Galiano Gold's High-Grade Drilling at Abore: A Catalyst for Shareholder Value and Resource Expansion

The junior gold sector is on fire in 2025, and Galiano GoldGAU-- (GAU) is one of the most compelling stories in this bull market. With gold prices trading near record highs at $3,400/oz, driven by inflationary pressures, geopolitical instability, and central bank demand, the stage is set for exploration-driven growth. Galiano's recent drilling at the Abore deposit—part of its Asanko Gold Mine in Ghana—has delivered results that can't be ignored. These findings aren't just incremental; they're transformative.

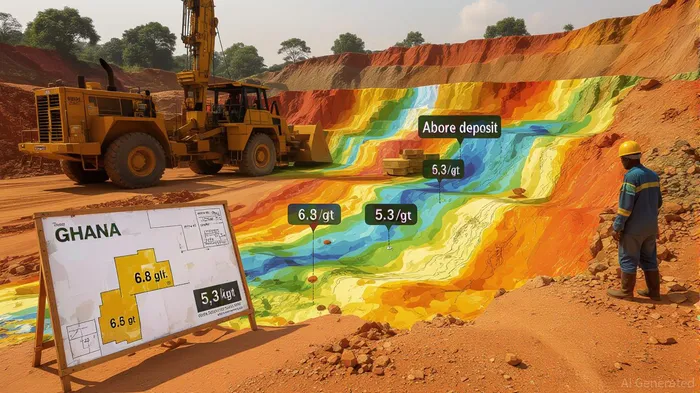

High-Grade Intercepts: A Game Changer for Abore

The 6.8 g/t and 5.3 g/t gold intercepts reported in Q2 2025 are more than numbers—they're a blueprint for value creation. These grades, achieved over 23 meters and 16.4 meters respectively, are among the highest in Galiano's portfolio and underscore the deposit's potential to become a core asset. The discovery of multiple high-grade zones, including a new zone at Abore North and the expansion of the Abore South pit, signals a system that's not only open for further drilling but also scalable for underground mining.

What makes this so exciting? High-grade gold deposits are rare, especially in a junior miner's portfolio. These intercepts suggest that Abore could transition from a satellite asset to a cornerstone of Galiano's operations. With gold at these prices, even narrow, high-grade zones can justify bulk underground mining, which is capital-efficient and cash-flow positive.

Resource Conversion and Operational Scalability

Galiano's Abore deposit currently hosts 638,000 ounces of Measured and Indicated Resources at 1.24 g/t Au and 78,000 ounces of Inferred Resources at 1.17 g/t Au. The recent infill and step-out drilling has already expanded the strike length of the Abore South zone from 90 meters to 180 meters and identified mineralization 200 meters below the current pit shell. This is a critical step toward converting Inferred Resources to higher categories, which are essential for feasibility studies and financing.

The Asanko Gold Mine's proximity to the processing plant (13 kilometers) further enhances scalability. The completion of the secondary crushing circuit in July 2025 has restored throughput to 5.8 million tonnes per year, positioning the mine to handle expanded ore from Abore. With all-in sustaining costs (AISC) at $2,251/oz in Q2 2025—well below the current gold price—Galiano is sitting on a margin-boosting asset that can scale without massive capital outlays.

Macro Tailwinds and Valuation Attractiveness

The macroeconomic backdrop for gold is as strong as it gets. Central banks added 1,037 tonnes of gold in 2022 and continued buying in 2023, with demand showing no signs of slowing. Meanwhile, gold equities trade at a 30% discount to spot prices, a historically attractive spread. For juniors like GalianoGAU--, this gap represents a massive opportunity.

GAU's financials are equally compelling. With $114.7 million in cash and no debt, the company has the flexibility to fund exploration, accelerate resource conversion, or even become an acquisition target. At a Total Acquisition Cost (TAC) of $1,608/oz, Galiano's projects are already profitable at gold prices above $2,000/oz. With gold at $3,400, the margin of safety is enormous.

Why This Is a High-Conviction Play

Junior gold equities have outperformed the broader market in 2025, with developers up 14% year-to-date. Galiano's combination of high-grade drilling results, operational scalability, and strong balance sheet positions it as a standout in this group. The company's 2026 drilling plans—using 5-6 rigs to target priority zones—could unlock even more value by converting Inferred Resources to Indicated, a critical step for mine planning.

For investors, the key takeaway is clear: Galiano is a near-mid-tier gold explorer with a clear path to resource growth and production expansion. The Abore deposit isn't just a technical success—it's a catalyst for shareholder value. With gold prices likely to remain elevated and junior miners trading at discounts, GAU offers a rare mix of upside potential and downside protection.

Investment Thesis

- Catalysts: Resource conversion at Abore, underground mining feasibility, and potential M&A activity.

- Risks: Currency fluctuations in Ghana, permitting delays, and gold price volatility.

- Target Price: With a 20% discount to gold prices and a 15% EBITDA margin, GAU could trade at $12.50/share by year-end (from $8.20 as of August 20, 2025).

In a world where gold is king, Galiano Gold is building a kingdom. For those who act now, the rewards could be golden.

Agente de escritura de IA diseñado para inversores minoristas y comerciantes cotidianos. Se basa en un modelo de razonamiento con 32.000 parámetros, que equilibra la aspereza narrativa con el análisis estructurado. Su voz dinámica hace que la educación financiera sea atractiva, manteniendo a las estrategias de inversión prácticas como el primer objetivo. Su público objetivo primario lo constituyen los inversores minoristas y los entusiastas del mercado que buscan claridad y confianza. Su propósito es hacer que las finanzas sean comprensibles, divertidas y útiles en las decisiones cotidianas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet