GM Roars Back: Stock Soars 14% After Crushing Earnings and Slashing Tariff Hit

General Motors delivered a standout third-quarter report that reignited investor confidence in Detroit’s largest automaker, propelling shares up 14% in what would mark their best single-day performance since March 2020. The company’s earnings and guidance easily surpassed expectations, driven by solid vehicle demand, improved cost management, and lower-than-expected tariff headwinds. Despite the persistent challenges of tariffs, high input costs, and electric vehicle growing pains, GM’s strong execution in its core business helped lift both near-term profit expectations and long-term sentiment around its post-tariff recovery trajectory.

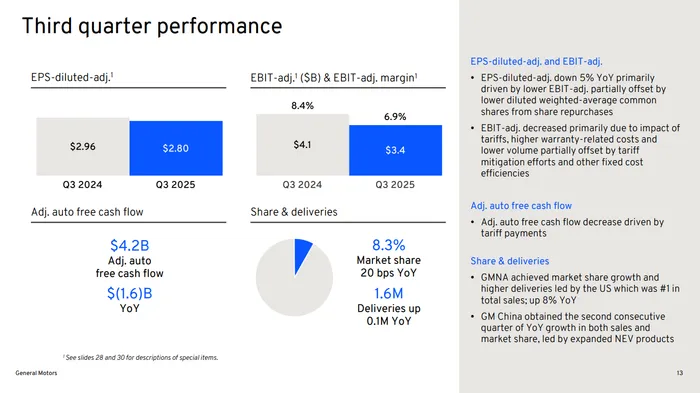

For the third quarter, GMGM-- posted adjusted earnings per share of $2.80, well ahead of Wall Street’s $2.31 consensus, and adjusted EBIT of $3.38 billion versus the $2.72 billion expected. Revenue came in at $48.6 billion, also topping estimates of about $45 billion. While sales were essentially flat year over year, higher vehicle pricing and stable consumer demand more than offset tariff-related costs and warranty expenses. CEO Mary Barra highlighted the company’s performance in a letter to shareholders, noting, “Thanks to the collective efforts of our team, and our compelling vehicle portfolio, GM delivered another very good quarter of earnings and free cash flow. Based on our performance, we are raising our full-year guidance, underscoring our confidence in the company’s trajectory.”

The company raised its full-year 2025 EBIT outlook to $12 billion–$13 billion, up from the prior $10 billion–$12.5 billion range, while also boosting adjusted EPS guidance to $9.75–$10.50 from $8.25–$10.00. Free cash flow expectations were lifted sharply to $10 billion–$11 billion, up from $7.5 billion–$10 billion, signaling stronger cash generation despite persistent macro headwinds. The new outlook suggests fourth-quarter adjusted EPS of roughly $2.00, modestly above consensus expectations. GM also lowered its expected tariff hit to $3.5–$4.5 billion for the year, down from $4–$5 billion previously, and said it plans to offset about 35% of that impact through pricing and operational efficiencies.

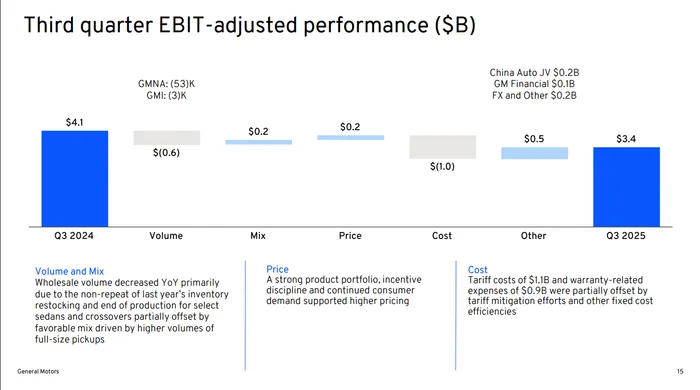

The tariff adjustment reflects the automaker’s ability to navigate a policy landscape that remains fluid under President Trump’s administration. GM even acknowledged the White House’s recent tariff revisions in its report, thanking the president for “important tariff updates” that included new levies on imported truck components but also a 3.75% offset for American-made vehicles. CFO Paul Jacobson emphasized that the company has “a better handle on the tariff structure now” and is “taking proactive steps to mitigate exposure while keeping product costs competitive.” Still, tariffs continue to pressure margins, with GM’s North American operating margin slipping to 6.2% from 9.7% a year ago. Barra reiterated that restoring margins to the 8%–10% range remains a “top priority” through cost discipline, production efficiency, and EV profitability improvements.

Tariffs were not the only cost headwind GM confronted. The company has faced growing challenges in its electric vehicle strategy, including a $1.6 billion impairment tied to its EV operations earlier in the quarter. Jacobson acknowledged that only about 40% of GM’s EV models are currently profitable on a contribution margin basis, adding that “it will take longer than initially expected for EVs to reach scale profitability.” Nevertheless, GM’s EV sales momentum continues: through Q3, the automaker’s U.S. EV market share rose to 13.8%, overtaking Hyundai and Kia, though it remains far behind Tesla. GM also said it is “right-sizing” EV production capacity and expects to reduce structural costs over the coming year.

Despite the margin squeeze from tariffs and EV investments, GM’s core business remains robust. North American sales rose 8% year over year to more than 710,000 vehicles, with trucks, crossovers, and SUVs driving the gains. The company reported record Q3 sales in these categories, supported by average transaction prices now exceeding $50,000. Dealer inventories fell 16% year over year, underscoring tight supply and solid retail demand. International operations also improved, with profits up $217 million in China and $184 million in other regions, offsetting some of the North American softness. GM Financial delivered adjusted earnings of $804 million, up 17% year over year, benefiting from stable credit performance and higher financing volume.

GM ended the quarter with $21.8 billion in cash on hand and continued to reward shareholders aggressively. The company has repurchased $3.5 billion in stock year-to-date and reduced diluted shares outstanding by 15% year over year. GM also fully redeemed $1.3 billion in debt that was set to mature in 2025, signaling confidence in its balance sheet flexibility and cash generation trajectory. Barra indicated that management remains committed to “balanced capital allocation” and hinted at potential for further capital returns should market conditions remain stable.

Looking ahead, GM’s guidance signals optimism that 2026 will mark another step forward in restoring margins and growing profitability. The company expects continued improvement in EV losses, warranty costs, and tariff offsets, alongside an industry backdrop of steady demand. Wedbush analyst Dan Ives praised GM’s execution, writing that “while tariff headlines and EV impairments have weighed on sentiment, GM continues to navigate the complex backdrop impressively.” He maintained a Buy rating and raised his price target to $77, citing valuation and technical momentum.

The bottom line: GM’s third-quarter report was a decisive win in an environment still clouded by policy volatility and industry transition. Stronger-than-expected profits, robust cash flow, and lowered tariff exposure reassured investors that the automaker’s fundamentals remain sound. With shares up 14%—their best day in more than five years—GM’s execution and guidance upgrades have reignited confidence that the automaker can balance short-term pressures with long-term transformation.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet