GE Soars Past Expectations with Blowout Earnings and Cash Flow Surge

GE Aerospace delivered another resounding earnings beat in the third quarter of 2025, underscoring the strength of its transformation into a pure-play jet engine powerhouse. The company posted results that topped Wall Street expectations across every major metric, raised its full-year guidance for the second consecutive quarter, and generated robust free cash flow—cementing its position as one of the strongest industrial stories of the post-breakup era. With shares pushing toward all-time highs around $309 in premarket trading, Tuesday’s results represent a key test of investor sentiment: after an 80% rally this year, the question now is whether even exceptional performance is enough to propel GEGE-- higher.

The numbers left little to quibble over. Adjusted earnings per share came in at $1.66, comfortably ahead of the $1.45 consensus estimate, while adjusted revenue surged 26% to $11.31 billion, topping forecasts of $10.41 billion. Orders rose 2% year over year to $12.8 billion, reflecting steady demand across both commercial and defense programs. CEO Larry Culp highlighted the company’s “exceptional execution” and reiterated that GE’s proprietary lean operating model—branded internally as “FLIGHT DECK”—continues to drive productivity and quality improvements across the enterprise. He emphasized that priority suppliers shipped more than 95% of their committed volume for a third straight quarter, a notable improvement for an industry still grappling with supply chain friction.

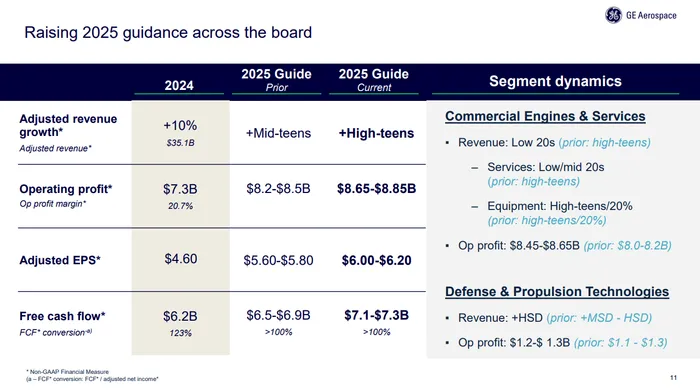

Culp’s team raised full-year guidance across all key metrics. GE now expects adjusted EPS of $6.00–$6.20, up from its prior range of $5.60–$5.80 and comfortably above consensus estimates of $5.91. Adjusted revenue growth is expected to accelerate to the high teens, while adjusted operating profit is projected to reach $8.65–$8.85 billion, up from prior guidance of $8.2–$8.5 billion. Free cash flow, a crucial performance yardstick for GE, is now seen at $7.1–$7.3 billion for 2025, up from earlier guidance of up to $6.9 billion. Culp noted that “free cash flow conversion” remains above 100%, meaning the company is generating more cash than net income—a level of operational efficiency that Wall Street views as critical validation of the turnaround’s durability.

Within GE Aerospace’s two reporting segments, both delivered standout quarters. The Commercial Engines and Services (CES) division posted orders of $10.3 billion, up 5%, as robust aftermarket demand offset minor timing effects in equipment orders. Revenue climbed 27% to $8.9 billion, led by a 28% surge in services, where internal shop visit revenue rose 33% and spare parts sales gained more than 25%. Equipment revenue increased 22%, driven by a 33% jump in unit deliveries and favorable pricing that offset a lower spare engine ratio. Operating profit in the segment soared 35% to $2.4 billion, with margins expanding 170 basis points. Management raised 2025 guidance for CES revenue growth to the low 20% range, supported by continued strength in services, now expected to rise in the low to mid-20s. Profit guidance was also boosted to $8.45–$8.65 billion, reflecting favorable mix and strong pricing power.

The Defense and Propulsion Technologies (DPT) segment also posted solid growth, with revenue up 26% to $2.8 billion despite a 5% decline in orders due to timing across quarters. Defense engine deliveries surged 83%, while operating profit rose 75% to $386 million as improved customer mix and pricing offset higher costs. Margins expanded 380 basis points to 13.8%. For the full year, DPT expects revenue growth in the high-single digits and operating profit between $1.2 billion and $1.3 billion, up from prior guidance of $1.1–$1.3 billion. Both divisions benefited from higher volumes and continued momentum in global air travel, with commercial activity still outpacing expectations despite lingering macro uncertainties.

Free cash flow stood out as one of GE’s most impressive achievements this quarter. The company generated $2.36 billion in FCF during Q3, up 30% year over year, supported by higher earnings, stronger collections, and continued capital discipline. Cash from operations reached $2.6 billion, while FCF conversion hit 134%—well above management’s target of 100%. Year-to-date free cash flow totals $5.9 billion, a 27% increase from the same period last year. These results demonstrate not only improving profitability but also tight control over working capital and investment spending, reinforcing investor confidence in GE’s ability to generate cash through both cycles.

The macro backdrop remains favorable for GE’s twin growth engines—commercial aviation and defense. Air travel demand continues to expand, while engine maintenance activity is booming as fleets return to full utilization. Meanwhile, defense demand has remained resilient amid elevated geopolitical tensions, fueling long-term visibility for GE’s military engine programs. The company’s backlog remains substantial, and new wins, including a major widebody engine deal with Qatar Airways, continue to fill the production pipeline.

Shares of GE were up about 3% premarket following the report, trading just shy of their all-time high around $309. The stock has already surged roughly 80% this year, vastly outperforming both peers and the S&P 500. While valuation remains elevated—trading around 44 times projected 2026 earnings—analysts argue the premium is justified by GE’s accelerating cash flow, expanding margins, and clean balance sheet. With supply chain bottlenecks easing, free cash flow outpacing profit growth, and guidance moving higher yet again, GE’s Q3 results reaffirm its standing as one of the industrial sector’s most impressive comeback stories. The only question left for investors: how high can it fly?

Two minutes to understand what`s happening in daily premarket trading.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet