Goldman Sachs Flags Unusual Market Calm Before The Election

On the eve of the U.S. election, the market is unusually calm, and hedge funds show a cautious wait-and-see attitude.

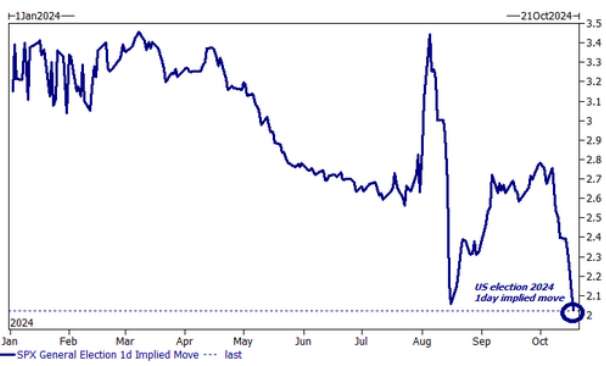

The policy positions of the two candidates are vastly different, and the market's calmness seems eerie. Goldman Sachs trader Brian Garrett pointed out last week that the implied volatility on Election Day is only 2%, the lowest reading since Goldman Sachs began tracking the indicator. He said, "This number might be a bit too low."

Last week, analysis pointed out that the significant drop in implied volatility may be due to a sharp decline in liquidity before the election day, a view later confirmed by Goldman Sachs.

Data from Goldman Sachs Prime shows that hedge funds' total leverage has decreased significantly as net leverage (a risk preference indicator measuring long and short positions) has dropped at the fastest pace since the banking crisis in March 2023.

At the same time, last week, the total leverage in the U.S. fundamentals hit the lowest level since March 2023, while the change in net leverage was relatively small. Goldman Sachs believes this indicates that net leverage is decreasing and some funds are being set aside before the U.S. election.

However, even in the face of a sharp decline, the U.S. stock market was still in a net buying state last week, with the number of long buying transactions nearly twice that of short selling, with a ratio of 1.9:1.

Despite the overall buying trend in the market, during a week filled with earnings releases from tech giants, TMT stocks saw the largest net selling in five weeks, driven mainly by short selling and a lesser degree of long selling. Software, entertainment, electronic devices, instruments and components, and interactive media and services were the sub-industries with the most net selling, while technology hardware and IT services were the sub-industries with the most net buying.

It is worth noting that for the fifth consecutive week, hedge funds have been unwinding recently established positions in the U.S. non-essential consumer goods sector, with long selling being twice as much as short covering. Household durables, hotels, restaurants and leisure, and textiles, apparel, and luxury goods were the sub-industries with the most net selling, while department store retailing and automobiles were the sub-industries with the most net buying.

In addition, data shows that from a liquidity perspective, long positions net sold about $10 billion worth of U.S. stocks (with about 50% of total sales in the technology sector). Prime Brokerage also commented that the equity sales department did not see a large-scale sell-off by hedge funds this week.

However, the analysis believes that selling before the election is understandable, but seasonal bullishness will start to take effect substantially:

"If volatility resets after the election and the Federal Reserve ends, then systematic strategies will generate huge demand, and stock buybacks will bring $6 billion in demand daily in November. Specifically, the stock sales department is optimistic about financial/value/transportation/industrial (short-term momentum themes), and PB data continues to show investor demand for cyclical stocks since early October."

Expert analysis on U.S. markets and macro trends, delivering clear perspectives behind major market moves.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet