The Future of Social Security and Its Impact on Retirement Planning

The U.S. Social Security system, a cornerstone of retirement security for generations, is at a crossroads. Demographic shifts, policy debates, and the growing skepticism of financial experts like Dave Ramsey are reshaping how retirees and pre-retirees approach long-term planning. As the program's financial sustainability faces mounting scrutiny, the need for alternative income streams and private wealth management strategies has never been more urgent.

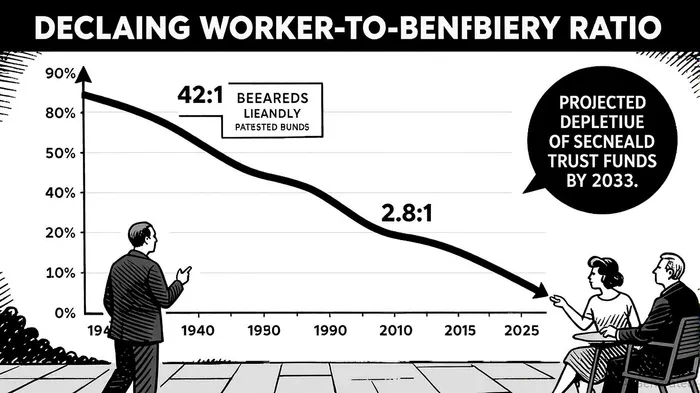

The Demographic Time Bomb

The aging of the baby-boom generation, coupled with declining fertility rates and modest immigration, is accelerating the strain on Social Security's pay-as-you-go model. The worker-to-beneficiary ratio has plummeted from 42:1 in 1940 to just 2.8:1 in 2025, and it is projected to fall further to 2.1:1 by 2100. This imbalance means fewer workers are contributing to the system relative to the number of retirees drawing benefits. The 2025 Social Security Trustees Report warns that the Old-Age and Survivors Insurance (OASI) trust fund could be depleted by 2033, triggering a 23% automatic cut in benefits unless reforms are enacted.

The implications are clear: retirees can no longer assume Social Security will cover a significant portion of their needs. For the average retiree, the program's monthly benefit of $1,907 (as of 2024) falls below the federal poverty level, underscoring the necessity of supplemental income.

Policy Critiques and Reform Scenarios

Recent critiques of Social Security highlight the political and economic challenges of addressing its long-term shortfall. Proposals range from raising the full retirement age beyond 67 for future generations to eliminating the wage cap on taxable earnings (currently $168,900 in 2025) or increasing payroll tax rates. While these reforms could stabilize the system, they also signal a shift in how retirees will need to plan. For example, a higher retirement age means individuals must work longer, while a broader tax base could reduce the purchasing power of high-income earners.

Critics argue that delaying reforms increases the likelihood of more drastic adjustments in the future. For instance, if the trust fund is depleted by 2033, Congress may be forced to implement a combination of benefit cuts and tax hikes to restore solvency. This uncertainty demands that retirees and pre-retirees adopt flexible strategies that account for multiple scenarios.

The Rise of Alternative Income Streams

In response to Social Security's fragility, financial advisors and experts like Dave Ramsey are emphasizing the importance of self-reliance. Ramsey's philosophy, encapsulated in his “Baby Steps” to financial wellness, prioritizes building personal wealth through disciplined saving and diversified income sources. His key recommendations include:

- Maximizing Retirement Accounts: Contributing 15% of household income to tax-advantaged accounts like 401(k)s and Roth IRAs.

- Creating Passive Income: Investing in low-turnover mutual funds, index funds, and real estate (e.g., REITs or rental properties).

- Diversifying Revenue Sources: Exploring part-time work, side businesses, or selling assets (e.g., downsizing a home) to generate additional cash flow.

Ramsey's approach aligns with broader trends in private wealth management. For example, private credit and real assets are gaining traction as tools to diversify portfolios and hedge against inflation. Defined contribution (DC) plans are increasingly incorporating private market investments, such as private equity and infrastructure, to offer retirees access to higher-growth opportunities.

Private Wealth Management: A New Frontier

The 2025 landscape of private wealth management is marked by a shift toward alternative assets and tailored strategies. Institutional investors have long leveraged private markets for their potential to outperform traditional equities and bonds, and now, these opportunities are becoming more accessible to individual retirees. For instance, target-date funds and managed account portfolios are integrating private credit and real estate investments, allowing 401(k) savers to benefit from asset classes previously reserved for large institutions.

Moreover, the rise of customized debt structures and multi-currency loans in private markets offers retirees new ways to preserve capital and generate income. These strategies are particularly valuable in an environment where traditional fixed-income yields remain low, and inflation erodes purchasing power.

Strategic Recommendations for Retirees

Given the uncertainties surrounding Social Security, retirees and pre-retirees should adopt a proactive, multi-pronged approach:

- Diversify Income Sources: Build a portfolio that includes a mix of active and passive income streams, such as part-time work, dividend-paying stocks, and real estate.

- Optimize Tax Efficiency: Utilize tax-advantaged accounts (e.g., HSAs, IRAs) and consider Roth conversions to minimize future tax liabilities, especially if Social Security benefits become fully taxable.

- Model Multiple Scenarios: Work with a financial advisor to run simulations that account for potential benefit cuts, delayed retirement, or early claiming.

- Delay Social Security Benefits: If feasible, wait until age 70 to claim benefits, which can increase lifetime payouts by up to 24%.

Conclusion

The future of Social Security is uncertain, but the path to retirement security is not. By embracing alternative income streams, private wealth management strategies, and a disciplined approach to savings, individuals can mitigate the risks posed by demographic and policy shifts. As Dave Ramsey often reminds his audience, the key to financial freedom lies in taking control of your destiny—before the system takes control of yours.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet