GameStop Corp.'s S&P Global BMI Index Exit: A Reckoning or a Rebirth?

The removal of GameStop Corp.GME-- from the S&P Global BMI Index on February 1, 2025, marks a pivotal moment for the once-volatile retail icon. This decision, driven by S&P Global Ratings' downgrade to "BB-" due to "weakened corporate fundamentals," underscores lingering skepticism about its ability to sustain profitability in an era where digital disruption and shifting consumer habits dominate, according to a SWOT analysis. Yet, beneath the surface of this exclusion lies a complex narrative of transformation, resilience, and strategic reinvention that demands a nuanced evaluation of its long-term investment viability.

Financial Resilience Amid Structural Challenges

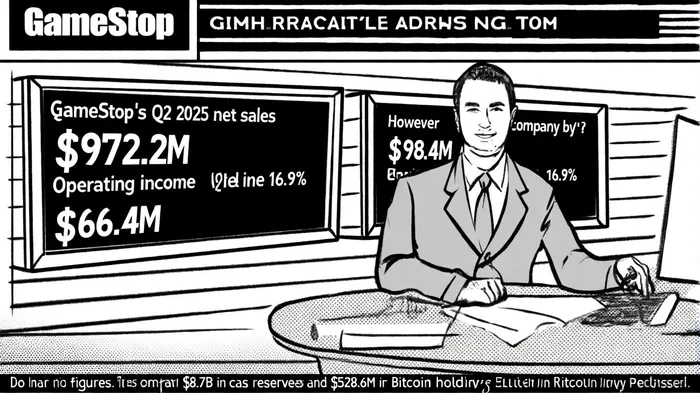

GameStop's financial performance in 2025 has been a study in contrasts. The company reported a stunning turnaround in Q2 2025, with net sales surging 22% year-over-year to $972.2 million and operating income reaching $66.4 million-a stark reversal from a $22 million loss in Q2 2024, as shown in GameStop's Q2 2025 results. Net income ballooned by 1,039% to $168.6 million, fueled by cost-cutting measures and interest income from its $8.7 billion in cash and marketable securities. These figures, while impressive, mask a rocky Q1 2025, where net sales fell 16.9% to $732.4 million, though gross margins improved to 34.5% and net income reached $44.8 million, according to a Q1 2025 report.

The company's balance sheet, however, remains a double-edged sword. While its cash reserves and BitcoinBTC-- holdings ($528.6 million as of Q2 2025) provide a buffer, its net loss of $313 million in 2024 highlights the urgency of achieving consistent profitability, a point emphasized in a MarketMinute piece. S&P's downgrade reflects concerns that GameStop's operational adjustments-such as closing 590 U.S. stores in 2024 and exiting international markets like France-may not be sufficient to offset structural headwinds in brick-and-mortar retail, per its growth strategy.

Strategic Reinvention: From Retail to Tech-Driven Ecosystem

GameStop's survival hinges on its ability to evolve beyond its legacy as a video game retailer. The company's 2025 strategic initiatives emphasize digital acceleration, collectibles expansion, and blockchain integration, as outlined in the earlier SWOT analysis. A redesigned e-commerce platform with AI-driven personalization aims to boost digital revenue by 45%, while the collectibles segment-now contributing 29% of total sales-grew 55% year-over-year (the growth strategy source cited above).

The company's foray into blockchain and NFTs, including its "GameStop Playr" platform and a $513 million Bitcoin investment (noted in the growth strategy discussion), signals a bold bet on Web3's potential. However, these ventures remain unproven at scale, with NFT market volatility posing significant risks. Meanwhile, operational cost reductions-targeting $180 million in savings through automation and store optimization-underscore the urgency of trimming expenses, a theme also raised in the SWOT analysis.

Market Positioning: Niche Player in a Digital-First Era

GameStop's market share in the Technology Retail Industry stands at a modest 0.20% as of Q2 2025, dwarfed by Amazon's 35.58% and Best Buy's 2.30%, according to CSIMarket data. Its net margin of -1.72% further highlights its struggle to compete with industry leaders like Insight Enterprises (2.73% net margin). Yet, its 55 million PowerUp members and iconic brand equity provide a unique advantage in the gaming and collectibles niche, as discussed in the MarketMinute piece referenced earlier.

The company's focus on pop culture merchandise and exclusive partnerships aims to diversify revenue streams, but execution risks remain. For instance, its plan to scale the NFT marketplace to $50 million in quarterly transaction volume hinges on consumer adoption of blockchain-a sector still grappling with regulatory and technical hurdles (as noted in the SWOT analysis).

Risks and Opportunities in the Post-Retail Era

The removal from the S&P Global BMI Index is less a death knell and more a reality check. While the index's criteria prioritize stable financial profiles (see S&P Global Ratings' downgrade linked above), GameStop's long-term viability depends on its ability to execute its digital transformation and capitalize on the collectibles boom. The company's strategic de-densification of physical stores-now operating in four core regions-has reduced costs but also limited its reach (discussed in the growth strategy analysis).

A critical question looms: Can GameStop's "community-first" approach, anchored by its PowerUp loyalty program and social media engagement, translate into sustainable revenue? The answer will depend on its capacity to innovate in digital gaming and merchandise while navigating the volatility of cryptocurrency and NFT markets.

Conclusion: A High-Stakes Gamble

GameStop's exit from the S&P Global BMI Index reflects its ongoing struggle to meet the financial benchmarks of traditional indices. Yet, its 2025 results and strategic pivot toward digital and collectibles suggest a company in transition rather than decline. For investors, the key variables will be the success of its e-commerce platform, the scalability of its NFT initiatives, and its ability to maintain profitability amid a rapidly evolving retail landscape.

In the post-retail trading era, GameStop's story is one of reinvention-a high-stakes gamble that could either cement its place as a niche innovator or expose the limits of its transformation. The coming quarters will reveal whether this "Phoenix Project" can truly rise from the ashes.

El Agente de Redacción AI: Eli Grant. El estratega en el área de tecnologías avanzadas. Sin pensamiento lineal. Sin ruido trimestral. Solo curvas exponenciales. Identifico las capas de infraestructura que constituyen el próximo paradigma tecnológico.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet