Gold Poised to Break Range — $4,000 in Sight Next Year?

Gold has been stuck in $3,100–$3,500 range, but that may be ending. With central banks quietly returning, ETFs piling in, and supply frozen, could $4,000 be closer than we think?

Since April this year, gold has been consolidating within the $3,100–$3,500/oz range for more than four months, showing no clear direction. But eventually, the market must pick a side.

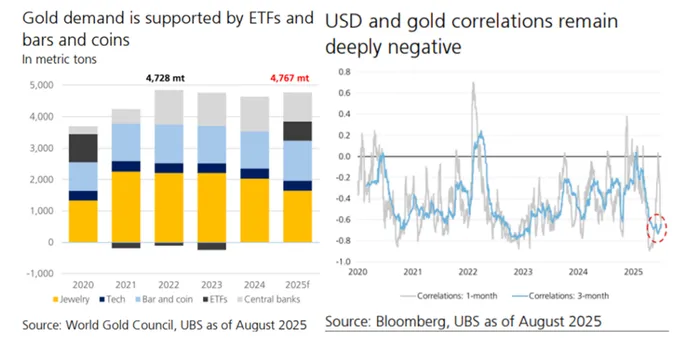

The bullish case rests on several pillars: global central bank demand is set to rebound as seasonal weakness ends, with purchases expected to accelerate in September.

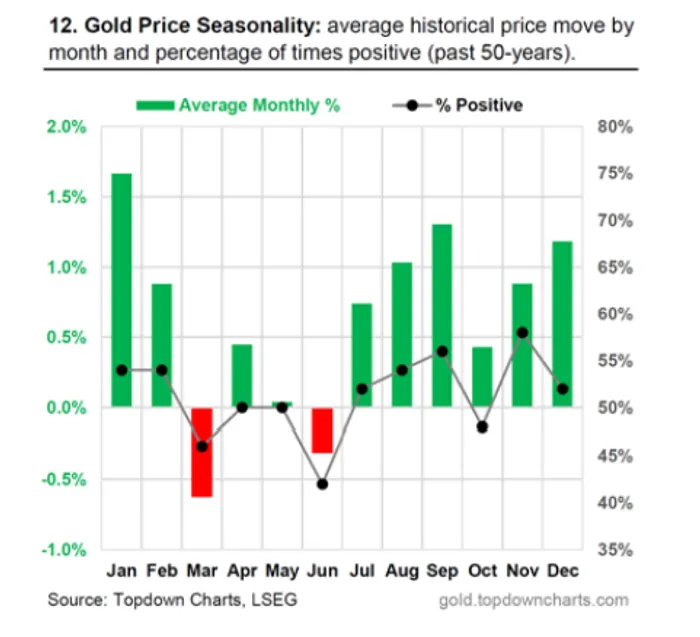

Seasonality is favorable — September has historically been gold’s second-strongest month in the past 50 years.

Commodity trading advisors (CTAs) continue to increase exposure to gold and maintain net long positions.

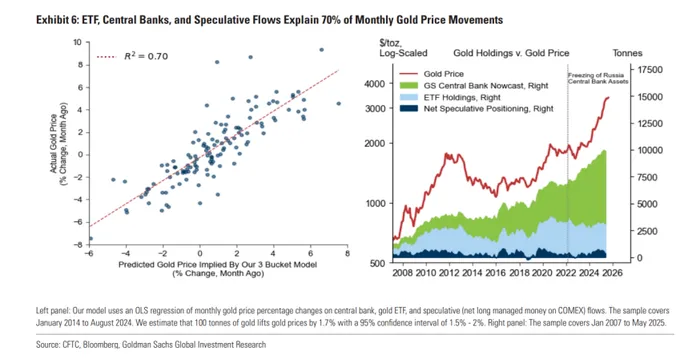

Goldman Sachs research shows that about 70% of gold price fluctuations are explained by flows from three “dedicated buyers”: ETFs, central banks, and speculators.

For every 100 tons of net gold purchases, the price tends to rise by about 1.7%. Based on robust structural demand from central banks, expected ETF inflows driven by Fed easing, and a 30% chance of U.S. recession in the next 12 months, GoldmanGS-- forecasts gold at $4,000/oz by mid-2025.

The most important driver remains central bank demand. After the Russia-Ukraine war broke out in 2022, around $300 billion of Russian FX reserves were frozen — mostly held in Western bonds. Since then, global central bank gold buying surged fivefold, particularly among emerging markets, as gold cannot be frozen or sanctioned.

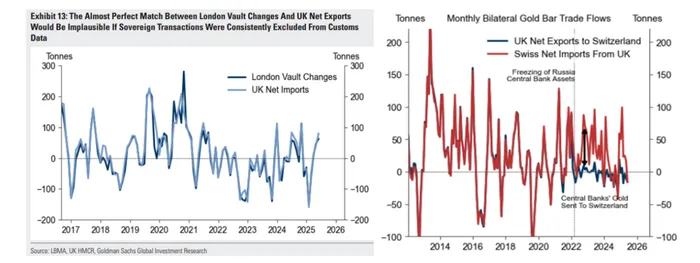

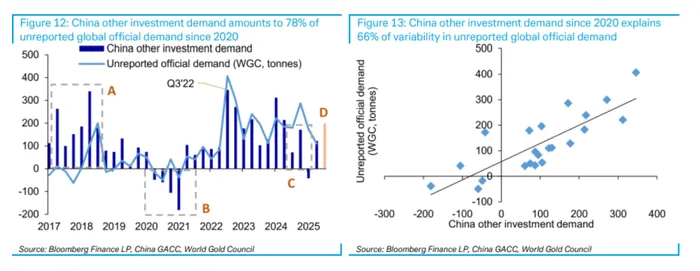

Currently, about two-thirds of official gold purchases are hidden, but London vault flows and U.K. gold export data offer clues. Excluding gold shipped directly from the U.K. to Switzerland, the gap between the two countries’ customs records represents undisclosed official demand.

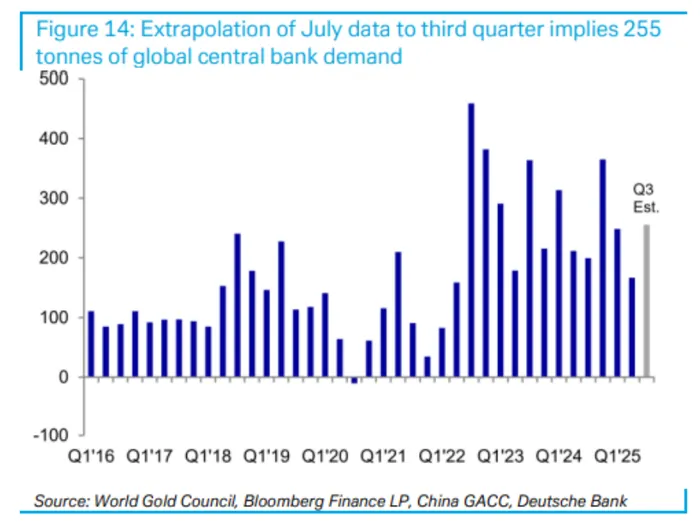

Deutsche Bank estimates that since 2020, about 78% of this “unreported official demand” came from China, including both official and private buying. Based on July’s accelerated imports and ETF inflows, China’s official gold purchases could jump significantly in Q3. Global gold demand could rebound from Q2’s 167 tons to 255 tons.

Using Goldman’s model, this implies potential for gold to break above $3,450/oz in Q3.

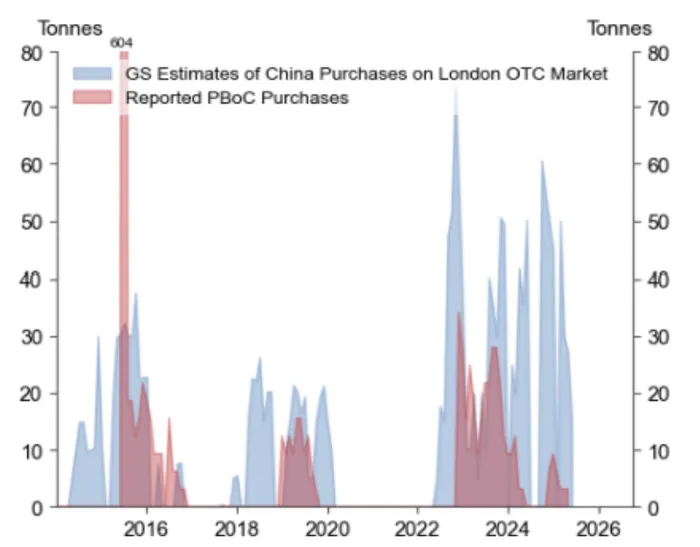

Goldman also estimates that the People’s Bank of China (PBoC) bought 27 tons in April, far above the officially reported 2 tons, while June saw no purchases.

This hidden Chinese buying provides structural support, weakening the traditional “higher prices suppress demand” logic.

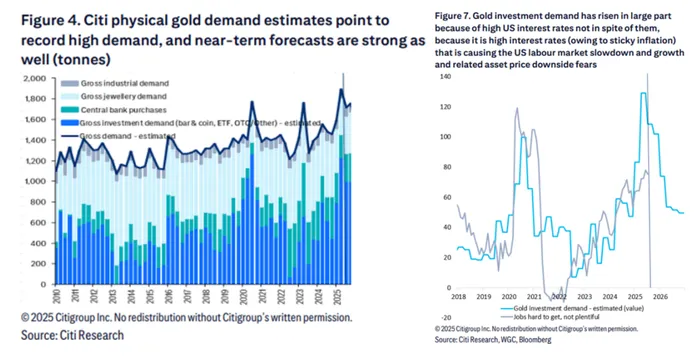

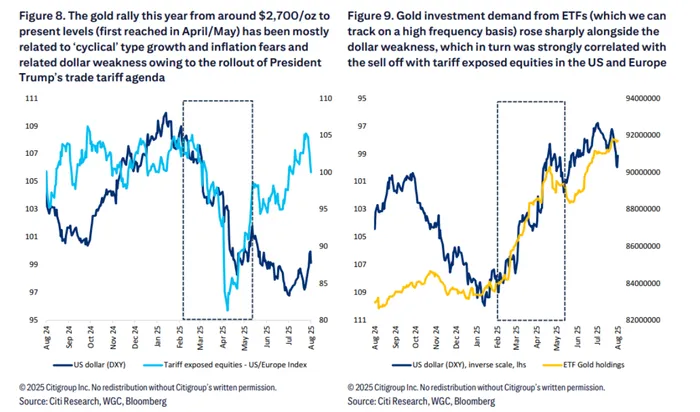

Beyond central banks, ETFs and investors are showing growing appetite for gold. The Trump administration’s “Reciprocal Tariff” strategy and its attempt to curb Fed independence have shaken global confidence in dollar assets. Gold is increasingly seen as a neutral “de-dollarization” reserve asset, anchoring a reshaped global reserve system.

Retail and smaller investors mainly gain exposure through ETFs, which have continued to see net inflows.

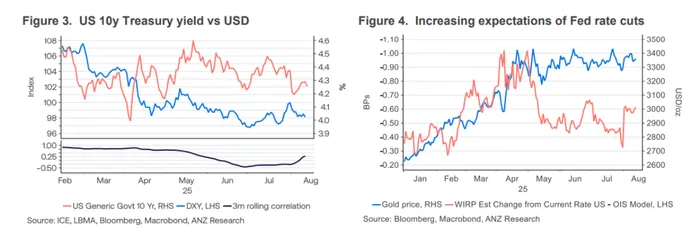

At the Jackson Hole symposium, Fed Chair Jerome Powell emphasized downside risks in the U.S. labor market, especially after May and June payroll data were sharply revised down. His dovish tone, highlighting recession risk over inflation, strengthened expectations of a September rate cut — supportive for gold.

If Trump secures greater influence over the Fed board, a more dovish central bank could emerge, implying a weaker dollar, higher inflation, and even stronger demand for gold.

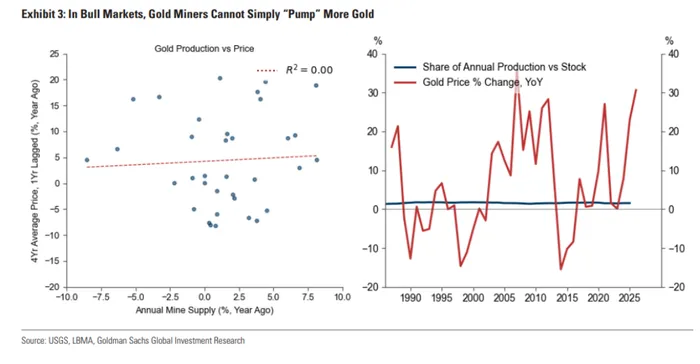

On the supply side, gold mine production is nearly flat due to environmental constraints, rising just 1% this year — showing little flexibility. Central banks are net buyers and won’t sell, while recycling volumes are limited. With demand strong and supply constrained, gold is biased upward.

Three factors to watch ahead:

Seasonal central bank buying resumes in September — China’s customs imports and Shanghai Gold Exchange deliveries will be key.

A Russia-Ukraine peace deal could trigger short-term profit-taking, but long-term fundamentals remain bullish.

Faster-than-expected Fed rate cuts and dollar weakness would accelerate ETF inflows.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.