Google’s $185B AI Spending Shock: Blowout Quarter, Investor Panic

Alphabet delivered a decisive earnings beat in Q4 2025, but the market’s reaction made clear that fundamentals are no longer the only thing investors are pricing. While revenue, margins, and growth across Search and Cloud all came in stronger than expected, the real headline was management’s stunning 2026 capital expenditure outlook, which landed well above even the most aggressive buy-side estimates and immediately reignited concerns around free cash flow, capital returns, and balance-sheet strain.

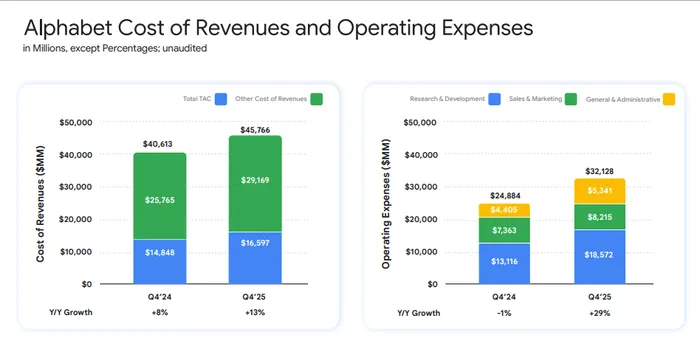

Starting with the numbers , Alphabet reported Q4 revenue of $113.8 billion, ahead of consensus estimates near $111.4 billion and up 18% year over year. Earnings per share came in at $2.82 versus expectations of $2.63, representing 31% growth. Operating margin held steady at roughly 32%, an impressive outcome given the scale of investment underway and a $2.1 billion stock-based compensation charge tied to Waymo. Net income rose 30% to $34.5 billion, reinforcing that Alphabet’s core businesses remain highly profitable even as spending accelerates.

Advertising remained a key pillar of strength. Total Google advertising revenue reached $82.3 billion, with Search and Other revenue growing 17% year over year to $63.1 billion. This growth reflects not just macro resilience, but also improving ad relevance driven by AI. Management highlighted meaningful reductions in irrelevant ads served, with Gemini models enhancing targeting and performance across direct-response formats. YouTube ads rose 9% year over year to $11.4 billion, with management noting that growth was partially constrained by lapping a strong U.S. election advertising cycle in the prior year. Importantly, YouTube’s combined ads and subscription revenue exceeded $60 billion for the full year, underscoring its evolution into a diversified media platform rather than a pure ad-cycle play.

Google Cloud was the standout growth engine. Cloud revenue surged 48% year over year to $17.7 billion, materially ahead of expectations near $16.2 billion and well above the widely cited growth bogey of 37%. The business exited 2025 with an annualized run rate above $70 billion, driven by accelerating demand for AI infrastructure, platform services, and enterprise AI solutions. Perhaps more important than revenue was the backlog: Cloud backlog increased 55% sequentially and more than doubled year over year to $240 billion, providing unusually strong visibility into future growth. Operating income in Cloud reached $5.3 billion, confirming that profitability is scaling alongside revenue—an issue that weighed on sentiment in earlier phases of the Cloud story.

AI engagement metrics reinforced the momentum narrative. Management disclosed that daily AI Mode queries per user have doubled since launch, while the Gemini app now exceeds 750 million monthly active users. Gemini Enterprise adoption has also ramped quickly, with more than 8 million paid seats sold in just four months. Just as notable, Alphabet disclosed that Gemini serving unit costs were reduced by 78% over 2025 through optimization and efficiency gains, helping counter investor fears that AI scale necessarily implies permanently lower margins.

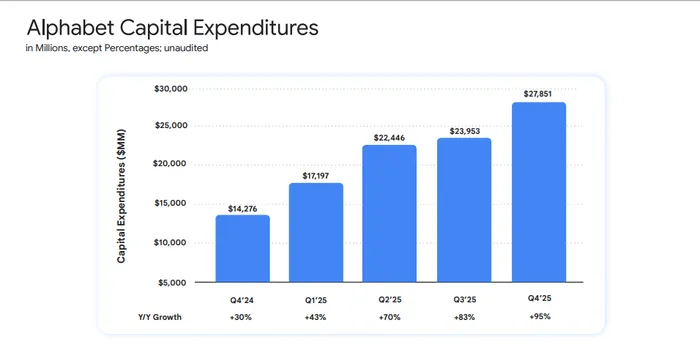

Against this backdrop of strong execution, the CapEx guidance was a shock. Alphabet guided to 2026 capital expenditures of $175 billion to $185 billion, compared with consensus expectations closer to $120 billion and up sharply from roughly $91 billion spent in 2025. Management framed the increase as a direct response to sustained AI and Cloud demand, ongoing supply constraints, and the need to invest ahead of revenue to maintain leadership in AI infrastructure. CFO Anat Ashkenazi emphasized that depreciation expense will meaningfully increase in 2026, particularly as data center and energy costs ramp, a clear signal that near-term margin pressure is likely.

On funding, management did not explicitly announce changes to capital return policy, but the implications were hard to miss. Alphabet ended the quarter with $126.8 billion in cash and marketable securities and generated $164.7 billion in operating cash flow over the past twelve months. Free cash flow for 2025 totaled $73.3 billion, already reduced by elevated CapEx. Alphabet also issued $24.8 billion in senior unsecured notes in late 2025, suggesting that debt issuance is already part of the funding mix. While management stressed efficiency initiatives and long-term planning, investor speculation quickly turned to whether share repurchases may slow or whether debt issuance will scale further to support infrastructure build-out.

The market’s initial reaction reflected this tension. Despite the earnings beat, shares fell sharply post-report as investors recalibrated valuation frameworks to account for higher capital intensity and lower near-term free cash flow. However, the scale of spending also created immediate winners across the AI and data center supply chain. Broadcom rallied as investors priced in sustained demand for custom AI accelerators and TPUs. Lumentum benefited from expectations for increased spending on high-speed optical interconnects, while Celestica gained on its role as a key manufacturing partner for Google’s data center hardware. Other beneficiaries include Vertiv, Amphenol, Nvidia, and TTM Technologies, all leveraged to sustained hyperscale infrastructure investment.

In sum, Alphabet’s quarter was operationally excellent and strategically aggressive. Core advertising remains durable, Cloud growth is accelerating well beyond expectations, and AI engagement metrics continue to scale rapidly. The market’s discomfort is not about demand, relevance, or competitive positioning—it is about the sheer magnitude of capital required to win the next phase of AI. Alphabet is clearly choosing to spend now, accept near-term financial noise, and defend its platform advantage. For investors, the debate is no longer whether Alphabet is executing, but whether the market is willing to tolerate a structurally more capital-intensive version of one of tech’s most profitable franchises.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet