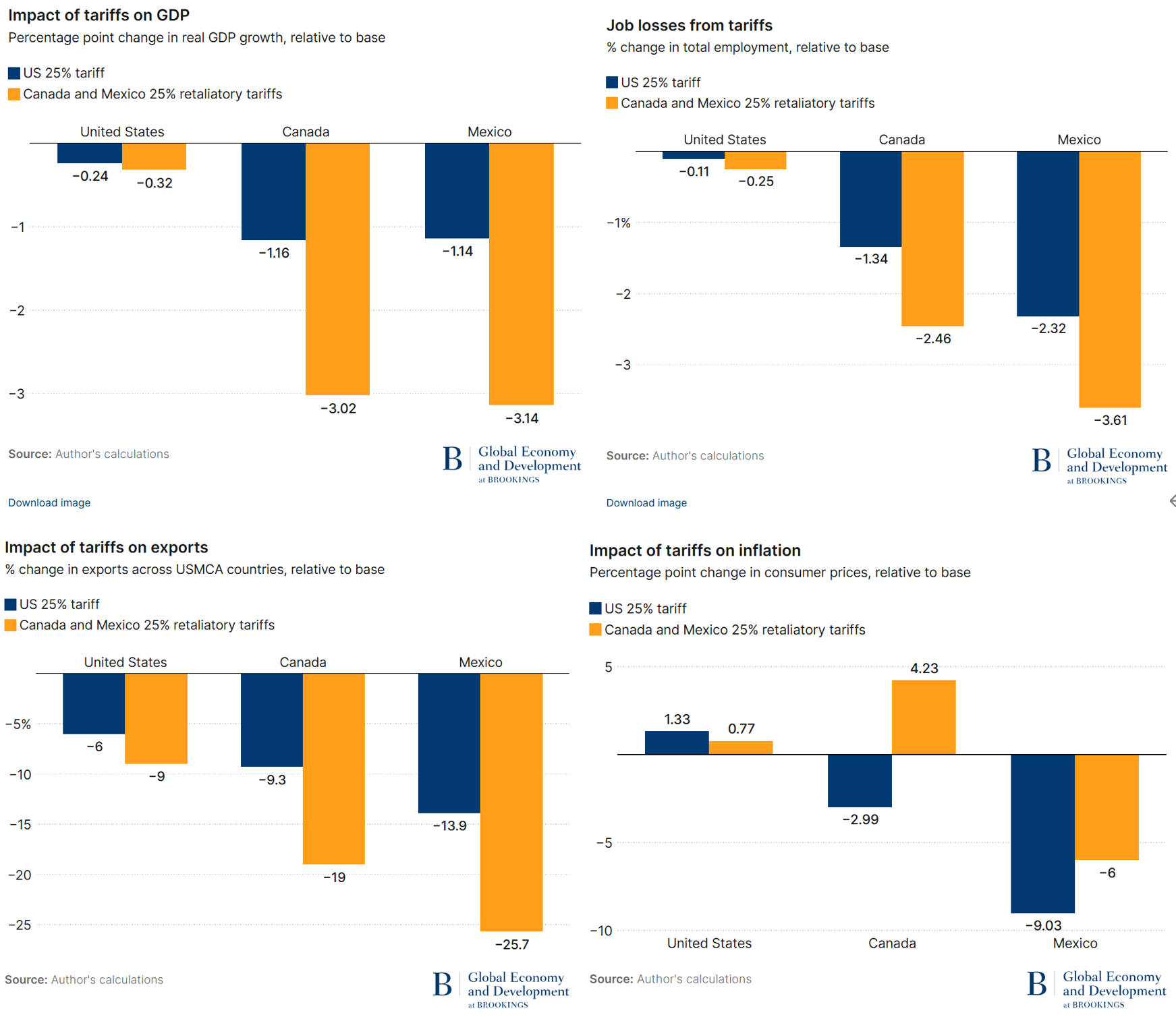

Economic Impact of a 25% Tariff on Canada & Mexico

GDP: A 0.25 percentage point decline in U.S. GDP; if Canada and Mexico retaliate, the decline could exceed 0.3 percentage points.

Employment: A 0.11% reduction in U.S. jobs; with retaliation, job losses could rise to 0.25%.

Inflation: U.S. inflation could increase by more than 1.3 percentage points; however, if Canada and Mexico retaliate, inflation might rise by a lesser 0.77 percentage points due to reduced exports.

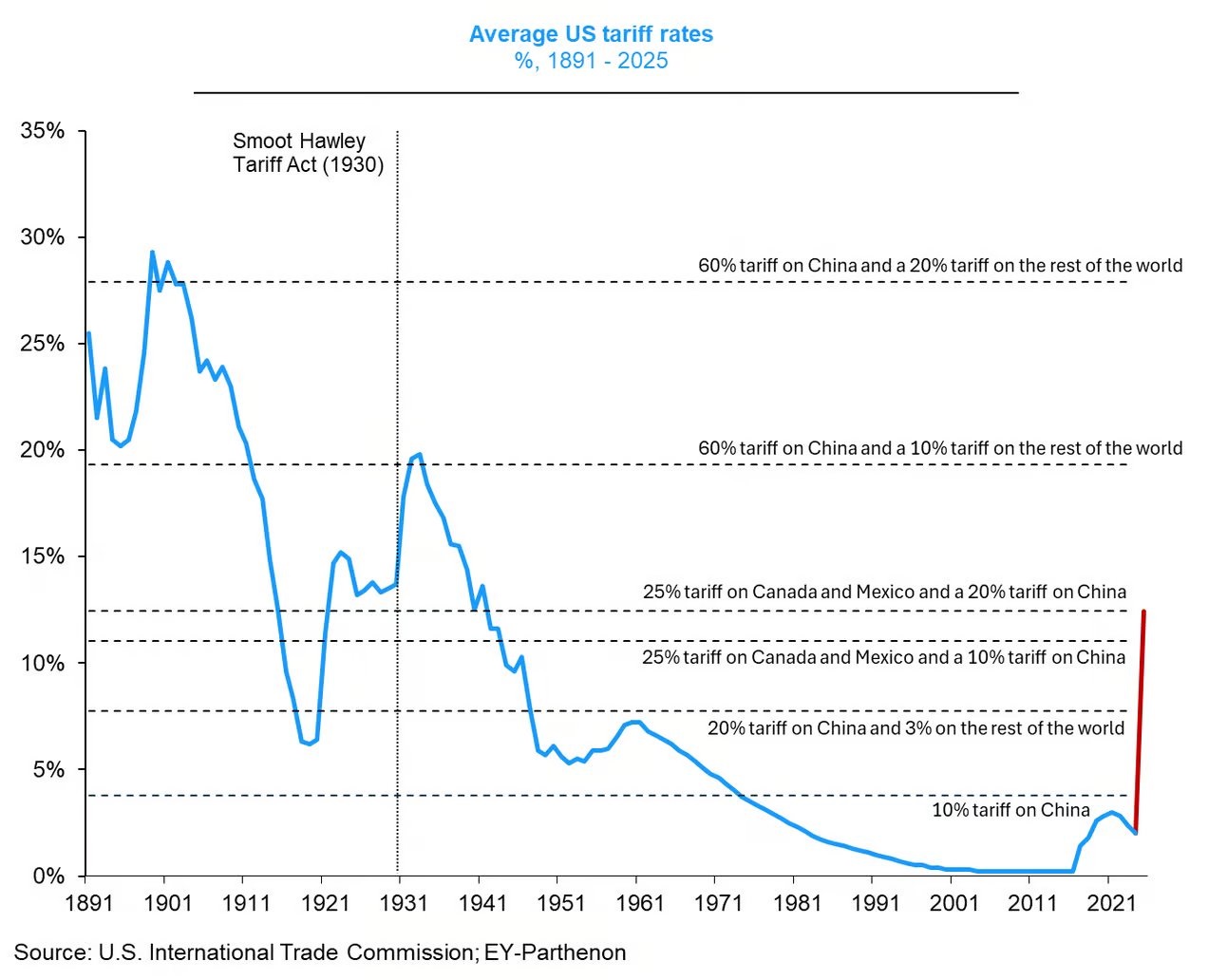

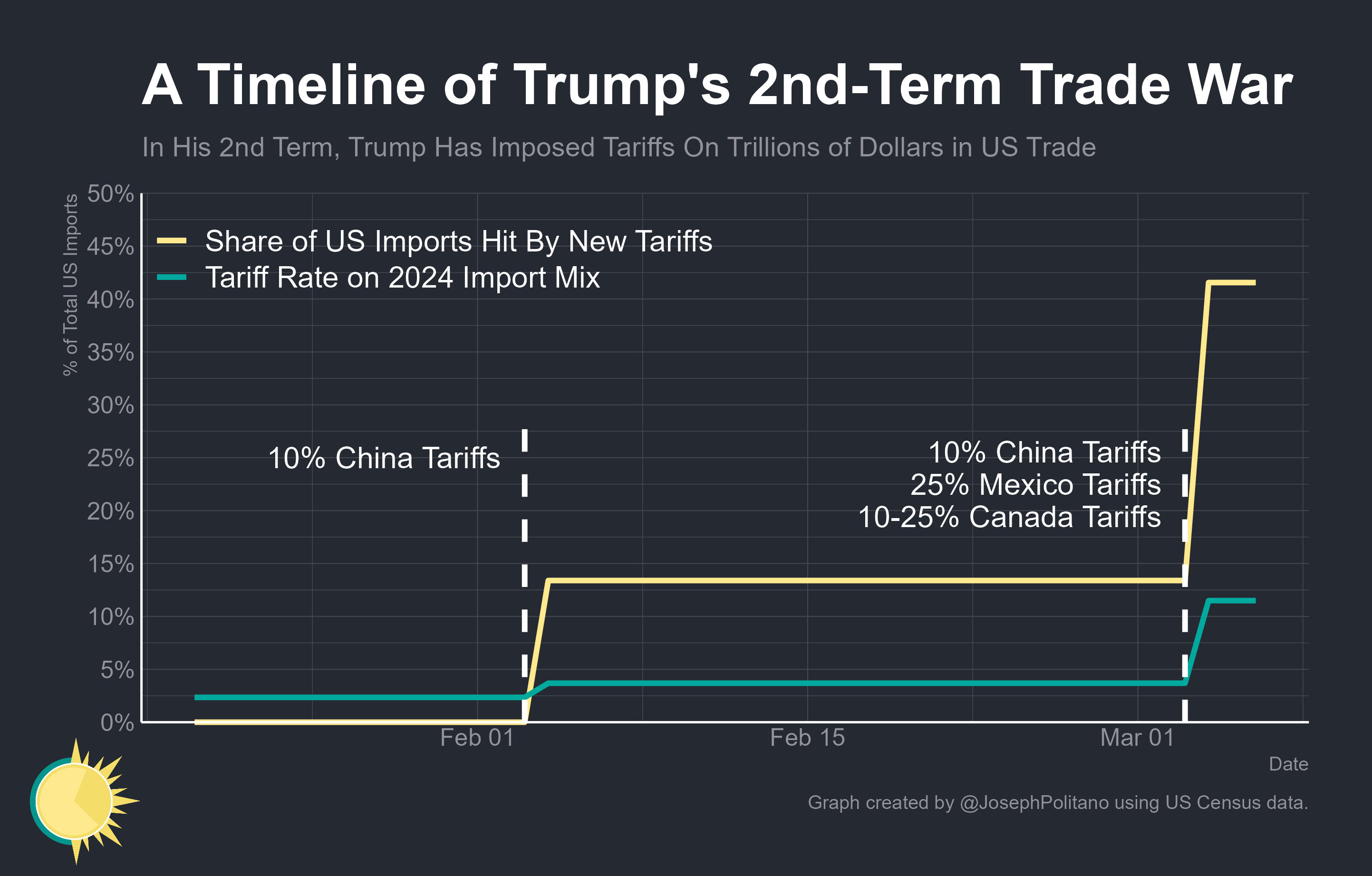

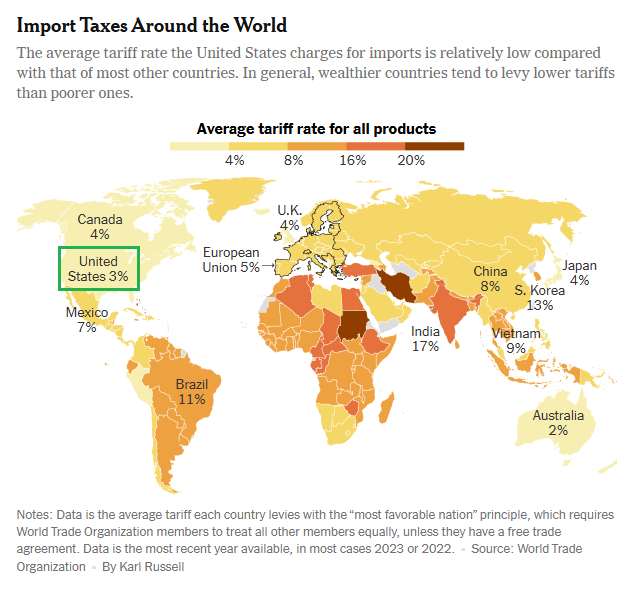

Where Do U.S. Tariffs Stand Today?

Where Do U.S. Tariffs Stand Today?

Under Trump's aggressive tariff strategy, 42% of total U.S. imports are now subject to tariffs—the highest level since World War II.

To put things into perspective, the current U.S. average tariff rate is just 3%—one of the lowest among developed economies. A sharp escalation in tariffs would mark a dramatic shift in trade policy.

Market Reaction: Investors on Edge

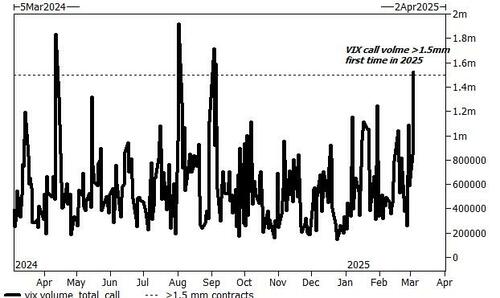

The uncertainty surrounding Trump's tariff policies has left U.S. stock market investors uneasy. The S&P 500 has posted negative returns this year, significantly underperforming both Chinese and European markets. Goldman SachsGBXC-- notes that Tuesday saw the highest volume of VIX call options purchased in a single session since last September—suggesting that traders are hedging against heightened volatility.

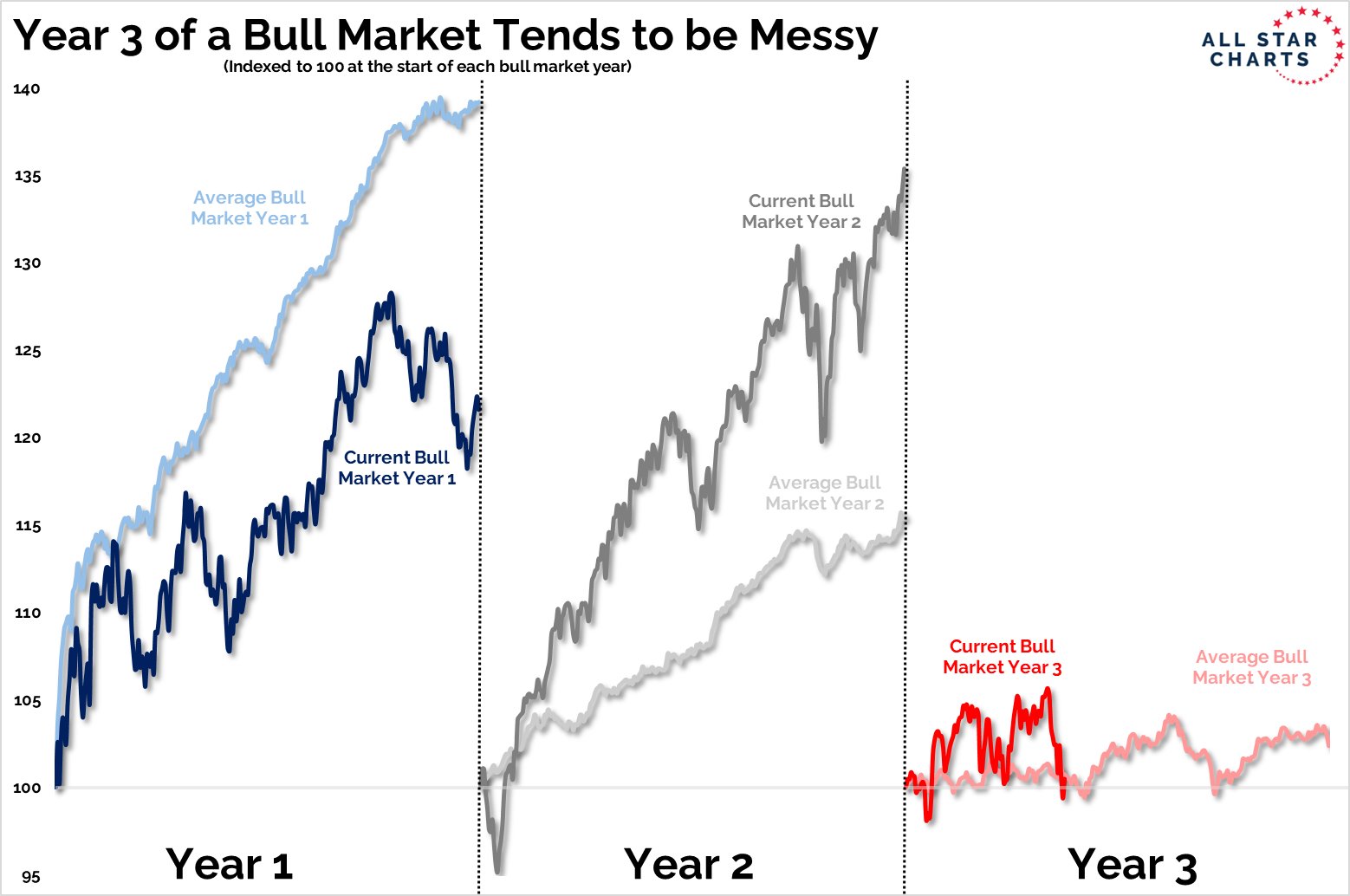

Interestingly, this year's U.S. market trajectory closely mirrors 2019, during the height of the U.S.-China trade war.

Another notable trend: historically, the third year of a bull market tends to yield lackluster returns. Since the bear market of 2022, the current bull cycle began in 2023—making 2025 its third year.

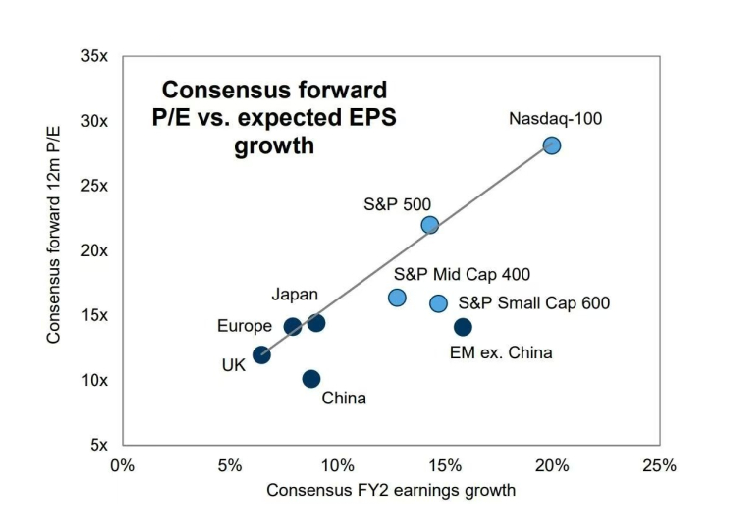

While historical patterns can be intriguing, fundamental analysis remains key. Goldman Sachs' valuation model suggests that U.S. stock valuations are fair, whereas emerging markets—excluding China—appear significantly undervalued.

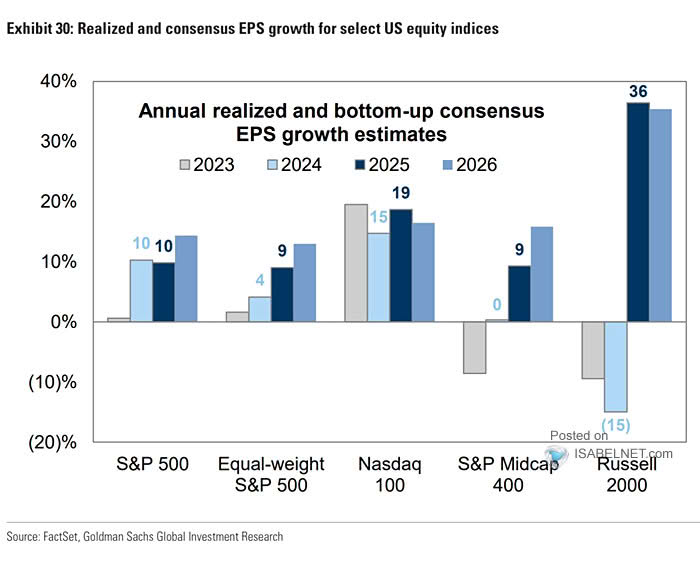

Earnings Outlook: Small-Cap Stocks Lead the Way

Despite macroeconomic concerns, analysts expect robust earnings growth for U.S. companies in 2025:

Small-cap stocks: Projected EPS growth of 36%, the highest among all asset classes.

S&P 500: Earnings expected to rise by 10%, supporting a continued bull market.

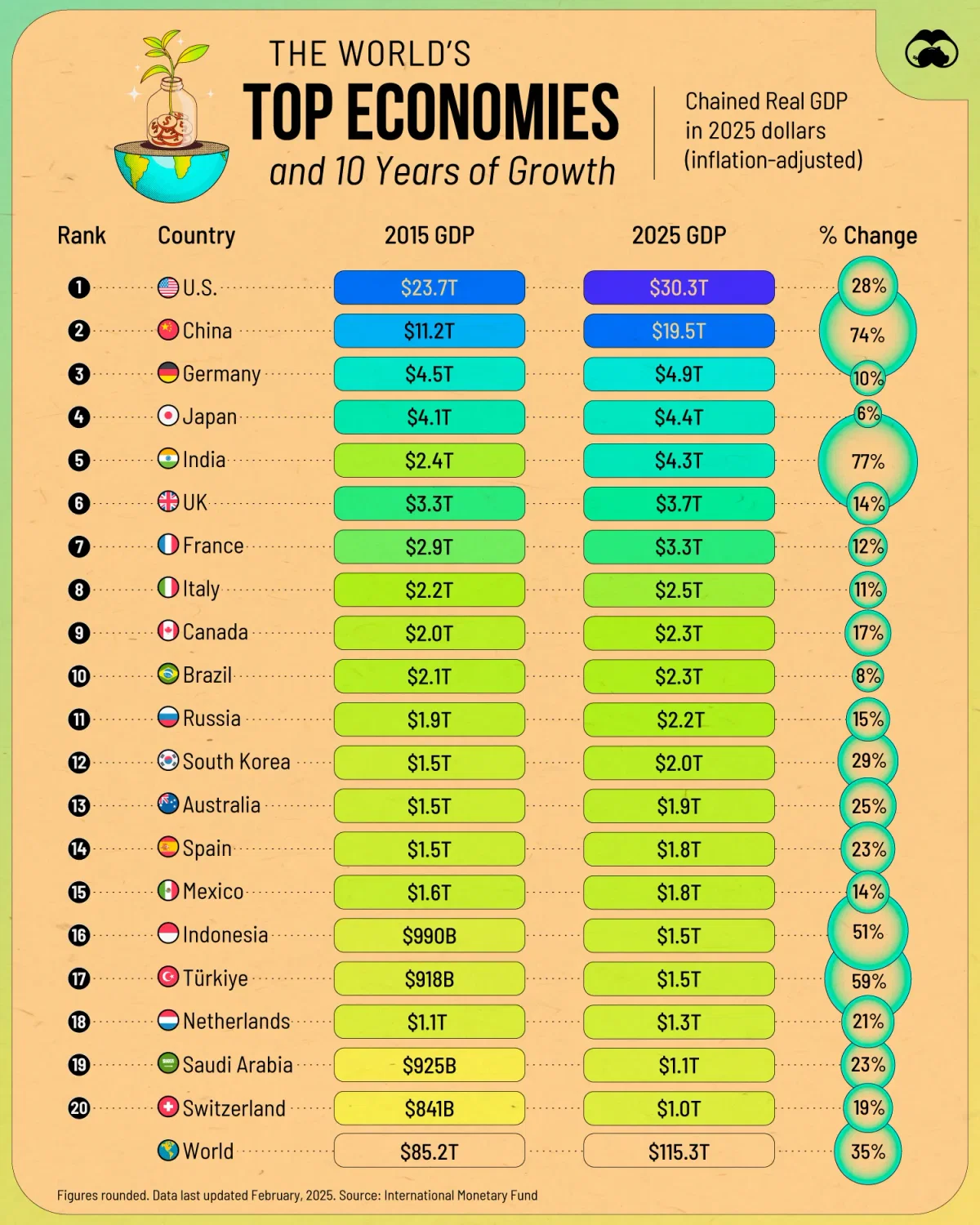

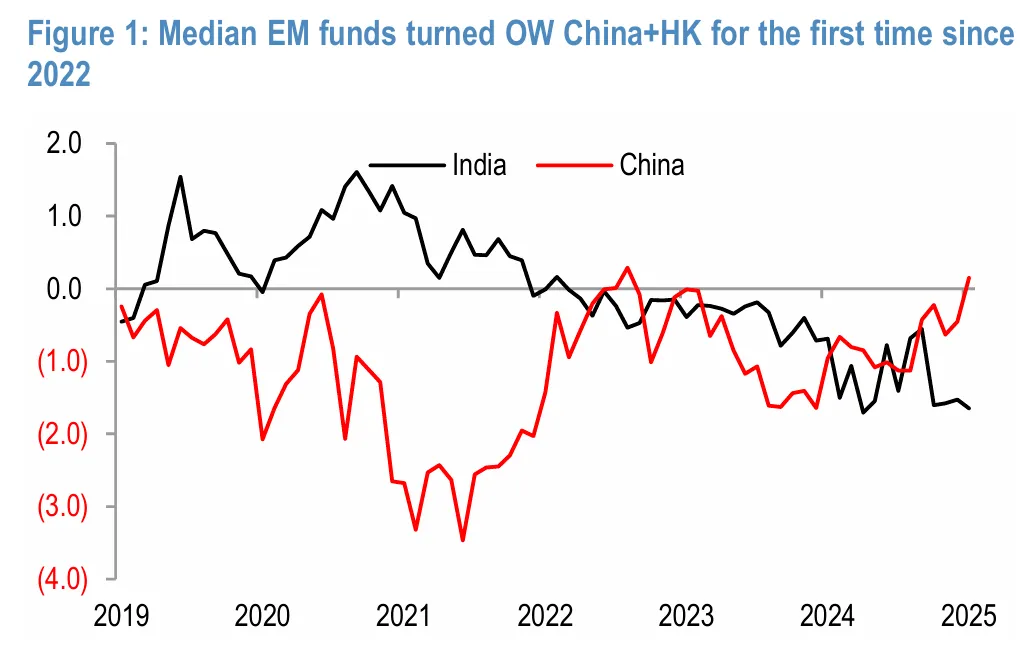

China's Economic Performance: A Decade of Outperformance

Shifting the focus to China, Chinese assets have recently rallied, though they have lagged behind global markets over the long term. However, when measured by GDP growth, China remains the global leader over the past decade.

Between 2015 and 2025, China's inflation-adjusted GDP is set to increase from $11.2 trillion to $19.5 trillion, an expansion of $8.3 trillion—outpacing even the U.S., which is expected to grow by $6.6 trillion over the same period.

In percentage terms, China's GDP is projected to rise 74% over ten years, the highest among major economies, second only to India's 77% growth. However, given China's much larger economic base, maintaining such high growth rates is particularly impressive.

Reflecting this optimism, global investors have been increasing their exposure to Chinese markets. Goldman Sachs reports that emerging market funds have, for the first time since 2022, begun overweighting Chinese assets, surpassing India in allocations.

Global Economic Developments: Japan & Gold Markets

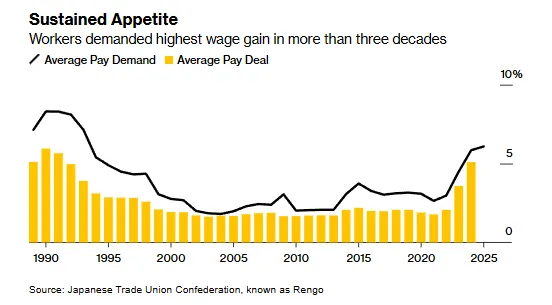

Japan: After decades of economic stagnation, Japan may finally be exiting its deflationary trap. The country's largest labor union is demanding a 6.09% wage increase, the highest since 1993

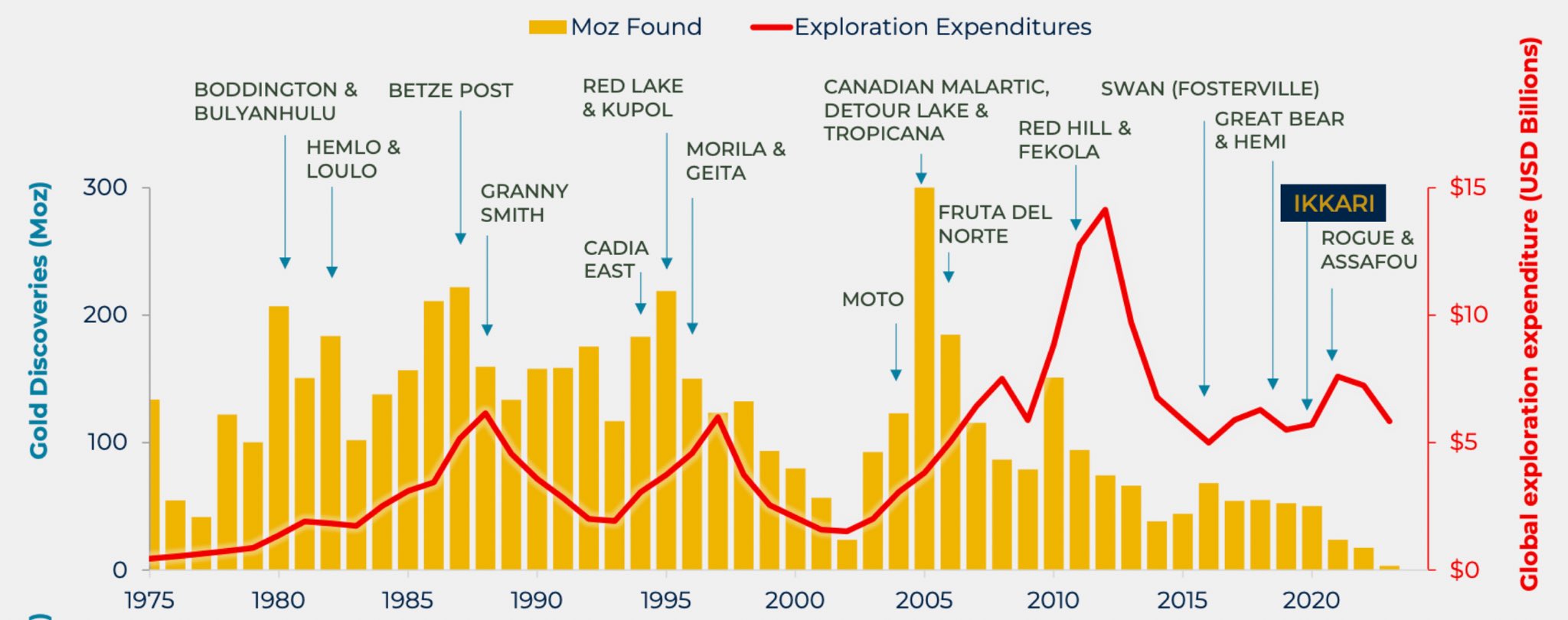

Gold Supply: Since 2005, the global discovery of new gold reserves has halved every five years, while demand for gold continues to surge. This supply squeeze could drive prices higher in the long term.

Expert analysis on U.S. markets and macro trends, delivering clear perspectives behind major market moves.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet