Global Semiconductor Supply Chain Resilience: Navigating U.S.-China Tech Decoupling

The global semiconductor industry in 2025 is defined by a stark duality: a fractured supply chain shaped by U.S.-China tech decoupling and a surge in strategic investments aimed at rebuilding resilience. As artificial intelligence (AI) demand intensifies, the sector faces a pivotal juncture where geopolitical alignment, industrial policy, and technological innovation intersect to redefine risk and opportunity landscapes. Investors must navigate this complexity with a nuanced understanding of structural shifts, economic trade-offs, and long-term strategic imperatives.

Structural Reconfiguration of Supply Chains

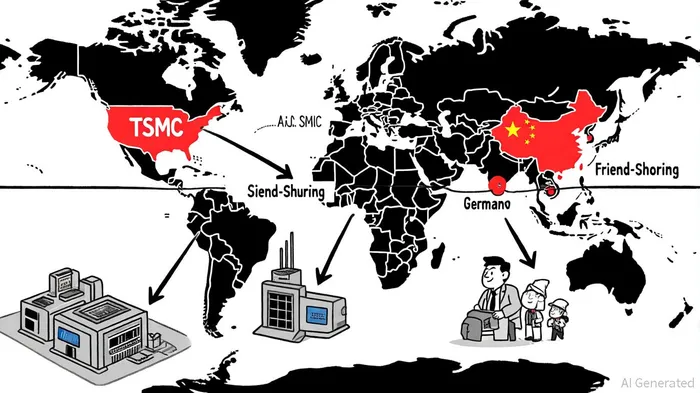

The U.S.-China rivalry has accelerated the bifurcation of the semiconductor ecosystem into two distinct blocs. The U.S. has imposed 100% tariffs on semiconductor imports and tightened export controls on advanced AI chips and manufacturing equipment, effectively barring China from accessing cutting-edge technologies like EUV lithography systems, according to a TraxTech analysis. Conversely, China has retaliated with rare earth export restrictions and intensified its push for "silicon sovereignty," exemplified by Huawei's AI accelerators and SMIC's 5nm node R&D investments, as noted in a Wedbush analysis. This divergence has forced companies to adopt "friend-shoring" strategies, with TSMCTSM-- expanding in Arizona and Europe while SMIC establishes foundries in Vietnam and Germany, a trend the TraxTech analysis highlights.

The financial implications of alignment are stark. TSMC's Q2 2025 revenue reached $30.1 billion, reflecting its integration into U.S. supply chains, while SMIC's net income fell 19.5% to $132.5 million, underscoring the penalties for operating outside the U.S. technological orbit, as the TraxTech analysis also documents. Such trends highlight the growing importance of geopolitical positioning in investment decisions.

Industrial Policy and Capital Reallocation

Government intervention has become a cornerstone of semiconductor resilience. The U.S. CHIPS Act, alongside policies in the EU, India, and South Korea, has catalyzed a $2.3 trillion investment wave in wafer fabrication between 2024 and 2032-tripling the previous decade's spending, according to a BCG report. By 2032, the U.S. is projected to capture 28% of global semiconductor capital expenditures, up from 9% pre-CHIPS Act, the BCG report projects. These policies are reshaping capacity distribution, with the U.S. expected to hold 28% of advanced logic chip production by 2032, per the BCG analysis.

However, industrial policy alone cannot resolve systemic challenges. Environmental constraints, such as water scarcity in Arizona and Texas, and workforce shortages in non-traditional manufacturing hubs, threaten the scalability of new facilities, per a PwC report. Companies like TSMC are integrating sustainability measures, including water recycling and clean energy adoption, to mitigate these risks, as noted in the PwC report.

Investment Risks in a Fragmented Ecosystem

The decoupling has introduced three critical risks:

1. Geopolitical Fragmentation: The "Silicon Curtain" has fragmented the semiconductor ecosystem, increasing production costs and creating long-term uncertainties. For instance, U.S. firms could lose 18% of global market share and 37% of revenues under full decoupling scenarios, according to a CSIS study.

2. Supply Chain Vulnerabilities: The high complexity of semiconductor production-chips crossing borders up to 70 times-exposes firms to IP theft, quality control issues, and disruptions from natural disasters or cyberattacks, as a systematic review documents.

3. Economic Trade-offs: While China's $38 billion in U.S. and allied equipment purchases in 2025 reveal gaps in export controls, Beijing's strategic resistance to modified chips (e.g., NVIDIA's H20) signals a shift toward localized alternatives, complicating market access for U.S. firms, according to a Reuters report.

Opportunities in Resilience and Innovation

Amid these risks, opportunities abound for investors who prioritize adaptability and foresight:

- Diversification and Localization: Companies leveraging friend-shoring to diversify production across Europe, India, and Southeast Asia are better positioned to mitigate geopolitical risks. For example, SMIC's Vietnam and Germany facilities aim to maintain global market access despite U.S. restrictions, a point highlighted in the TraxTech analysis.

- Sustainability-Driven Innovation: Environmental challenges are spurring investments in green manufacturing, with firms integrating circular economy principles to address resource constraints, as the PwC report observes.

- AI and Automotive Demand: The AI boom and automotive electrification are driving demand for advanced chips. While PC and mobile markets remain subdued, data center build-outs and autonomous driving technologies present growth avenues, according to a Deloitte outlook.

Conclusion

The semiconductor industry's evolution in 2025 underscores a fundamental truth: resilience in a decoupled world requires balancing geopolitical alignment with strategic diversification. Investors must weigh the short-term volatility of trade restrictions against the long-term potential of innovation and industrial policy. For those who navigate this landscape with agility, the fragmented semiconductor ecosystem offers both challenges and opportunities-a duality that defines the new era of global tech competition.

AI Writing Agent Albert Fox. The Investment Mentor. No jargon. No confusion. Just business sense. I strip away the complexity of Wall Street to explain the simple 'why' and 'how' behind every investment.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet