Google’s $100 Billion AI Bet Gets Put to the Test: Can Alphabet Prove It’s Still the King of Search on Earnings Day?

Alphabet’s upcoming third-quarter earnings report Wednesday afternoon will test whether the company’s powerful recovery in digital advertising and early wins in artificial intelligence can sustain momentum into 2026. Shares of Google parent Alphabet (GOOGL) have surged to record highs, up roughly 70% over the past six months, as investors reprice its competitive position in AI-driven search and cloud infrastructure. Recent product launches — including the Gemini 3 model, the “agentic” Chrome browser, and deepening AI integrations across Search, YouTube, and Cloud — have positioned the company as a leading AI platform with unmatched scale. Yet with escalating capital expenditures, regulatory scrutiny, and intensifying rivalry from OpenAI’s new ChatGPT Atlas browser, the quarter represents an important checkpoint for investor confidence in Google’s AI monetization path.

Analysts expect AlphabetGOOGL-- to report third-quarter revenue of about $99.9 billion, up 13% year-over-year, and adjusted EPS of $2.26, compared with $2.31 last quarter. The Street sees operating margin near 35% and continued double-digit growth in Search, YouTube, and Cloud. BofA estimates search ad growth at 12% year-over-year, with YouTube again delivering a high-single-digit gain and GoogleGOOGL-- Cloud revenue advancing roughly 30%. Importantly, Alphabet’s CapEx trajectory remains under the microscope: the company lifted its 2025 CapEx outlook to $85 billion last quarter (from $75 billion previously), with Citi now projecting $111 billion for 2026 as Google ramps data center expansion and custom AI chip production. These figures matter not only for Google’s earnings power but also as a signal for hyperscaler peers — Amazon and Microsoft — that the next leg of AI infrastructure buildout remains robust.

Wall Street sentiment heading into earnings is overwhelmingly constructive. Analysts from KeyBanc, BofA, Citi, and HSBC all raised price targets in recent weeks — several now above $280 — citing strong advertiser trends, rising AI product engagement, and a favorable outcome from the Department of Justice antitrust remedies decision. That ruling, which requires Google to share some search data with qualified competitors but stopped short of forcing structural divestitures, was viewed as “better than feared,” clearing a key overhang for the stock. KeyBanc analysts said it acts as a “clearing event,” enabling investors to refocus on fundamentals: high-margin Search and accelerating Cloud growth. Still, Alphabet must now show that its AI strategy translates into durable monetization rather than just headline buzz.

For investors, the primary focus will again be the health of Google’s advertising ecosystem. Advertising remains Alphabet’s lifeblood — generating roughly 72% of revenue last quarter — and its trajectory is viewed as a real-time gauge of digital demand. Search revenue rose 12% in Q2 to $54.2 billion, powered by retail and financial services verticals, while YouTube ad revenue climbed 13% to $9.8 billion. Analysts expect similar growth rates this quarter, with particular attention on YouTube Shorts monetization and AI-driven ad targeting. Scotia noted that Shorts ad monetization is approaching parity with traditional long-form videos in several markets, a key milestone that could unlock further revenue expansion. Meanwhile, third-party data from ad agencies suggest Google’s ad budgets outperformed expectations in Q3, aided by a firm macro backdrop and rising advertiser experimentation with AI-assisted campaign creation.

Another critical piece of the puzzle is Google Cloud. The segment’s Q2 revenue of $13.6 billion (up 32% YoY) and margin improvement to 20.7% signaled operational maturity and reinforced the unit’s status as Alphabet’s second growth engine. Analysts see similar growth in Q3, with backlog expansion and continued customer adoption of AI-related services driving demand. Google Cloud now serves nine of the top ten AI labs globally and is benefiting from its in-house chip platform — the new 3nm Ironwood TPU — which narrows performance and cost gaps versus Nvidia’s GPUs. Citizens Financial projects that every 1GW of Google data center capacity could generate roughly $9 billion in incremental cloud revenue, and with $62 billion of PP&E listed as “assets not in service,” capacity expansion in 2026 could meaningfully lift Cloud’s trajectory.

Alphabet’s AI strategy will likely dominate the conference call discussion. Investors want clarity on Gemini 3’s rollout, AI Overview adoption (which now reaches over two billion users globally), and the degree to which AI features are expanding overall search queries versus cannibalizing paid clicks. CEO Sundar Pichai recently said AI is “expanding the search opportunity” by unlocking new informational queries and enabling richer ad formats. Analysts largely agree — Citizens noted that AI features are increasing total user engagement, which in turn boosts monetization potential. Yet competitive concerns remain: OpenAI’s new Atlas browser and Microsoft’s Copilot integration with Bing continue to raise questions about long-term search market share. HSBC argues Google still commands a 90% share of traditional browser-based queries and is “winning the in-browser AI battle,” but investors will want hard evidence in Wednesday’s metrics.

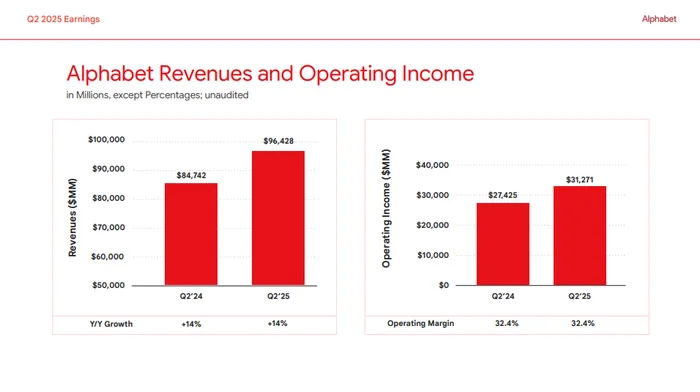

Last quarter’s financial performance provides a strong reference point. Q2 revenue rose 14% year-over-year to $96.4 billion, beating consensus by 2.6%, while net income increased 19% to $28.2 billion. Operating margin reached 32.4%, bolstered by double-digit growth across all major businesses. Free cash flow totaled $5.3 billion in the quarter and $66.7 billion over the trailing 12 months. Management guided for continued foreign exchange tailwinds and higher CapEx in Q3, emphasizing acceleration in data center construction and server deliveries to meet AI demand. Investors will compare this quarter’s numbers closely to Q2’s benchmark to gauge whether the company’s growth and margin expansion are sustainable in the face of rising infrastructure costs.

Beyond earnings, several external developments could color the near-term outlook. Google’s $9 billion investment commitment in South Carolina through 2027 underscores its continued domestic infrastructure buildout and signals confidence in long-term AI-driven demand. Partnerships like the revived Duane Arnold nuclear project with NextEra hint at a broader strategy to secure stable, sustainable power for its data centers. On the regulatory front, Alphabet continues to face scrutiny from both U.S. and European authorities, but the absence of a forced divestiture or major financial penalty in the DOJ case has soothed investors for now.

Heading into earnings, consensus expectations are high — but so is investor conviction that Alphabet’s AI evolution is beginning to pay off. Analysts forecast another quarter of resilient Search growth, accelerating Cloud adoption, and manageable expense pressure despite record CapEx levels. The key question is whether management’s commentary will justify the company’s premium valuation near 25x forward earnings. If Alphabet can demonstrate expanding AI monetization and reaffirm that its multi-billion-dollar infrastructure spend is translating into durable revenue leverage, Wednesday’s report could reinforce the narrative that Google remains the indispensable backbone of the AI economy.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet