Goldman or Citigroup: Which Transformation Story Is More Compelling?

Wall Street’s largest institutions are redefining what sustainable growth looks like. The Goldman Sachs Group, Inc. GS is evolving from a deal-driven powerhouse into a more balanced financial services firm, while Citigroup Inc. C is shedding complexity to sharpen its competitive edge.

As both banks pursue new strategic directions, investors are left with a critical question: which transformation narrative holds stronger long-term potential? Let us take a closer look and evaluate the potential of each bank.

The Case for GS

Goldman has been a dominant player in mergers and acquisitions, trading, and capital markets. Under CEO David Solomon, the company has embarked on a deliberate transformation to exit non-core consumer banking and double down on the divisions where GoldmanGS-- maintains a clear competitive advantage: investment banking (IB), trading, and asset and wealth management (AWM).

In sync with this, in January 2026, Goldman signed an agreement to transition the Apple Card program and associated accounts to JPMorgan. In December 2025, Goldman entered an agreement to acquire Innovator Capital Management. The deal significantly expands Goldman’s active ETF capabilities and is part of a broader pivot toward building “durable revenue streams” through diversified asset management and wealth-management offerings. In November 2025, Goldman reached an agreement with ING Bank Slaski to divest its Polish asset management firm, TFI. The deal is targeted for completion in the first half of 2026. In the third quarter of 2025, Goldman transitioned the General Motors credit card program. In 2024, Goldman completed the sale of GreenSky, its home improvement lending platform, to a consortium of investors.

The benefits of business restructuring are beginning to show in the numbers. In 2025, Goldman’s IB revenues rose 21% year over year. The company’s AWM division also posted a 11.9% increase in net revenues, reflecting growing fee income and strength in private credit. Goldman is targeting high-teens returns for the AWM division and roughly 5% annual growth in long-term fee-based net inflows over the medium term.

Goldman plans to ramp up its lending services to private equity and asset managers and expand internationally. The company's Asset Management unit intends to expand its private credit portfolio to $300 billion by 2029. After strengthening U.S. operations, the company will expand into Europe, the U.K. and Asia. In January 2026, GSGS-- acquired Industry Ventures to expand its exposure to the innovation economy and further solidify its position in the global alternatives market.

The Case for C

Citigroup’s transformation, by contrast, is far more sweeping. Under CEO Jane Fraser, the company is advancing its multi-year strategy to streamline operations and focus on its core businesses. Since announcing plans in April 2021 to exit consumer banking in 14 markets across Asia and EMEA, the company has completed exits in nine countries.

In sync with this, in February 2026, CitigroupC-- completed the sale of its Russian banking subsidiary, AO Citibank, to Renaissance Capital. The sale of AO Citibank strengthens Citigroup’s capital position and streamlines its balance sheet. The transaction is expected to provide an estimated benefit of $4 billion to C’s Common Equity Tier 1 capital in the first quarter of 2026.

The same month, C agreed to sell an aggregate 24% equity stake in Grupo Financiero Banamex, S.A. to several investors after completing the sale of a 25% equity stake in Banamex to Mexican businessman Fernando Chico Pardo at a fixed price-to-book multiple. The bank is also progressing with the wind-down of its Korean consumer banking operations, the exit from Russia, and preparations for an IPO of its Mexican consumer, small business and middle-market banking operations. These initiatives will free up capital and help the company pursue investments in wealth management operations in Singapore, Hong Kong, the UAE and London to stoke fee income growth.

Aligned with its goal of achieving leaner operations, Citigroup has overhauled its operating model and leadership structure, reduced bureaucracy and complexity while enhancing efficiency. In January 2024, the company announced plans to cut 20,000 jobs (about 8% of its global workforce) by 2026, having already lowered headcount by more than 10,000 employees.

Given such initiatives, the company expects revenues to see a compounded annual growth rate of 4-5% by 2026-end and will further drive $2-2.5 billion of annualized run rate savings. Further, management continues to target a return on tangible common equity of 10-11% in 2026.

In parallel, the company is deepening its presence in private markets and wealth management through partnerships that enhance revenue diversity and client engagement. In September 2025, Citigroup launched an $80-billion customized portfolio offering with BlackRock Inc., providing clients with tailored exposure across public and private markets. In June 2025, it partnered with Carlyle Group to expand asset-based private credit in fintech lending via the SPRINT platform. In September 2024, Citigroup and Apollo Global Management created a $25-billion private credit direct lending platform to meet rising corporate financing demand.

GS & C: Price Performance, Valuation & Other Comparisons

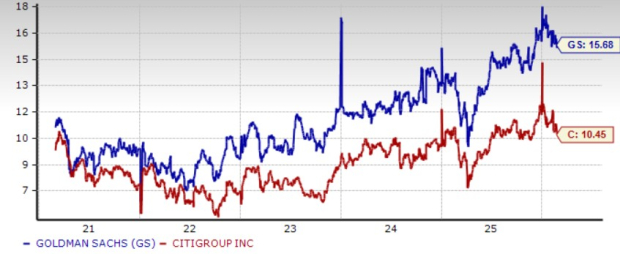

Over the past six months, shares of Goldman and Citigroup have risen 20.5% and 14.4%, respectively, compared with the industry’s growth of 3.2%.

Price Performance

Image Source: Zacks Investment Research

In terms of valuation, Goldman is currently trading at a 12-month forward price-to-earnings (P/E) of 15.68X. Meanwhile, Citigroup’s stock is trading at a 12-month forward P/E of 10.45X.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

C is trading at a discount compared with the industry average of 13.64X. However, the GS stock is trading at a premium.

C and GS reward their shareholders handsomely. In January 2026, GS raised its dividend 12.5% to $4.50 per share. It has raised its dividend six times over the past five years. Similarly, Goldman raised its dividend 33.3% to $4 per share in July 2025. It has raised its dividend three times over the past five years.

How Do Estimates Compare for GS & C?

The Zacks Consensus Estimate for GS’s 2026 and 2027 revenues reflects year-over-year rallies of 8.6% and 3.2%, respectively. Likewise, the consensus estimate for 2026 and 2027 earnings indicates increases of 10.3% and 10.7%, respectively. Over the past week, earnings estimates for both years have been revised upward.

Estimate Revision Trend

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for C’s 2026 and 2027 revenues suggests year-over-year increases of 5.4% and 4.3%, respectively. Also, the consensus estimate for 2026 and 2027 earnings indicates 27.9% and 18.4% growth, respectively. Over the past week, earnings estimates for both years have been revised upward.

Estimate Revision Trend

Image Source: Zacks Investment Research

GS or C: Which Stock Has Better Upside?

Goldman’s transformation is not just about shrinking risks, it is about reallocating capital toward structurally higher-return businesses. By reinforcing its dominance in advisory, trading and alternatives while scaling private credit and wealth management, GS is building a model that blends cyclical upside with recurring fee stability. That balance gives the company more operating leverage when capital markets rebound, while still providing resilience through asset and wealth management growth. The company’s push to expand its private credit portfolio and global alternatives platform positions it directly in line with long-term institutional demand trends.

By comparison, Citigroup is primarily in repair mode. Its restructuring is necessary and constructive, but much of the near-term story revolves around cost cuts, divestitures and capital redeployment rather than organic competitive expansion. While C’s discounted valuation and stronger near-term earnings growth projections may appeal to value-oriented investors, the path to sustained double-digit returns on equity remains execution-heavy and dependent on flawless operational streamlining.

Ultimately, Goldman offers a clearer growth narrative, backed by strengthening fundamentals, upward earnings revisions and a strategic focus on high-margin, scalable businesses. Its premium valuation reflects higher-quality earnings and stronger return potential. For investors seeking a combination of earnings durability, strategic clarity and long-term upside, GS emerges as the more compelling transformation story and the stronger stock to own for now.

At present, GS carries a Zacks Rank of 2 (Buy), while C has a Zacks Rank of 3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Goldman Sachs Group, Inc. (GS): Free Stock Analysis Report

Citigroup Inc. (C): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet