U.S. GDP Growth and Emerging Economic Weakness in Q1 2025: Assessing the Sustainability of the Q2 Rebound Amid Macroeconomic Stress

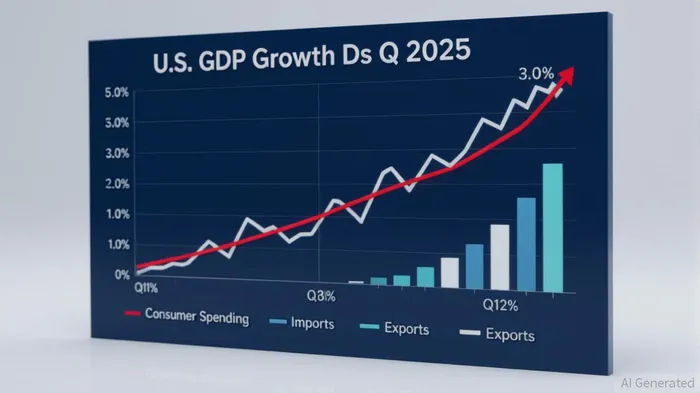

The U.S. economy's second-quarter rebound in 2025 has been hailed as a triumph of resilience, with real GDP expanding at a 3.0% annual rate—a stark reversal from the 0.5% contraction in Q1. This surge, driven by a 30.3% drop in imports and a 1.4% rise in consumer spending, has sparked debates about whether the recovery is genuine or a statistical illusion. For investors, the critical question is: Can this rebound sustain itself, or is it masking deeper structural weaknesses?

The Q2 Rebound: A Tale of Two Sectors

The second-quarter growth was fueled by a dramatic shift in trade dynamics. Imports, which had surged by 37.9% in Q1, collapsed by 30.3% in Q2, artificially inflating GDP by subtracting a smaller drag. While this technicality is often overlooked, it underscores a key risk: the rebound may not reflect broad-based strength but rather a one-time correction in trade flows.

Consumer spending, however, provided a more durable boost. A 1.4% increase in Q2 (compared to 0.5% in Q1) suggests households remain a pillar of demand. Yet, the underlying data is mixed. Final sales to private domestic purchasers—a metric that strips out inventory changes and trade distortions—rose by only 1.2% in Q2, down from 1.9% in Q1. This moderation hints at a slowdown in domestic demand, which could constrain future growth.

Employment and Inflation: A Mixed Bag

The labor market, a cornerstone of economic health, appears stable but strained. The unemployment rate averaged 4.2% in Q2, near the Congressional Budget Office's estimate of the non-cyclical rate, while payroll job growth accelerated to 150,000 per month. However, labor force participation for those aged 55+ hit an 18-year low of 38.0%, signaling demographic headwinds.

Inflation, meanwhile, has eased. The core PCE price index rose 2.5% year-over-year in Q2, down from 3.5% in Q1, suggesting the Federal Reserve may have time to cut rates gradually in 2026. Yet, the headline CPI edged up to 2.7% by June 2025, partly due to base effects and rising energy prices. This duality—controlled core inflation but sticky headline measures—poses a risk for the Fed's policy path.

Business Investment: A Cautionary Trend

The manufacturing sector, a bellwether for broader economic health, reveals a more troubling picture. Despite a 24.7% surge in machinery and equipment spending in Q1 (as firms rushed to avoid tariffs), business confidence has waned. The NFIB small business optimism index hit a multi-year low in April 2025, and plans for capital expenditures are at their weakest since 2020.

Investment in structures is projected to decline by 1.6% in 2025, and machinery spending is expected to fall by 2.5% in 2026. These trends reflect a sector grappling with high tariffs, interest rates, and policy uncertainty. For example, the automotive and steel industries have already seen production delays due to supply chain bottlenecks and rising input costs.

Policy Uncertainty: The Long Shadow

The Trump administration's tariffs, while not yet visible in aggregated price data, loom large. A 30.3% drop in imports in Q2 may have been a temporary windfall, but sustained trade barriers could erode competitiveness and stifle long-term growth. The Fed's dilemma—balancing rate cuts with inflation risks—adds to the uncertainty.

Investors should monitor the 10-year Treasury yield, currently near 4.5%, as a proxy for market sentiment. A sharp rise could signal fears of inflation reacceleration or policy missteps. Conversely, a decline might indicate confidence in the Fed's ability to engineer a “soft landing.”

Investment Implications

For equity investors, the rebound in consumer-driven sectors (e.g., retail, services) has outperformed manufacturing and capital goods. However, the latter's struggles suggest caution in overexposed sectors. Defensive stocks in utilities and healthcare, which are less sensitive to economic cycles, may offer safer havens.

Bond investors face a balancing act. While the Fed's potential rate cuts in 2026 could push Treasury yields lower, the risk of inflation rebounding—particularly in energy and housing—means holding shorter-duration bonds is prudent.

The Consumer Confidence Index, currently at 97.2, remains below recessionary thresholds but shows a modest improvement. This suggests households are cautiously optimistic, but not overly exuberant—a trend that could stabilize consumption in the short term.

Conclusion: A Fragile Optimism

The Q2 rebound is a statistical and political victory, but its sustainability depends on three factors:

1. Continued consumer spending despite rising prices for essentials like housing and energy.

2. A stabilization of trade policy to avoid further distortions in import/export balances.

3. A Fed that navigates its dual mandate without overreacting to transitory data points.

For now, the U.S. economy appears resilient but strained. Investors should adopt a barbell strategy: overweighting sectors with strong cash flows (e.g., tech, healthcare) while hedging against potential volatility in cyclical industries. The key is to remain agile, as the line between a durable recovery and a fragile bounce is thinner than it appears.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet