Genuine Parts Stock Down 15% YTD: Buy, Sell or Hold the Stock Now?

Genuine Parts Company GPC, based in Atlanta, is a distributor of automotive and industrial replacement parts and materials. The company operates a vast network of more than 10,800 locations, primarily across North America, Europe and Australasia.

Genuine Parts operates through two segments – Automotive Parts and Industrial. In the fourth quarter of 2025, the company reorganized its Automotive Parts Group into two separate business segments. The North America Automotive Parts Group (North America Automotive) includes all automotive operations in the United States and Canada, while the International Automotive Parts Group (International Automotive) comprises automotive operations across Europe and Australasia.

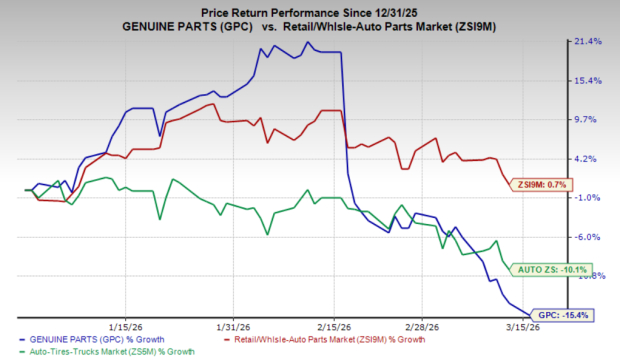

Year to date, Genuine Parts’ shares have underperformed the Zacks Retail/Wholesale-Auto Parts Market and the auto sector. GPC’s shares have lost 15.4% year to date, underperforming the Zacks Retail/Wholesale-Auto Parts Market’s (ZSI9M) 0.7% gain and the auto sector’s 10.1% decline during the same period.

Analyzing YTD Stock Performance

Image Source: Zacks Investment Research

What Supports the Investment Case for GPC

Acquisition-Driven Growth Strengthens Market Position

Genuine Parts is actively expanding its market presence through strategic acquisitions. Notable deals include KDG in early 2022, which enhanced its industrial segment in North America, and Gaudi in 2023, which grew its European automotive footprint.

In 2024, Genuine PartsGPC-- acquired MPEC and Walker to bolster its NAPA network and Midwest reach. In 2025, GPCGPC-- spent more than $320 million toward acquisitions, including the Benson Auto Parts deal (≈85 stores in Canada), reinforcing its presence in key priority markets and supporting long-term share gains.

Motion Segment Poised to Benefit From Industrial Recovery Trends

Motion is supported by stable MRO demand, growing data center activity, and onshoring trends driven by shifting trade policies. While some commodity-related end markets remain soft, its disciplined cost structure and operational focus position it to benefit from an industrial recovery. A rebound in OEM capital spending could drive margin expansion through operating leverage, offering a compelling earnings acceleration opportunity over the next cycle.

Strong 2026 Sales Outlook Signals Steady Growth Momentum

GPC expects 2026 sales growth in the range of 3-5.5%. North America Automotive sales are projected to rise 3-5%, driven by strong demand in North America and the benefits from the Benson acquisition in Canada. International Automotive is expected to grow 3-6%. Industrial sales growth is expected to be in the range of 3-6%, supported by improving trends in Motion’s core MRO and data center end markets.

Restructuring Actions Drive Cost Savings and Margin Expansion

GPC is executing a global restructuring initiative to better align its cost base and asset footprint with current market conditions. The efforts delivered approximately $175 million in benefits last year, exceeding management’s expectations of $110-$135 million. In 2026, the company’s restructuring actions are expected to generate an additional $100-$125 million in annualized benefits.

Shareholder-Friendly Policies and Strong ROE Highlight Value Proposition

GPC continues to build investor confidence through shareholder-friendly actions. A dividend aristocrat, the company has paid dividends annually since 1948 and recently raised its 2026 payout 3.2% to $4.25 per share, marking its 70th consecutive annual increase.

In 2025, Genuine Parts returned $564 million to shareholders through dividends. The company’s 16.9% return on equity far exceeds the auto sector average of 8%, highlighting strong capital efficiency and management’s commitment to rewarding shareholders.

Key Risks for GPC Stock

Rising Cost Pressures Weigh on Profitability

The company anticipates continued cost inflation from rising salaries and wages, largely due to mandated pay increases in international markets, along with ongoing inflationary headwinds in U.S. healthcare expenses, which are increasing at a high single-digit pace.

Higher Operating Expenses and Investments to Pressure Margins

Genuine Parts expects adjusted SG&A to rise 30-50 basis points in 2026 as persistent inflation in rent and operating costs offset restructuring savings. As a result, SG&A is projected to grow slightly faster than revenues, pressuring margins. Depreciation and interest expenses are expected to create a $30 million headwind due to ongoing capital investments and financing obligations. Rising operating expenses will hit near-term earnings growth.

Weakness in the European Segment Raises Growth Concerns

GPC’s European segment is under pressure, with sales down approximately 2% in local currency and roughly 3% in comparable sales in the fourth quarter. The region faces soft demand and ongoing cost pressures. While strategic initiatives, including NAPA brand expansion, are supporting performance, near-term growth and margin expansion remain challenged.

Tariff Uncertainty and End-Market Weakness Pose Risks

Tariff and trade uncertainty add to demand risk, particularly among more cautious end customers. In the Industrial segment, weakness in commodity-related markets, such as metals and heavy manufacturing, could limit growth. The automotive business also faces pressure as independent and small business customers manage inventory cautiously in a dynamic operating environment.

Final Thoughts for GPC Stock

Acquisition-driven expansion, resilient demand in its Motion segment and a steady 2026 sales outlook enhance GPC’s prospects. Ongoing restructuring initiatives and consistent shareholder returns further strengthen its long-term growth profile and capital efficiency.

However, near-term headwinds, including persistent cost inflation and rising operating expenses and softness in the European segment, could pressure margins and earnings growth. Macro uncertainty and cautious customer spending also pose risks. Given these factors and its current Zacks Rank #3 (Hold), the stock may not offer an attractive entry point for new investors at this time.

Stocks to Consider

Some better-ranked stocks in the auto space are RENAULT RNLSY, Modine Manufacturing MOD and Strattec Security STRT, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for RNLSY’s 2026 sales and earnings implies year-over-year growth of 14.4% and 176.3%, respectively. The EPS estimates for 2026 and 2027 have improved 34 cents and 18 cents, respectively, in the past 30 days.

The Zacks Consensus Estimate for MOD’s fiscal 2026 sales and earnings implies year-over-year growth of 21.3% and 19%, respectively. The EPS estimate for fiscal 2026 and fiscal 2027 has improved 1 cent and 4 cents, respectively, in the past 30 days.

The Zacks Consensus Estimate for STRT’s fiscal 2026 sales and earnings implies year-over-year growth of 2.1% and 16.2%, respectively. The EPS estimate for fiscal 2026 and fiscal 2027 has improved $1.01 and 48 cents, respectively, in the past 60 days.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Genuine Parts Company (GPC): Free Stock Analysis Report

Strattec Security Corporation (STRT): Free Stock Analysis Report

Modine Manufacturing Company (MOD): Free Stock Analysis Report

RENAULT (RNLSY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet