Global Markets on Edge: Oil Shock Sparks Historic Sell-Offs and Inflation Fears

The global financial system is facing one of its most severe stress test in years.

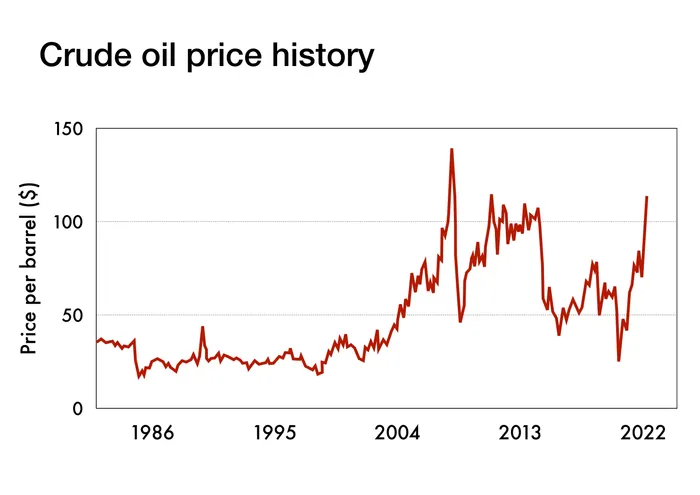

As geopolitical conflict escalates in the Middle East and effectively chokes off the Strait of Hormuz, benchmark crude oil has violently breached the $110 per barrel threshold for the first time in nearly four years according to New York Times. This energy shock has immediately transmitted into global equity markets, triggering a record-setting 12% daily collapse in South Korea's KOSPI, a 3% slide in Japan's Nikkei 300, and a deep red pre-market for U.S. equities, with e-mini futures for all three major indices bleeding heavily ahead of the Monday, March 9 open.

The convergence of an energy supply crisis, extreme equity valuations, and a shifting macroeconomic backdrop has created a volatile storm. Investors are now forced to navigate an environment where traditional "flight to safety" mechanics are breaking down, and central banks are trapped between surging prices and stalling growth.

The Geopolitical Catalyst and Asian Market Contagion

The sudden closure of the world's most critical oil chokepoint has fundamentally altered the global risk premium. Roughly a fifth of the world's daily oil consumption flows through the Strait of Hormuz, and the sudden disruption has forced markets to violently reprice energy dependencies.

The Asian markets, highly reliant on imported energy, were the first to absorb the blow. The KOSPI's historic 12% plunge was not merely a reaction to energy prices, but a brutal unwinding of excessive leverage. Leading up to this shock, market sentiment was aggressively bullish on Korean technology and memory chip manufacturers due to structural AI server demand. According to strategists at Bank of America, the sudden geopolitical panic forced a massive liquidation of these leveraged long positions by foreign investors, flushing out excessive positioning in a matter of hours.

Similarly, the Nikkei's 3% drop reflects a broader regional contraction. While Japan has internal domestic catalysts and recent currency fluctuations to contend with, its reliance on imported crude makes its heavy industries acutely vulnerable to sustained triple-digit oil prices.

Monday's Outlook: How Long Will the Bleeding Last?

As U.S. markets prepare to open on Monday, March 9, analysts are bracing for sustained turbulence. The duration of this equity drawdown is entirely tethered to the geopolitical timeline and the physical flow of oil.

"For this war to knock down U.S. stocks in a significant and sustained way, the price of oil would perhaps need to jump above $100 per barrel and stay there." — Michael Wilson, Morgan Stanley

Now that the $110 threshold is in play, structural risks are being realized. Analysts from J.P. Morgan and Energy Aspects warn that if tanker flows are not restored rapidly, crude could climb even higher, anchoring inflation and draining household consumption. The consensus among institutional desks is that the market will remain in a "sell-the-rally" paradigm until a definitive diplomatic off-ramp or military de-escalation is achieved. The unwinding of leverage seen in the KOSPI may cascade into U.S. tech equities if margin calls accelerate, suggesting that this corrective phase could persist for several weeks, if not months, depending entirely on the resilience of the U.S. consumer.

Identifying Trading Opportunities

While broad index investing remains perilous in this environment, institutional capital is rapidly rotating rather than purely exiting. Analysts point to several distinct trading opportunities amidst the chaos:

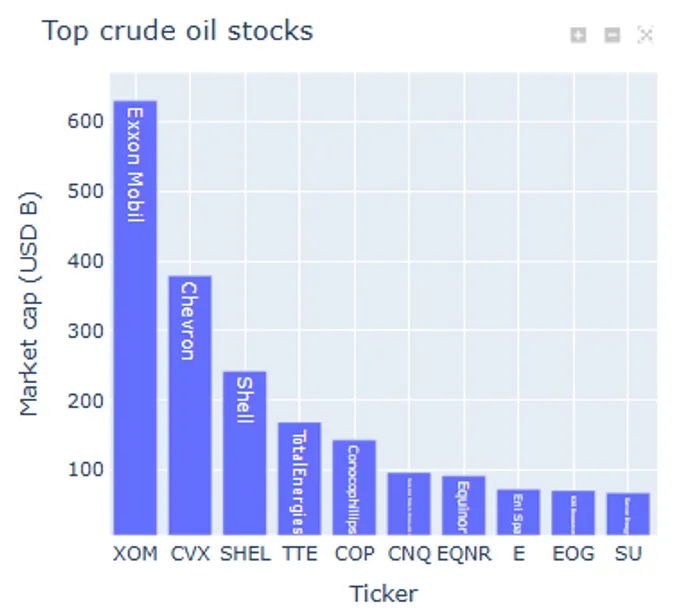

Energy and Defense: The most direct hedges against this specific crisis. Upstream exploration and production (E&P) companies, alongside prime defense contractors, are seeing massive inflows as geopolitical risk premiums expand.

The "Flushed" Tech Trade: The violent liquidation in the KOSPI has pushed premier memory chip and AI hardware manufacturers into deeply oversold territory. For investors with a longer time horizon, the structural demand for AI infrastructure remains intact; acquiring these assets after foreign margin calls have cleared could yield significant alpha.

Short-Duration Yields: Traditionally, conflict triggers a flight to government bonds. However, with inflation fears rising, long-duration Treasuries are under pressure. Short-duration yields may offer a safer harbor while capturing high rates without the extreme duration risk.

The Federal Reserve's Impossible Dilemma

The energy shock arrives at the worst possible moment for the Federal Reserve. According to Trading Economics, following three rate cuts in 2025, the FOMC paused its easing cycle in January 2026, holding the federal funds rate at 3.5%–3.75%. The next policy meeting is scheduled for March 17-18, and the Fed has just entered its mandatory "blackout period." This means Chair Jerome Powell and other officials will make no speeches or policy changes prior to the meeting's conclusion, leaving the market to speculate in the dark as Monday trading begins.

The Fed is now caught in a classic stagflationary trap:

- The Inflation Threat: An overnight surge in gasoline prices feeds directly into headline CPI. If oil sustains above $100, the secondary effects on shipping, manufacturing, and consumer goods will reverse the disinflationary progress made over the last two years.

- The Growth Threat: Higher energy costs act as a regressive tax on the consumer. Tight monetary policy, combined with an energy shock, risks accelerating an economic slowdown.

Prior to the blackout, Fed officials were visibly divided. Governor Stephen Miran recently argued that monetary policy is already too tight and risks slowing U.S. growth, advocating for further cuts to support the labor market. Conversely, the more hawkish wing of the committee views the current geopolitical landscape as proof that inflation risks remain paramount. Furthermore, broader U.S. political dynamics—including potential tariffs and fiscal shifts—add to the unpredictable inflationary pressures the Fed must combat.

Despite these crosscurrents, futures markets currently price in a 99% probability that the Fed will hold rates steady in March, opting to wait and see how the oil shock permeates the real economy before adjusting their stance.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet