Gold Super Bull Run? JPM Sees $4K Soon, $5K If Fed Loses Grip

WATCH: Capitalism Under Attack — Why Socialism Fails Every Time

Gold has been climbing to record highs, and speculation is mounting about just how far the rally can go. Wall Street’s latest forecast hints at a historic milestone—but what could drive the next leg higher?

Gold prices have repeatedly hit record highs, with the $4,000 milestone now within sight. JPMorganJPM-- has forecast that gold will break through this key level by early 2026. If the Federal Reserve’s independence comes under political pressure, the bank says even $5,000 is possible.

The core driver of this rally is shifting. The report stresses that investor demand has now overtaken central banks as the main catalyst. Fueled by expectations of a Fed policy pivot, U.S. Treasury yields have fallen sharply, reigniting inflows into gold ETFs.

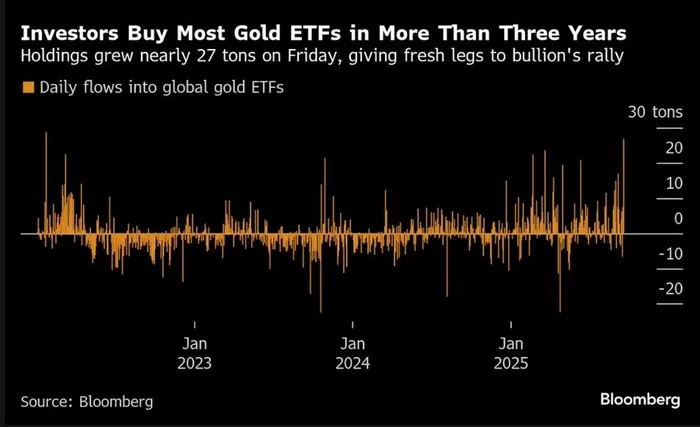

Data shows that in the two weeks to September 5, 2025, global gold ETFs added nearly 30 tons—the largest inflow since mid-April.

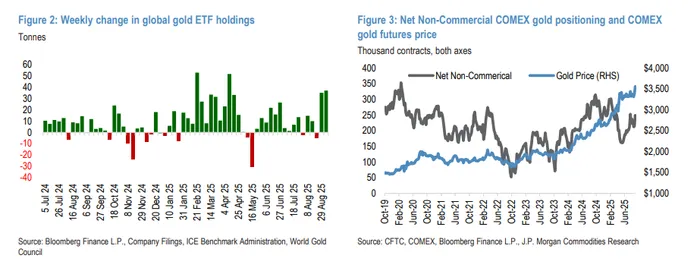

Speculative positions are also surging. Net long non-commercial futures positions in COMEX gold have reached new highs. JPMorgan economists expect that after next week’s rate cut, the Fed will lower rates at the next three consecutive meetings.

The bank emphasized that central bank buying remains strong, providing a solid foundation for the bull market. On top of that, investors are accelerating their entry. In the last four rate-cutting cycles, gold delivered double-digit returns in the nine months following the first cut.

The Fed has recently signaled that concerns about a weakening job market now outweigh worries about an inflation rebound, and rate cuts are expected in both October and December. Lower rates are a key tailwind for gold, as the metal provides no yield, reducing the opportunity cost of holding it.

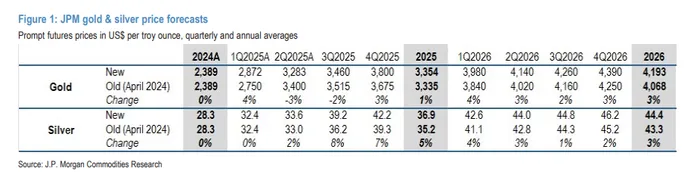

JPMorgan projects gold will reach $3,800 per ounce in Q4 2025 and break $4,000 in Q1 2026.

Moreover, while the Fed has so far defended its independence, political interference has not ended. If fears about Fed independence intensify, confidence in the dollar and U.S. Treasuries could be undermined, triggering a “flight to safety” into gold and other hard assets, potentially sending gold above $5,000.

The report lays out several quantitative models:

Market asymmetry: Global private and official gold holdings total around $9.4 trillion, compared with the $29 trillion U.S. Treasury market.

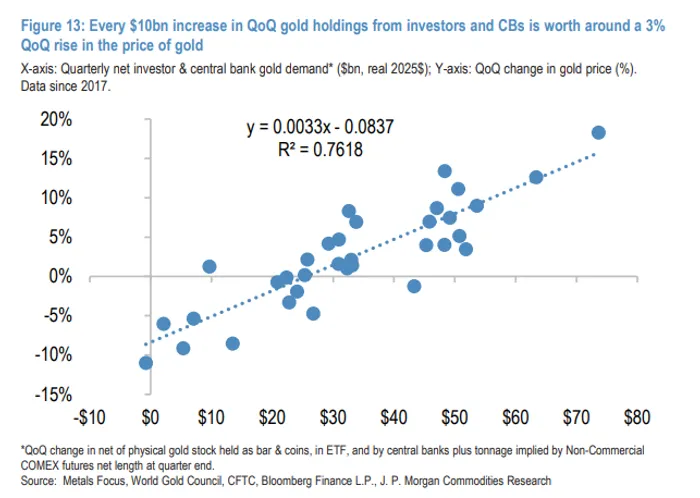

High price elasticity: Regression analysis shows that since 2017, each additional $10 billion in quarterly net gold demand from investors and central banks drives prices about 3% higher quarter-on-quarter.

Scenario analysis: If even a tiny fraction of the $29 trillion Treasury market rotated into gold—say $80 billion per quarter, just 0.1% of Treasuries’ value—gold prices could spike above $5,000 within two quarters.

Supply constraints are another factor

Annual mine production has stagnated. From 2013 to 2023, output only grew from 3,375.3 tons to a peak of 3,710.4 tons, before dropping 3% to 3,591.7 tons in 2024. Primary mine supply still accounts for 70–75% of global supply, with recycled gold contributing 25–30%. In 2024, recycled supply hit a decade-high of 1,366.8 tons.

Finding new large, high-grade deposits has become increasingly difficult. From 1990–2012, 350 projects yielded 2.89 billion ounces of resources. Between 2013–2022, only 26 new deposits were found, totaling just 200 million ounces. Stricter resource-sharing demands by host countries have further dampened investment appetite.

At the end of 2024, the combined cash costs, sustaining capital, exploration, admin expenses, and royalties for gold mining stood at around $1,450/oz. Rising labor and tax costs provide a floor for prices and continue to push the long-term gold price higher.

China’s role in gold markets is also expanding

Beyond buying gold openly and covertly, China is seeking to attract foreign sovereign reserves for custody at the Shanghai Gold Exchange. At least one Southeast Asian country has shown interest.

Custody services are crucial for credibility and liquidity, similar to vaults at the Fed and Bank of England, which hold thousands of tons of global reserves.

For countries excluded from mainstream markets, such as Russia or North Korea, China’s vaults could provide an alternative to build reserves and bypass Western financial restrictions.

Risks to the bull case remain

JPMorgan warns that the greatest risk is a sharp slowdown in central bank demand. Due to high prices, Q2 2025 central bank purchases dropped to 166.5 tons, the lowest since Q2 2022.

While the bank still expects average annual purchases of 700–800 tons in 2025–26—well above the ~400-ton average before 2022—any significant pullback could undermine the sustainability of the rally.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO